Just mentioning that I had exited in the start of the year due to lost patience & negligible profit growth.

Would not recommend even in top 200 stocks list.

2 Likes

The share price collapsed 11% today to below 300 levels. Any rationale as to why?

Have been pointing out the risks for long time !!

Results seem to be a drag again with margin going down further but did not seem to be a howler kind of numbers. Its been a significant fall ~25% and its coincided with markets falling in general so not sure if its result, sentiment, combination of both or something else cooking inside? FII’s, DII’s and promoter have reduced stake. Does it indicate that a more structural issue is brewing with the model which participants are not being made aware of?

Any views or knowledge of what could be leading to such a big fall for something which was already down significantly?

I’m invested in this. Though I’m not 100% bullish on this, I’m not as bearish as the market says. I think this company would still be a long-term wealth builder.

Yes, margins went down, which was mostly because of card companies reducing the benefits given to its customers. Apart from that company is also adding more workforce.

Having said these, my thought is, the value of this company would go higher as more parties are added to their network. Simply said, network effect(think netflix, ola/uber etc) will come into play. This is exactly what the company has been doing. Today, they are a monopoly business only in India. While they are working to go beyond India, they are also working to entrench it firmly in India, by offering related services.

Quote from their Q3FY25 Investor presentation:

“The company has expanded its service offerings with new services like Baggage Wrapping, Coffee at Malls, addition of 9 F&B outlets, and 2 airport lounges in India. We have welcomed multiple enterprise and banking clients, with some transitioning from competitors. Our global expansion includes 16 new global lounges, 18 F&B outlets and extended M&A services across 380+ airport terminals.”

Some related notes from the book “Zero to One”:

- Prioritize four aspects of your business over a hyper-focus on growth: proprietary technology, network effects, economies of scale, and branding.

- Rather than initially painting a grandiose vision of global market dominance, the best way to build a monopoly is to start small. Capture a small, specific market with the tentacles to easily branch to related markets over time.

9 Likes

I feel correction is because of some more selling after results commentary.

Card issuers are keep on increasing the eligible spending criteria amount every time to get the free lounge access.

This will impact the number of cards in circulation also, earlier people used to maintain as many card as they want to have more number free lounge accesses. Now its not about maintaining more cards, its all about spending more on cards.

This will ultimately results in some foot fall drop in the lounges, now company stopped reporting the number of pax availed lounge access.

Management is also very tricky and they don’t give any straight forward answers. In this Quarter call, they ended the call in 45 min even people are in queue for asking questions, they unnecessarily wasting 30 min time in opening remarks by 4 people ( content would be same from all 4 people).

14 Likes

Your observation about the handling of the concall is spot on, for the companies when they have nothing to show as performance. Management will come on call and will spend more than 50% of the time talking about all things… except what went wrong during the quarter and then they cut short the concall due to paucity of time…

Now a days , that’s a clear red flag for me and if thing dont improve in quarter or two, its time to exit for me. I could have saved lot of pain for myself if I would have known this earlier

Disclosure - not invested, not interested

9 Likes

It seems the credit card companies are controlling their business. The harder the pain for card companies more fall we will see from this level too.

I agree also their operating profit to cashflow conversion is not so good as compared to other platform companies. With high receivables days & thin margins it seems they don’t have that kind of bargaining power with its buyers.

1 Like

With all these negative points price is getting corrected and now available at 20 PE multiples of FY25 and looks very attractive with anticipation of 20% growth going forward.

If they can crack any international deal then it would be must buy signal

2 Likes

Yes its 20 PE Stock now with 35 plus ROE and growing decently and they are launching more services for premium customers in India. If Promoters are not Fraud this stock looks to be very attracting at this price…

2 Likes

Company depends on two parameters for growth i.e Air traffic and Credit Card consumption

Expected Air traffic growth for FY26 as per analyst is ~10% while Credit Card/loans at ~13%

In the past company has outperformed the growth in these two segements, hence Revenue in the range of ~15-20% is expected, and with company current multiples of 20 looks a decent buy, if not for very long term but for a year or so.

Also note, all EBITA is translated into PAT due to hardly any expenses, hence, PAT can grow at a very fast pace.

Note- Not holding, but planning to add. Not a SEBI registed advisor

2 Likes

This is only the trick here, as we have seen in 2023 Margins fell from 13% to 8% due to change in airport rentals.

Even though DFS doesn’t have any direct exposure with the airport rentals, they need to take hit on their margins to protect the lounge operators as there is no power in the business. They are unable to protect their margins, this can happen in the future also.

I am much happy if PAT growth at the same rate like top line without any further dip in the margins

2 Likes

With the ongoing modernization and upgradation of railway stations in India, along with the increasing number of railway lounges, does anyone have an idea of what percentage of revenues currently comes from the railway lounge service business? Additionally, considering these developments, how much revenue can a company operating in this space potentially earn in the next 5-6 years?

2 Likes

Railway lounge contribution is very less, infact management never shared any number. Adding railway lounges may not make much impact as per pax cost of railway lounge is 1/4th or 1/5th of the airport lounge per pax cost.

2 Likes

There has been a recent news,

HDFC Bank have stopped giving free Lounge Access to every user. The new Benchmark that has been set 50,000. If on quarterly basis, you are spending this much amount, then only you would be abe to access free Lounge.

This is a Major Set Back, followinn this each and every card providor may do this.

The Link to the News Article:-

3 Likes

We may thus spending criteria to increase further, I think few banks already set 75k minimum spending criteria also.

3 Likes

All these tweets seem oddly similar — repeating the same phrases and tone. It’s either a coordinated smear campaign or possibly AI-generated content.

Anyway, would think twice before taking these accounts seriously now onwards.

Disc: Holding.

19 Likes

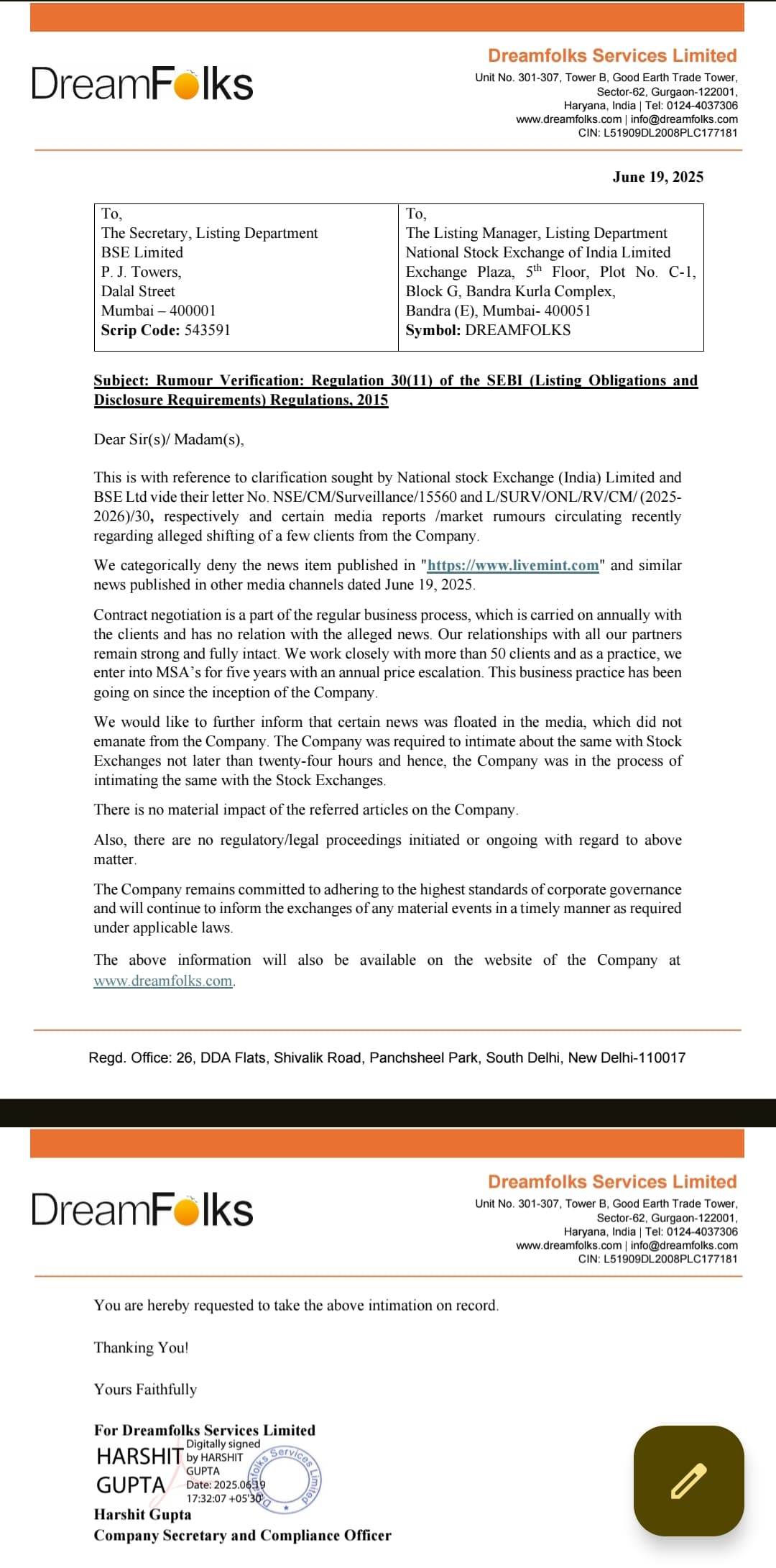

Clarification by the company.

Seems some shady tactics used by either competitor, clients or vested media houses.

4 Likes

This is exactly what SEBI needs to investigate .. PUMP AND DUMP AND DUMP AND PUMP both hurt investors. It’s obvious to all that there is corruption but will SEBI even look at it. Same thing happens to IEX . Operators have been bringing goverment officials to make untimely statements,likely for some benefits, , and nothing follows. 8 times they have crashed IEX shares so far based on one policy document that has not seen the light of day despite IEX MD saying it will never be implemented.

Dreamfolks is a target and this will keep happening as they can easily be hit with such news as it’s a simple product tech firm and operators are going to play with it with fake news . Hope SEBI traces who sold the 24L shares yesterday and does a detailed forensic.. till operators fear investors are not safe. See the news on Ahmedabad based 300 cr racket

13 Likes