What Ashneer says and that Gabbar says is not a commentary on business side of the Company. So its a unnecessary distraction for the investors.

1 Like

Today was at Ahemdabad lounge at 5pm. I checkin usually with axis privilege credit card. The lady at the counter told me that there is a 10 minutes waiting as the lounge is full and in the meantime asked me the type of card.

When I showed her, she tells me Axis Bank has disabled few cards including privilege for select sector which includes Ahmedabad. I told her I have not received any message from Bank, she swiped and showed me the error message.

This is getting interesting ![]()

2 Likes

Did you not try to check the eligibility on their site before hand, they have been talking about the ease of use because of this feature. It seems they now issue a QR based on this, and one can just show this at lounge. I just checked up my HDFC Bank cards eligibility and it show up fine.

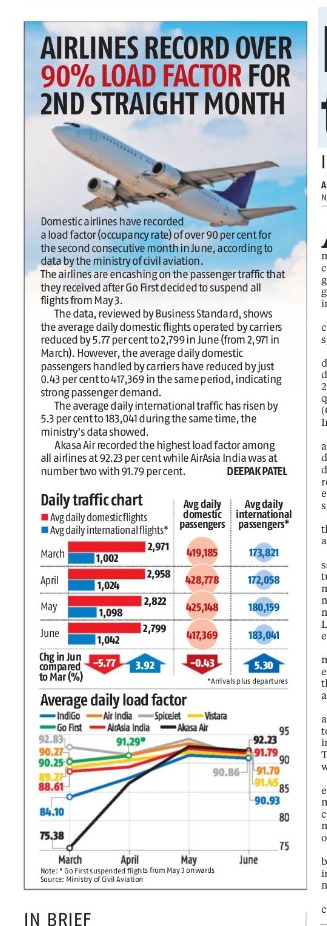

Seems the domestic passenger at almost similar level as Q4 (which was 37.5 Mn). As per mgmt. there is a seasonality in the air traffic business, as 40-45% of the business is in H1 and 55-60% is in H2.

3 Likes

3 Likes

1 Like

Air traffic continues to surge during Q1Fy24. Below is the air traffic data from AAI (https://www.aai.aero/en/business-opportunities/aai-traffic-news)

| Passenegers (in millions) | Q1FY24 | Q1FY23 | Growth% |

|---|---|---|---|

| International | 16.24 | 12.03 | 35.0 |

| Domestic | 76.73 | 64.43 | 19.1 |

| Total | 92.97 | 76.46 | 21.6 |

Below is the data during last 4 quarters about passenger’s (in millions) and revenue of dreamfolks during the quarter. This need not corelate always. Lets c how it will play out during Q1FY24.

| Q1FY23 | Q2FY23 | Q3FY23 | Q4FY23 | |

|---|---|---|---|---|

| Total passengers( in millions) | 76.46 | 73.56 | 86.8 | 90.6 |

| Revenue in Cr | 160 | 171 | 204.0 | 238 |

While clear risk has emerged to the business model over last two quarters with many banks restricting free lounge access, this seems to have nullified with overall growth in passengers.

Much bigger news is dreamfolks collaboration with plaza premium group. This probably good example of what capable management can do in what seems to be easy to disrupt business model.

DFS will get access to 340+ plaza premium lounges across 4 continents. With this inclusion dreamfolks global touchpoints will increase to 1700+. Q1 concall may provide more insights on the this collaboration and what impact it will have on revenue for the company.

dreamfolks and plaza premium.pdf (625.6 KB)

Discl: I have reduced my holding by ~30%.

5 Likes

We should have always expected it. But I don’t see it as a threat to the business model yet. Imagine, one is selling some stuff at a market place, and has free samples to give. Whom will he chose to give it ? Type A: To the crowd who seem likely to buy the stuff after they have tried the free sample or Type B: the crowd who will try free sample and simply walk away. If seller has no way of differentiating between the 2 types, then hard luck. But if he has a way of knowing, then any rational seller would give it to type A. Credit card issuers have the data to separate type A from B. So, it’s very logical and this was coming.

Why it’s not a threat to the business model yet is because 1. we are still at single digit percentage of eligible credit card users using this facility. The general perception, among public with higher paying capacity is, they don’t want enter into a over crowded lounge. It’s claustrophobic. So it’s not like if the credit card issuers, who are footing the bill, withdraw the privilege from certain category of customers then the whole business model went kaput. India is a country with growing aspirations, we will see customers with better credit profile using this space, which is actually good news for credit card issuers, as they find more type A customers. 2. It’s one of the best reward schemes that I have seen from credit card issuers in a long time (God knows what all bs they have tried in the name of reward-separate card, points, redeem, expiry etc). Earlier lounge access was given from Visa/MC, so there was no loyalty per se to the card issuer. Now since it’s coming directly from issuer, they stand to gain from the customer loyalty. 3. Credit scores are a reality for any person who ever wants to take a loan. Imagine using a card only for free lounge access and not paying it’s 2/- rs charge only to have your credit score lowered and suffering in future. 4. The lounge business model is not a new invention made by dreamfolks, it’s existing in many developed economies since ages and it has stood the test of time so far. So there is no logic of being negative on the business model for India.

The higher growth in international passenger should be music to the ears of mgmt. International passenger spend more time at airport, have higher rates. Going by the numbers, it looks like this year dreamfolks could close in or cross on 100 cr. PAT mark. So now trading at 40x current year. Not cheap, but given the nature of business not expensive either. At, VP, we have experience of making money in expensive businesses which remain expensive for a reason. Examples galore. I think, this is one such business (at least I hope so).

I will be keen to see what they do with the money that they are earning. Keen to see a good dividend policy of say about 50-60% of their earnings.

Disc: Remain invested with good allocation. No buys in last month.

12 Likes

I used to think similarly that lounge access is getting advertised excessively in recent months and with high surge in usage, banks will start restricting access.

But, What I have observed is that Lounge Access continues to remain a key attraction for new credit card users (we know banks want to continue card penetration in India).

Secondly, the restrictions on lounge access are mostly on the lower end cards which also pushes these users to upgrade to premium card versions which has higher fees.

The risk that I am closely looking at is capacity.

Today Dreamfolks’ growth opportunity is limited by available lounge capacity, their growth momentum now largely depends on new lounges coming up in India or expansion of existing lounge space as the queues outside most lounges clearly indicate peak utilisation is approaching or already reached for.

The Plaza Premium + partnership with Master Card indicates a good runway in the International side.

Definitely feel, Bank Card driven access can “if not kill, atleast displace Priority Pass leadership”.

4 Likes

The company is trying to diversify the offerings from the airport lounges by expanding offerings to railway stations, golf courses along with multiple growth drivers like airports, modernization of railway stations. Although, it’s a small percentage of its revenue at the moment, the runway is huge for airport lounges as well as railway lounges.

According to reports, the Airports Authority of India (AAI) has already invested a substantial amount of Rs. 1000 Crore in airports across India during the April-June period. Looking ahead, all airports in India are projected to spend approximately Rs. 20,000 crore in the fiscal year 2023-24, with Rs. 4,155 crore already spent up to this point. - Moneycontrol Report- AAI

A quick Google news search highlights that multiple airport expansion activities are currently underway across India.

These significant investments and expansion plans in the airport sector, along with the modernization of railway stations, present promising opportunities for DreamFolks to capitalize on.

1 Like

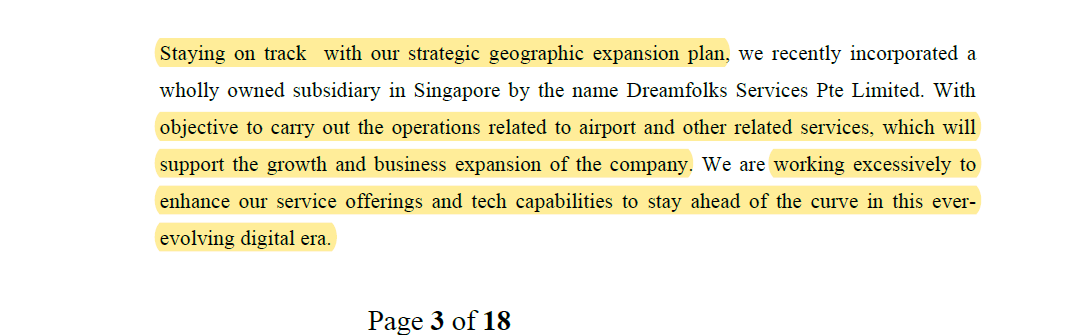

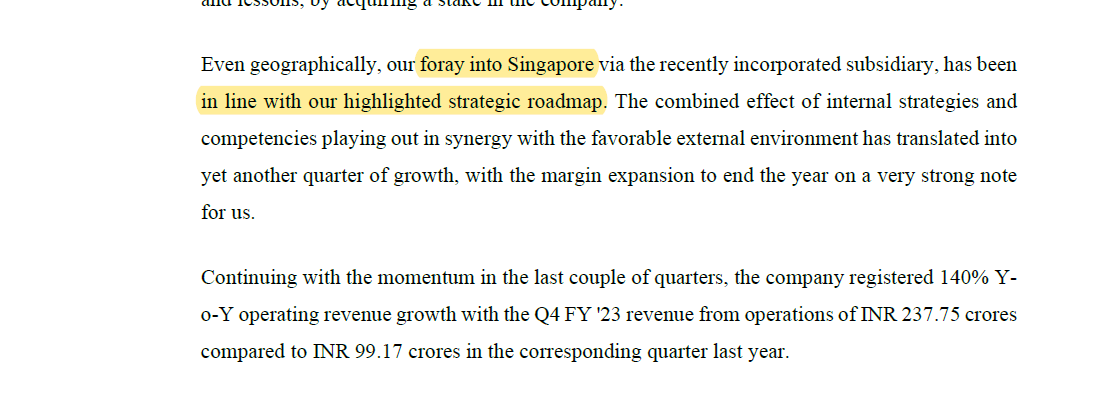

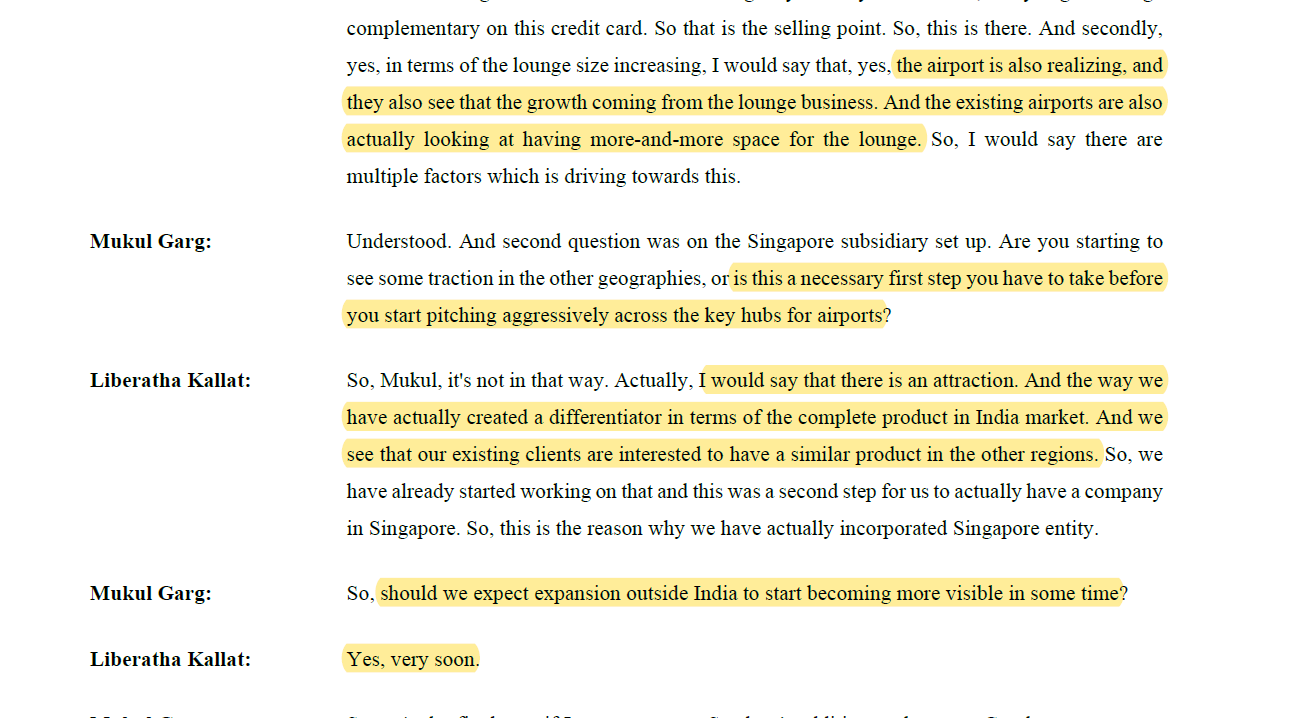

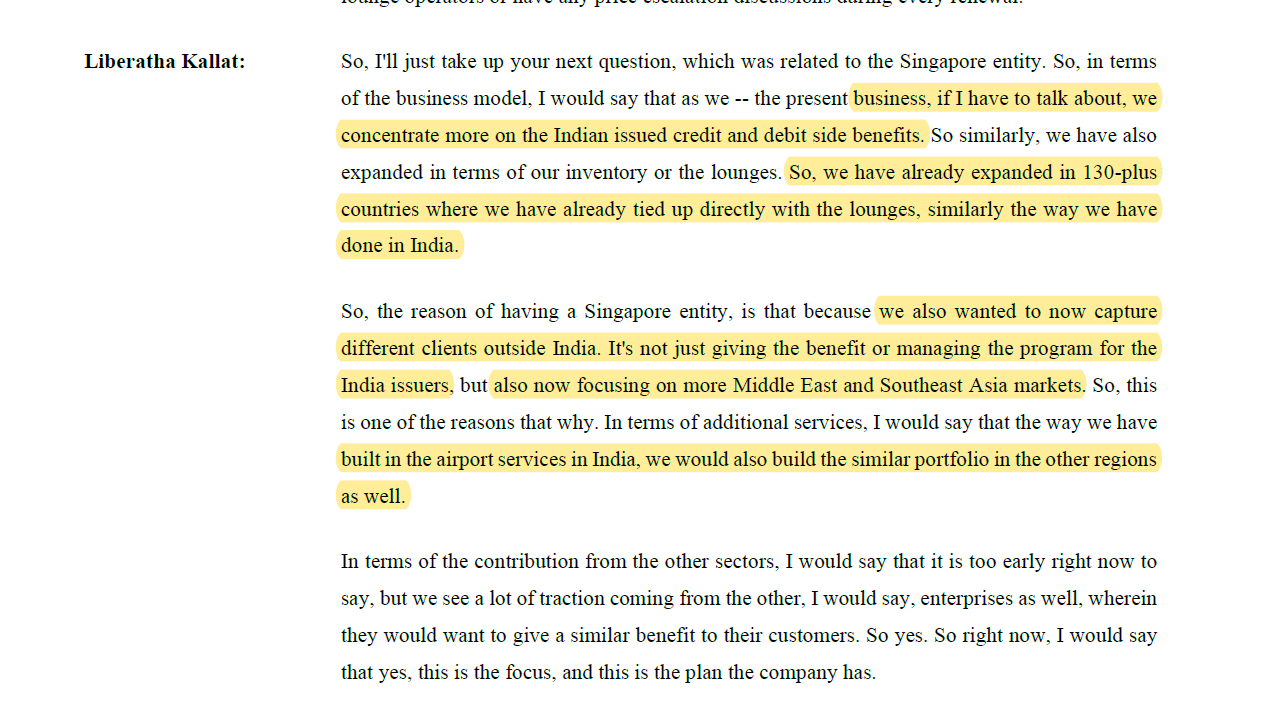

Another thing we should not miss about the company is, it’s aspiration in pursuing growth.

See, these snapshots from last Q call.

These are some bold ambitions. If the company succeeds in Singapore which seems to have one major airport (Changi), has a monthly traffic rate of ~5 Million. So total maket size may be about a qtr or 20% of India’s air traffic. But it’s a prestigious airport with very high value footfall. Singapore just replaced Japan as the most valuable passport. If company can make a mark in such a prestigious market, more doors can open.

We live in a time, when lot of business decisions are being influenced by geo politics. And fortunately or unfortunately the two major players are and US - Priority Pass and China Dragon Pass . There could be a genuine case for a 3rd player to provide an alternative and Dreamfolks is nicely placed for that. Let’s see if they make it count.

Overall, my point is, don’t get too negatively influenced by news of some credit card withdrawing the lounge facility to it’s least favorable customers. That’s par for the course. Keep an eye on the big picture. This service is not going outdated just because we saw surge in new first time credit card users choking the lounges for few qtrs and then abandoning the card. The utility value of the service goes much beyond that. Stay on till the company is showing growth.

Disc: Invested, will consider adding, if it correct meaningfully.

10 Likes

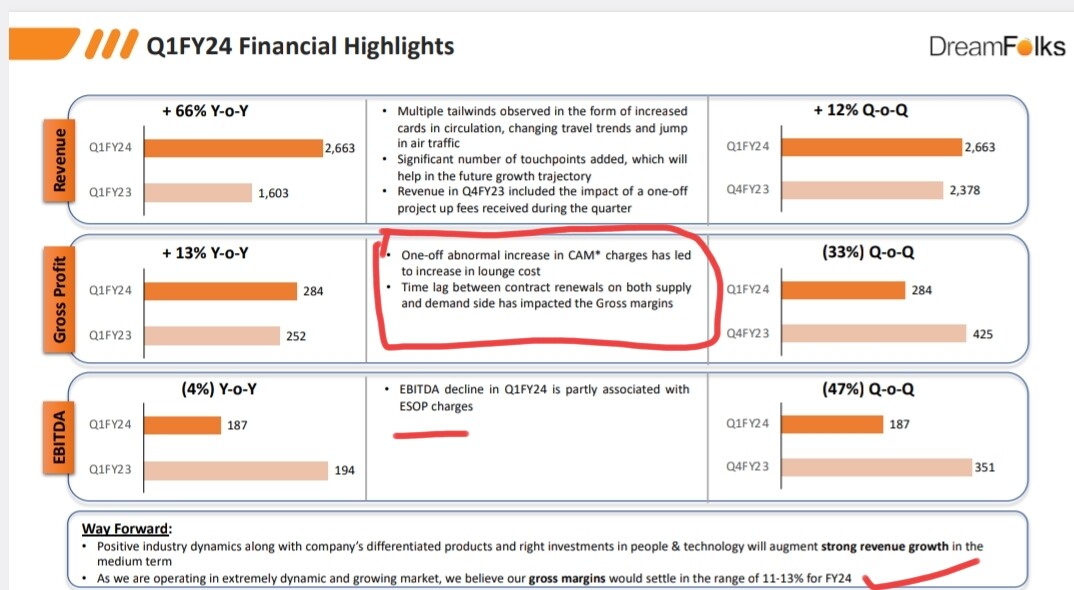

Few things changed in this Qtr. Would encourage everyone to hear the concall. Mgmt commentary around margins were not good. My earlier assumption (guided by mgmt.) was, they can maintain margins and growth of 25-30% in long term. That would have been decent turn of events to make this a wealth generator in long term owing to it’s asset light business model. But mgmt. tone on margins has changed completely in this qtrly call. Although as per them, there are some one off like, CAM (Levies from airport operator to lounge operator for common area maintenance - imagine this to be kind of flat maintenance charges by society). Lounge operators are not in a position to absorb this, as they operate on tight margins. Card issuer’s are also pushing back on costs, as the high growth in footfalls plus inflationary lounge costs have meant a very high outgo from their purse. So Dreamfolks had to absorb some of these costs and are now guiding the margins downwards, from 15% earlier to 11-13% now.

This is not a good turn of events. A better scenario would have been 25-20% growth with margins intact. But things are what they are. So market is rightly correcting the valuation to reflect this new reality.

Disc: Buy/sells in last month. Have reduced position size considerably (only after a losing a part of gains from top.). Might add later.

7 Likes

Dreamfolks revenue grew impressive 66% yoy to 266 Cr in line with rise in air travel in Q1. Gross margins are down to 10% compared to 15% in Q1Fy23 and 18% recorded in Q4Fy23 which is disappointing.

Management highlighted a few reasons for the drop in margins:

- One off abnormal increase in CAM charges(common area maintenance) as airports have increased the charges which are passed on by lounge operators to dreamfolks.

- Time lag in passing on yearly escalation charges from lounge operators to bank/credit card providers.

- Employee expenses/ESOP charges(impact of esop will be 6.3 Cr for the FY.)

- High margin of Q4 was contributed by one off revenue for a lounge consultancy service by dreamfolks.(Management didnt even mention this in Q4)

Generally lounge operators will revise the prices from April which will be passed on to network providers starting from Sept month. This quarter seems to have maximum impact of this and is likely to continue in Q2 as well.

Generally yearly cost escalation which use to 5-8% has gone upto 15% now which is difficult to pass on due to higher than expected footfall of which affects card providers.

As more and more airports gets privatised likely that CAM charges will increase as happened in Q1.

Overall management guided for 11-13% gross margin and topline growth of 50%.

Margins may see some improvement as their revenue from other high margin business like golf services increases meaningfully which is probably few years away.

In my view gross margins unlikely to improve even for the next year. Why will lounge operators /network providers offer higher margins again once they make dreamfolks work by accepting 10-12% margins?

Discl: I have sold dreamfolks today except tracking quantity.

10 Likes

Food for thought:

- Which is good, revenues increase by 60% and margin at 12%? or revenue increase by 30% and margin at 14%?

- Promoters have skin in the game. All employees are given ESOP, What they will do?

Market gave knee jerk reaction to margin erosion, will margin not revert? 2nd level thinking.

Disclosure: Invested

3 Likes

The second option is better. We have to look at the source of revenue. Imagine being a credit/debit card issuer who is paying the lounge bill. I have a budget for sale & promotion/marketing expenses. I may have a set %age of revenue or profit to give away under this head. Let’s say i budget 5/100 as my budget. Now suddenly i have to give 8/100 (with 60% growth). How do i budget this when my income may be growing at say 20-25% ?

So if my income becomes 120 then it’s easy to budget 6/120. But budgeting for 8/120 is a bigger ask and goes out of my budget. I may not care about whether dreamfolks makes 15 or 11 % gross margins as long as it’s my budget and inline with my core business growth. But if year on year my business is growing only at 20-25% how can I afford/budget growth in this payout at 60% ? It’s un realistic. So pushback is natural, first in terms of margins, then in terms of other means of restricting this growth by offering to only higher spend customers etc… but i’ll do everything to keep it in sync with my business growth.

What has happened in this qtr is bad for Dreamfolks from one permanent damage angle. In long run, the dreamfolks business simply can’t grow at double the rate than that of it’s sponsors. But the margin damage will take a lot to reverse, because now sponsor has tasted blood and knows that dreamfolks need not make 15% gross margins to make good money.

But having said all this, i think at some price, market will realize that this is a good asset light business for a 25% kind of earning growth in longer term. The business model is not bust, just some corrections in the expectations.

6 Likes

Business model is essentially same.

Some of these aspects have been discussed in last 3 concalls already. I believe even dreamfolks will grow double digit for next few years, The business model is intact.

The street expects all banks to significantly grow their Retail book. Within retail the expectation is that yields will improve. That is where Credit Cards play a big role. With the surge in UPI which is essentially a competition to CC, banks are under tremendous pressure to protect and grow their CC. In such a scenario, they will only have higher budgets to meet the objectives going forward.

Coming to the point on permanent damage to Margins. Will it be possible for banks to get a competitor to hit margins of Dreamfolks and negotiate better ? We know that Dreamfolks is getting access to card specific details from banks and any breach can have regulatory implications. So will banks trust this to a new player to save some margin ? Would doubt it.

In fact basis multiple new Airports coming up and Lounges becoming a possibility in many Railway stations, the growth opportunity is significant. The YoY growth of 60% confirms that. As long as the topline keeps growing, I would not be worried.

Disc : Invested with average acquisition price lower than current levels

7 Likes

rajpanda Dragonpass and Priority Pass are coving most of the world and their customers are lets say mostly from developed countries (banks).

Simply put, I live in UAE, Where banks pay many times approx. 10000rs to customer (as points,cashback etc.)

Now once customer is on board, they have simply have 3 to 4 times revenues then per customer in India due to currency, exchange rate etc.

Many cards charge approx. 15000 rs. per year to credit card holders, so they are in better shape to pay to priority pass and dragon pass.

Disclosure: Invested and adding in correction.

3 Likes

We are not looking in a broader vision. What additional synergy platinum plaza will bring. Earnings will increase only question is how it will be valied now

2 Likes

Here are my observations form the concall

-

CAMs costs are not one off , these are continuous cost escalations which will happen every year, and DF wont be able to pass it on to their clients entirely, they lied in their presentation when they stated that the costs are “one off” , the lounges are squeezed by the airport owners , asking the lounges to share the revenue (not profits) and inturn the lounges are cutting the DFs margins

-

Last year they got a one time consultation fees due to which their margins increased by 2.5 to 3% and this is a “one off” , which they didn’t disclose then , now they are caught with their pants down

-

Did I hear 6 crores yearly ESOPS charges , where Operating profits are at 18 crores?

Their business is great no doubt but they are not truthful abt many things

As far as lounging in golf course is concerned, they wont get even 0.1% footfall of that of airport, very niche and very small

Railway lounges is a great channel, but with govt controlling them I don’t know if lounges could ever make any money atall.

12 Likes