When icici and axis Bank cancelled the contract, company informed that it will be having material impact on their revenue. But company haven’t disclosed yet how much impact is anticipated. I guess we can get exact picture either in their earning call or in next quarterly results.

1 Like

Really liked the business model- something simple. Although today’s earnings (Q126) results have been positive, but the business moat is slowly fading away. Once a monopoly in this segment with no such airport lounge operators. Now faces threats from Adani, GMR. I wonder how the additional non-lounge services will make up/contribute to the topline of the company.

At last- the moat was like an open honey jar, any airline operator/airport operator could come in and take the honey. As an investor trying to find value, this is a good company to study. It gives a good sense of understanding of moats.

3 Likes

The real picture is still balance, we see those numbers in Q2 results.

Still management is trying to cheat investors by not disclosing the exact impact on revenue due to loss of major 2 clients. I strongly believe that these impact numbers are readily available in hand with the management.

Management behavior is not yet changed even after loosing such a value in Mcap. Still there is lot of risk left in the business as other banks also starts moving slowly from DFS to Airport operators

3 Likes

Have been pointing out the risks for long time !!

Have been proven right.

FIIs have exited. Most DIIs have exited. So it proves they are not the smartest investors. even small investors can be right.

What still remains a mystery is how is the results are still good inspite of all challenges they are facing.

2 Likes

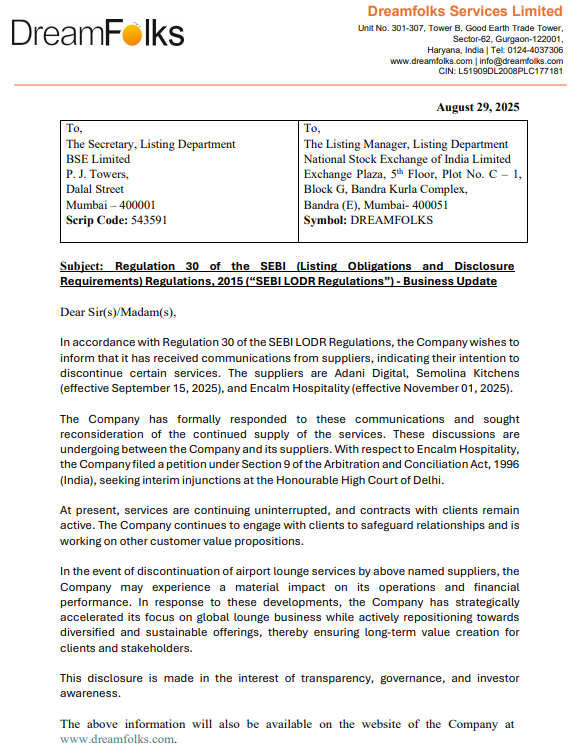

Adani to end partnership with Dreamfolks w.e.f September 15, Encalm from November 1st.

3 Likes

Well well well. India Airports contributed around 90% of the revenues for the company. And now that’s gone, like a fugazi. “You know what a fugazi is? It’s a wazi it’s a wuzi it’s a psh psh psh like it’s not even there.” - Wolf of Wall Street.

As I see it, other services provided by the company are not really value additive per se. Foreign airports market sure could boost sales after some time. Competition and scalability could act as a concern.

There’s really no growth driver going ahead.

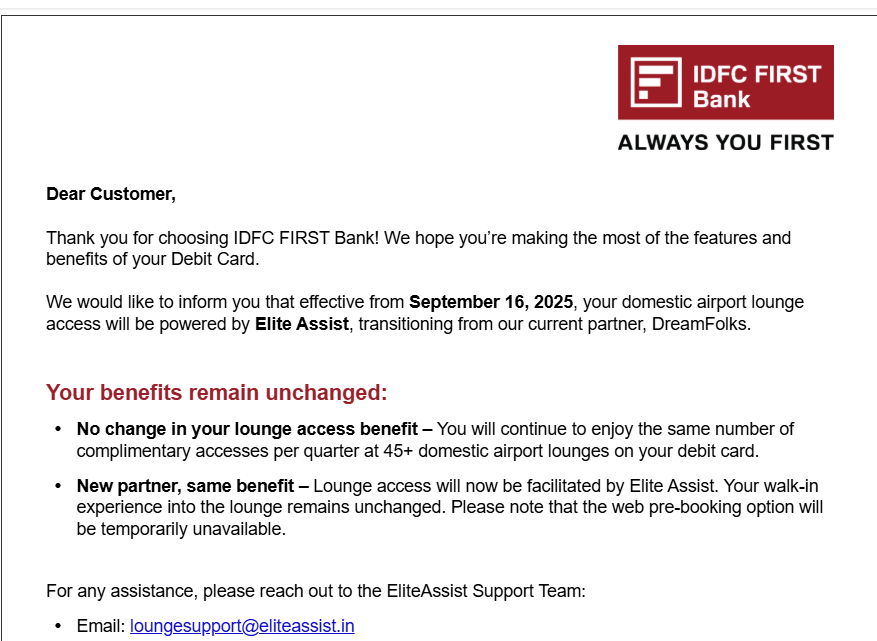

The CFO of Adani Airports posted on his LinkedIn account that now due to advanced Fintech, there’s not really any need for intermediaries like Dreamfolks.

Acquisition of the company is a possibility for sure. Now more than ever. But I am not really sure, the acquisition would provide any value. It will be more of a “This thing is available at fire sale prices, I have loads of cash, nothing to do this weekend, let’s buy an Indian listed company”.

Dreamfolks will be an interesting company to track. Especially if the market cap goes below 350 crores.

Disc: Not invested

thats like the final nail in the coffin, anyone still holding ? Hoping for a miraculous Turn around !

1 Like

This is certainly a major setback, but it’s not the end of the world for Dreamfolks. Even in the worst-case scenario where the company loses 70–80% of its current revenue, it can still generate ₹250–300 crores annually through its international lounge operations and other business segments. The impact essentially pushes the company back by about five years in terms of growth trajectory, rather than wiping it out entirely.

It is still possible to generate a decent 15% ROCE, Debt free company, clean management, hopes are still on for a come back.

While the near term looks challenging, there is room for recovery if the company can adapt and implement a sound strategy. For now, it’s just a matter of wait and watch to see where the stock price stabilizes and how management positions the business for a turnaround.

Already warned last year, who knows Librata completed some under the table deal. This is a sinking ship, stay away.

2 Likes

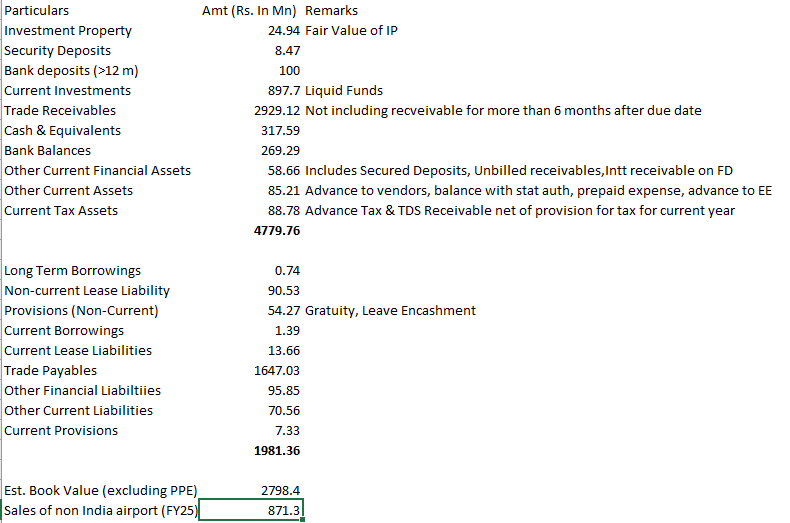

All values as at 31 March, 2025

Paying anything more than 300 crores (3000) million would not be feasible in my opinion. Especially since this business has ZERO TERMINAL VALUE.

90% revenues has been evaporated. It will be a herculean task to find alternate ways to recover these lost sales. Can the company achieve the perfect week [Credits: Barney Stinson (A.K.A. Swarley)]? (5 consecutive days of lower circuits)

Anyways learnings from this saga is pretty simple to me: “Monopoly in trading turds is still useless as the business itself is of trading turds” - Not Charlie Munger

Disc: Was neither invested nor interested. Am now interested.

2 Likes

Like @kautuk am also - Was neither invested nor interested. Am now interested. Just gone through whole thread and ppt and ar etc.

Net cash as per AR is 30 cr

As per CNBC - https://www.youtube.com/watch?v=9oQ8l6Xz8pw

Lounge business 93% and non lounge is 7%. Out of 93% domestic is 77% and remaining 23% is international.

FY 25 revenue 1292 cr.

Revenue of FY

Domestic lounge (77% of total) = 996 crore will be 0.

International lounge (23% of lounge = ~21.4% of total) = 276 crore

Non-lounge (7%) = 91 crore

Total Fy 26 revenue will be 276+91 = 367 cr.

Their OPM margin is 8% hence OPM is 30 Cr and same is their PAT.

If co gets 20 PE

Market Cap=30×20=₹600 cr

Current market cap is 630 cr.

This is just back of envelop calculation, suggest if I have missed anything?

Note: Their manpower cost is 3% of FY 25 revenue, as they have not anouced layoff, it will be little higher in % of FY 26 revenue. But ignored in my calculation.

No data is available for PAT margin of non lounge and international lounge business, will change calculation as and when data is available.

4 Likes

Hi!

In my humble opinion, this business has zero terminal value. 0 exit multiple. Why? For starters there’s no plant or machinery to dispose off. Next, the business model is such that it does not demand a terminal value.

I think of it from the point of view of a buyer firm. Why will I pay 600 crores for a company making 20 crores of profits annually, when the model is so easily replicable. Why not just hire a bunch of software engineers instead. Dreamfolks doesn’t offer me any qualities that justifies paying 20 times earnings. There is no brand loyalty, there is no intellectual property, no established client base (since the clients are limited), no pricing power and no distinguished or value additive service. The most I will pay for this company as an acquirer is the fair value of assets - Fair value of liabilities.

Heck I would even pay less than that because I know they don’t have any other option. It’s a distressed sale.

Plus there is huge competitive intensity. Not to mention the looming backwards integration threat where banks directly co-operate with the lounge operator.

I probably shouldn’t say this but anything above 300 crores M.cap is a value trap.

Good day and Thank you for your attention to this matter! (Ifykyk)

8 Likes

Can someone explain if their International lounge business is also vulnerable to backwards integration? Why can’t International airport replicate what Adani did and disrupt that stream of revenue as well?

Disc: Interested due to recent developments

1 Like

In my opinion not much risk to international business as Banks need to on board lot of lounge operators to inorder to replace DFS.

In india there are only few operators, who are dominating the lounge operation so its easy for banks to deal with them. Its not the case with international business.

With the switchover, now power shifted from the banks to lounge operators. There is no negotiation power left with the banks as they are compelled to shift from DFS & they obeyed the same.

1 Like

Dreamfolks hit the upper circuit today. I wonder who took delivery of shares worth ₹9 crore

I am honestly amazed at the continued interest in a company whose basic business model itself has collapsed! Optimism cannot be an investing strategy!

There are plenty of actually interesting businesses out there, aren’t there?

Am I missing something?

7 Likes

1 Like

So all FII and DII have exited - Nil. only retail investors remain.

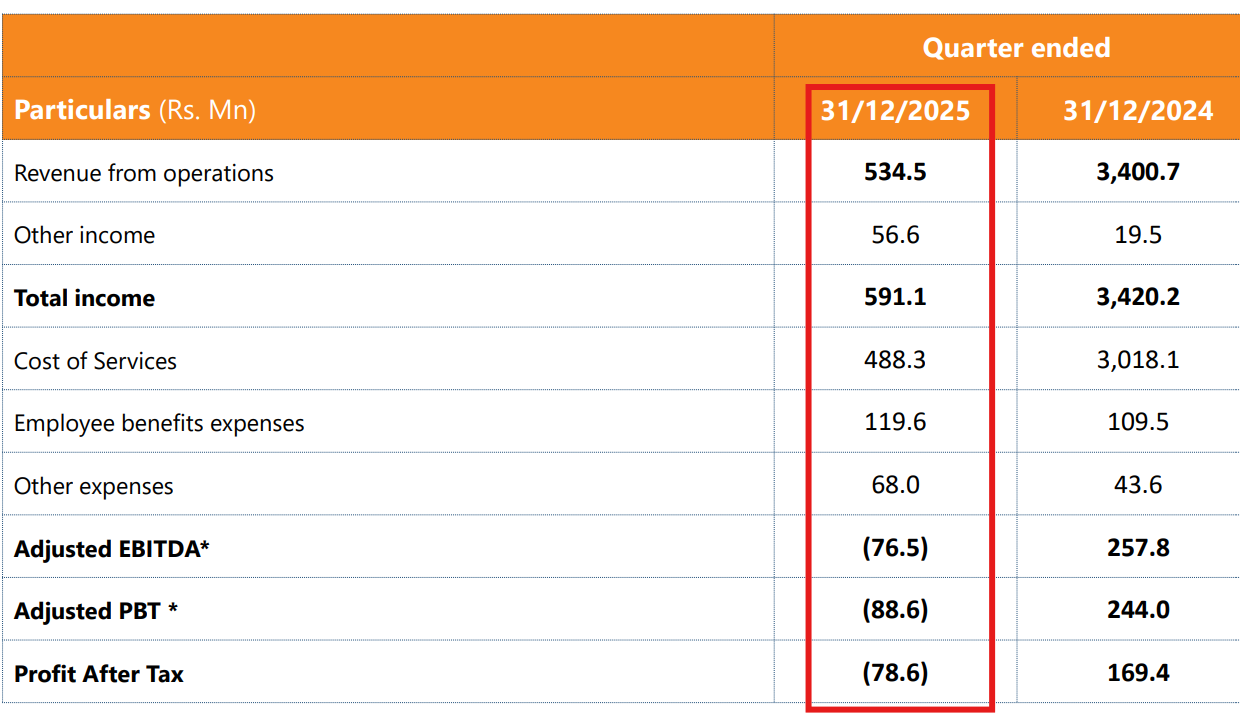

Sep quarter results also have declined.

Retail investors have got stuck in this company. Wont be surprised if stock goes down by 50%.

2 Likes

Now real picture is visible in the Q3 numbers. Q3 numbers are hidden in the 2nd last page of presentation. How badly retailers stucked in the company, whereas MF’s & FII’s existed completely in 3-4 quarters.

They may post losses for 2 or 3 (or >3) quarters again before hitting breakeven. There are hardly anyone available in the call to ask questions. 100k retailers parked their money thinking that it will grow automatically.

I wish the re entry time will come for sure, when they win some sizable deals in SEA & ME countries and railway lounge business starts running.

International deals will take long period for conclusion, they are not able to close a single deal since listing but they may able close 1 or 2 deals in coming 2-3 quarters as they are in crisis now.

Railway lounge would take long time to contribute decent amount to top line as there are only few lounges available in india and Pax rate would be 200-300/- as compared to > 1000-1500/- in airport lounge business.

Its a wait and watch situation now.

2 Likes