Key Summary:

For a business like this margins and inventory turn over are key factors to watch for. Unlike Titan, the management at DPAL are concentrating more on inventory turn over rather than margins which is giving them excellent ROEs so far.

The growth prospects are based on - To achieve a same-store sales growth for new stores. Company plans to open 2 showrooms with a potential of 200 crs topline every year; with a 50% utilization in 1st year and 100% utilization in next year onwards. Turnover is expected from 1700 crs to 3000 crs.

Moat being: Natural hedging (covered in detail below), golden locker scheme, focused region and low operating costs. Brand specific moats are quality products, high customer satisfaction, brand recall, etc.

My focus areas (detailed below) are: Inventory turn over & margin analysis, prudent debt allocation, covid disruptions, cash flow from operations, future expansions.

In this post I have not much touched upon the sector dynamics as those are already discussed in other jewellers posts (Thangamayil Jewellery).

Background of company:

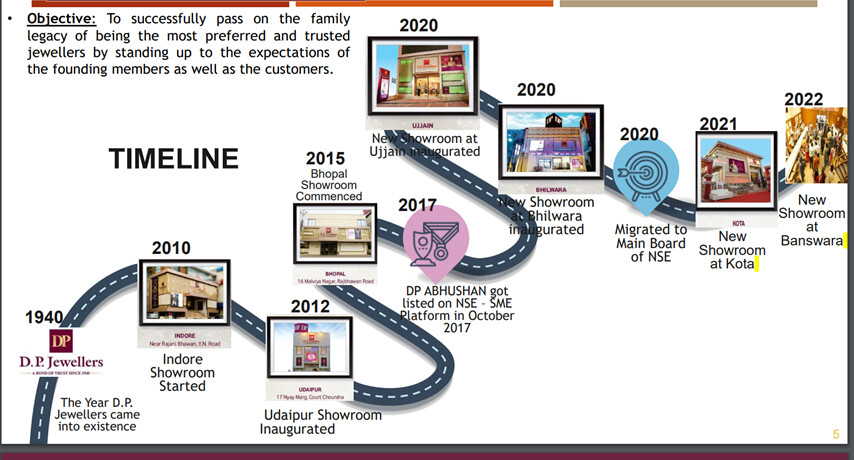

DP Jewellers is family driven (now 4th generation) business engaged into the retail of Gold and Diamond Jewellery & Ornaments. The journey began in 1940 from Ratlam a small city of Madhya Pradesh. Today the Company has grown largely in Central India with presence at 8 stores Ratlam, Indore, Udaipur, Bhopal, Ujjain, Bhilwara, Kota and Banswara.

Janam Kundli of company as follows:

The company got listed in NSE – SME Platform in 2017 with market cap of Rs 62 crs but got shifted to main board with market cap of Rs 867 crs now.

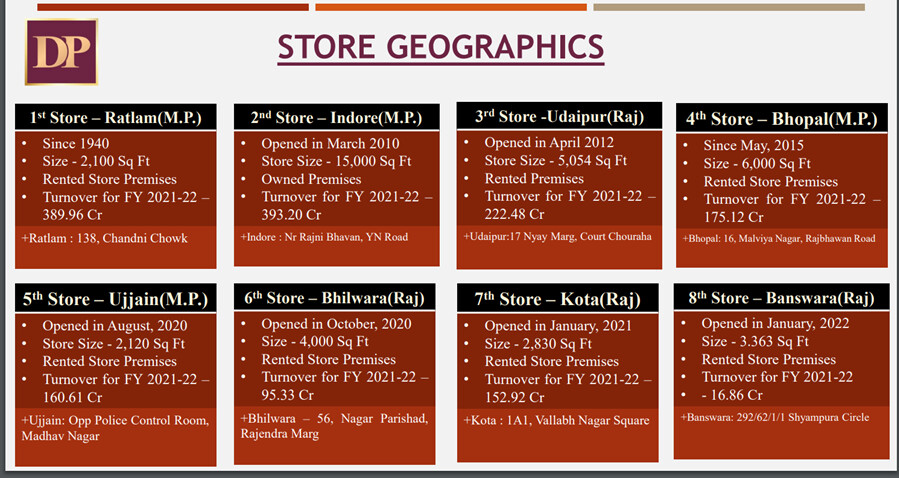

*Bio-data of Stores:

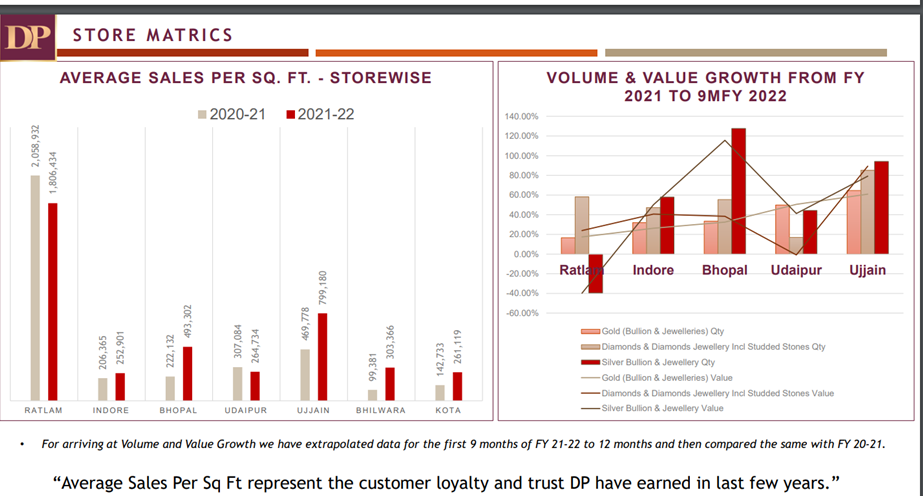

Please note that the store matrix should not be strictly compared with each other because of difference in age of stores.

Products:

Necklaces, Rings, Chains, Bangles, Pendants, Earrings, Armlets, Gajrahs, Nose Rings, Mangal sutra

Collections:

Wedding jewellery, Traditional Jewellery, Valentine Jewellery, Lightweight and trendy jewelry, Flower Collection, Idol Collection, Dohra Collection, Mewar Collection

Styles:

Gold jewellery, Diamond studded jewellery, Precious and semi-precious stone studded jewellery, Plain and diamond studded platinum jewellery, Jadau Jewellery, Jewellery with colored stones in gold and diamond

Inventory Turn over ratio:

Particulars 2018 2019 2020 2021 2022

Inventory Days 81.8 74.8 93.6 82.4 73.86

Inventory Turnover

Ratio 4.5 4.9 3.9 4.4 4.94

Total Asset Turnover

Ratio 3.4 3.8 3.2 3.7 4.19

ROE 19.8 25.1 27.2 28.26 29.29

EBIDTA Margin 3.3 3.4 4.3 4.2 4.34

PAT Margin 1.2 1.5 2.1 2.25 2.34

As seen Inventory Turnovers are best in sector at 4-5. For Thangamayil Jewellery and Titan it is 2 – 3.

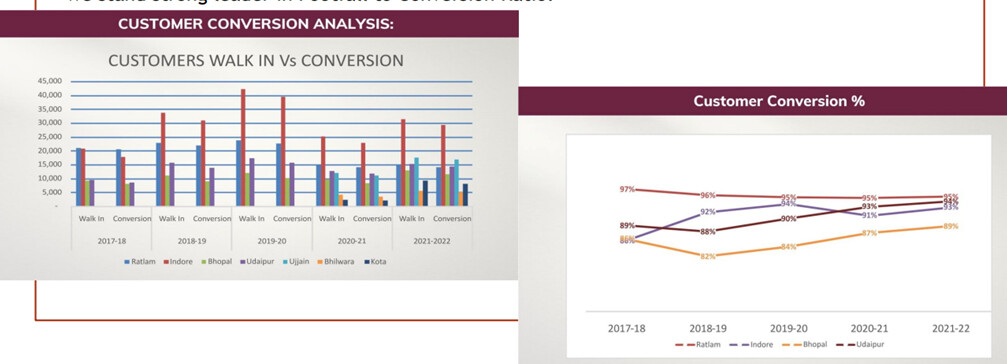

The footfall conversion (proxy of inventory turnover) is as follows:

Margins:

PAT margins slowly but steadily improving but are still at ~ 2%. For Thangamayil Jewellery is it 2% and for Titan it is 7%. Obviously Titan margins cannot be strictly compared with DPAL but still mentioning just for reference.

In one of the concall recordings, I heard management saying that while they are cognizant of low margins but their main focus is footfall conversion and will take adequate steps to increase margins.

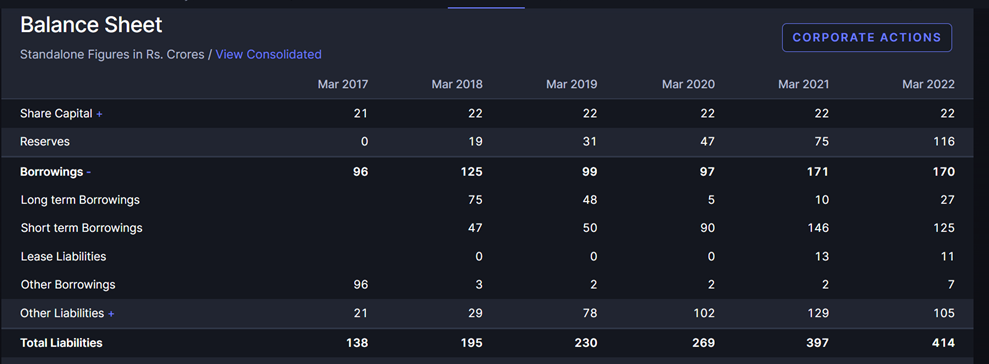

Debt:

Debt has remained double edged sword businesses like this. It takes stringent efforts for promoter driven business maintain financial discipline. While capital intensive business like this will need debt but balance has to be maintained. As can be seen from screenshot above DPAL has significant debt making D/E more than one and this needs to be monitored closely.

In one of the concall a participant was asking whether promoters would be keen explore institutional funding. So I guess they have easy access to funds, its just that I hope they don’t overdo it.

Covid disruptions and comments on H1FY21 result:

In the backdrop of Covid related lockdown, company’s store were almost shut in April and May month, while some recovery was seen from June month onwards with encouraging footfalls. DPAL’s net revenue declined by 37% YoY to Rs 2,137 mn as volume across products declined. Gold jewellery/Diamond jewellery volumes declined by 59%/39% respectively.

Despite sharp de-growth in top-line, DPAL managed to salvage margins led by lower cost of sales. Gross margin of the company increased sharply from 8.3% in H1FY20 to 13.9% in H1FY21. Material cost as a percentage of sales decreased to 86% from 92% YoY. EBITDA during H1FY21 grew by 31% YoY to Rs 186 mn while EBITDA margin expanded sharply by 451 bps YoY to 8.7%. Profit during H1FY21 grew by 53% YoY to Rs 103 mn largely due to better operating profit growth.

Cashflow from operations (kyuki bhaiya sabse bada rupaiya):

CFOs are erratic and the only reason I could attritute is: (1) Covid lockdown and (2) Lot of inventory is tied up in new stores whose operating leverage is yet to kick in.

GROWTH PROSPECTS:

• The Company expects to achieve a same-store sales growth of around 22% for the upcoming years on the basis of past performance and future growth. Company plans to open 2 showrooms with a potential of 200 crs topline every year; with a 50% utilization in 1st year and 100% utilization in next year onwards

• Stores would be opened from internal accrual and gold obtained under the various Schemes as well as external debt when required. The Company envisages an outlay of around 25-30 crs per store for CAPEX and inventory

• The Company plans to deepen its roots in Central India by entering into the states of Chhattisgarh and Gujarat and expanding its feet in M.P. and Rajasthan that would drive economies of scale

• The Company’s stores enjoy faster breakeven of around 4-6 months; because of faster inventory turns of the Company and low CAPEX, as well as low marketing cost

• Since Offices & showrooms are located in tier 2 & 3 cities, staff cost is low, and optimum utilization of resources is done, Company plans to run on same model in future.

• 2025 Targets: From 8 to 13 stores and Turnover from 1700 crs to 3000 crs.

MOAT: WHAT MAKES D.P. ABHUSHAN DIFFERENT

NATURAL HEDGING: The Company has got natural benefits of Hedging because it follows a weighted average cost method i.e. buy-equivalent quantity of goods sold at the day of the sale itself. The Company is following this method since inception so its cost of inventory is remains lower than the current market price.

There was detailed discussion on this in one of the concall wherein the promoters explained why their hedging process is different and beneficial than hedging of large players like Titan.

GOLDEN LOCKER SCHEME: The Company has implemented a old gold locker scheme policy where it replaces customers old inventory with new inventory after 11 months without or with concessional making charges which is a unique proposition across Central India

FOCUSED REGION: The Company is more focused on gold jewellery as the Central Indian market is more inclined to gold Jewellery. Moreover, the promoters have knack of understanding customer behaviors in their target markets leading to higher conversion ratio.

LOWER OPERATING COST: The Company operates in tier 2 & tier 3 cities hence its making and operating expenses are lower. Also the logistics movement of Inventory is easy and economical among these cities.

Strengths:

• High brand recall being in existence for more than 80 years

• The Company is following BIS criteria since the inception of DP

Weakness:

• Any regulatory change in government policy that can affect the business

Opportunity:

• Plans to enter into Chhattisgarh and Gujarat and to expand in existing States by opening 2-3 Stores every year

• Shifting of Jewellery Business from unorganized to organized Sector with an implementation of mandatory hallmarking.

Threats:

• The Company doesn’t see any potential threat that exists, as it is very good at its craft, however, increased competition from other players can cause a threat.

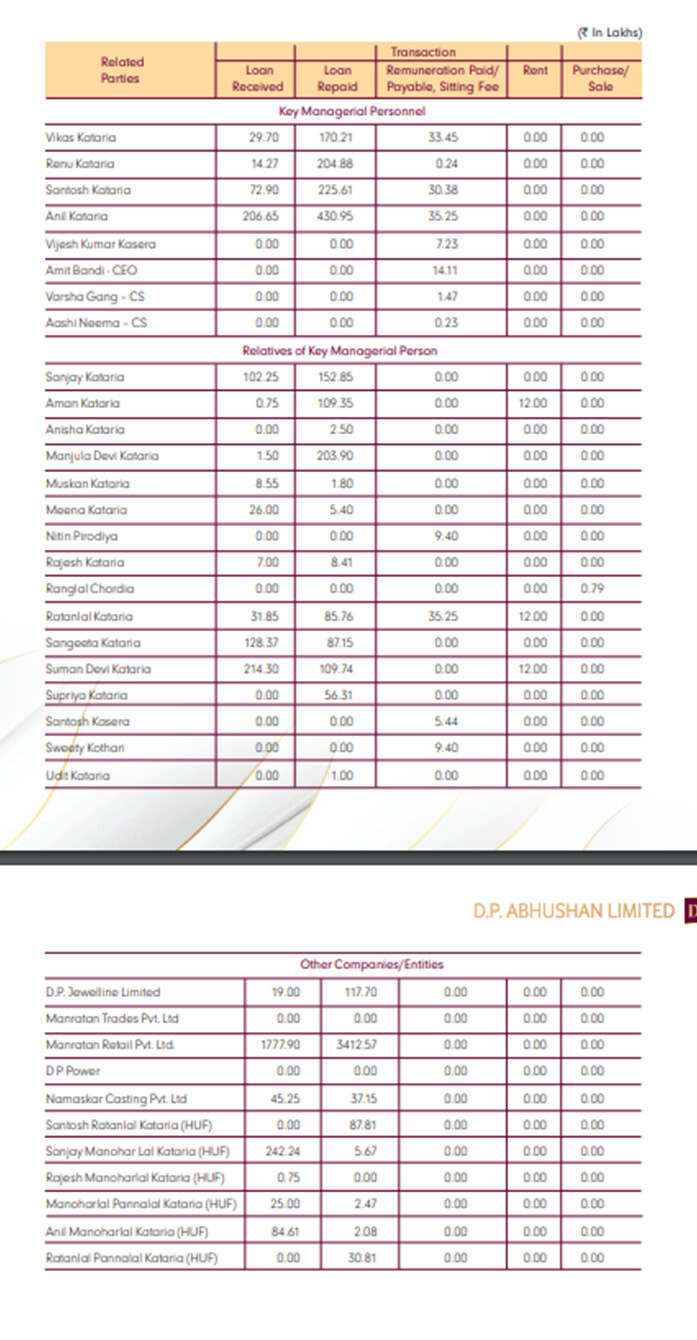

Related party transactions:

Just like typical SME we have unfortunately loans to/from promoters to deep dive into. I had sent an email about detailed terms and conditions for this but have not got any reply yet.

Some extra gyaan:

-

Wind Power

The Co. had 5 wind turbine generators of 750 KW each in the village Bagia & Naveli, Ratlam, Madhya Pradesh. During FY21, the co. sold the business of Windmill to M/s D.P. Power against the consideration of Rs. 5.1 crores along with all assets and liabilities thereto on a slump sale basis. -

Subsidiary

D.P.Jewelline (formerly Gatha Trendz) has been incorporated as a wholly-owned subsidiary of the Company for carrying out the business of jewellery on e-commerce platforms to cater for the small ticket size of jewellery and gift products made out of gold, diamond and silver. In FY22, the Company sold its entire holding to related parties. Management avoided question on this in concall. -

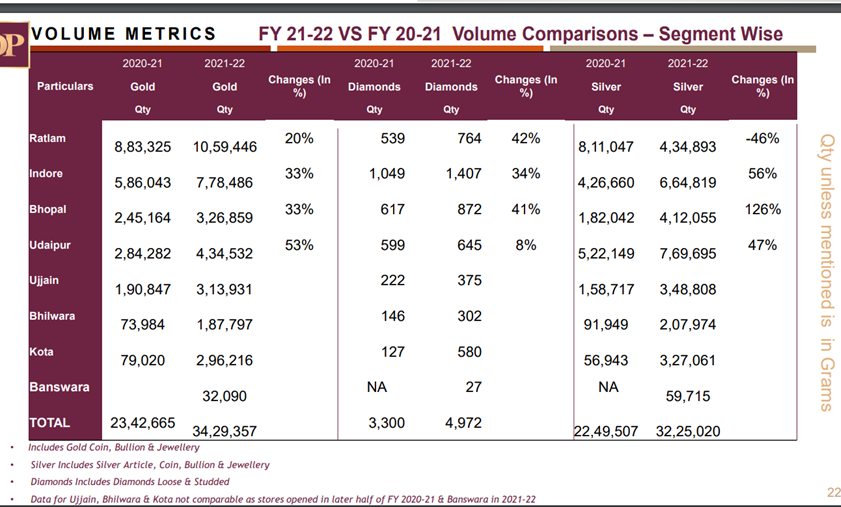

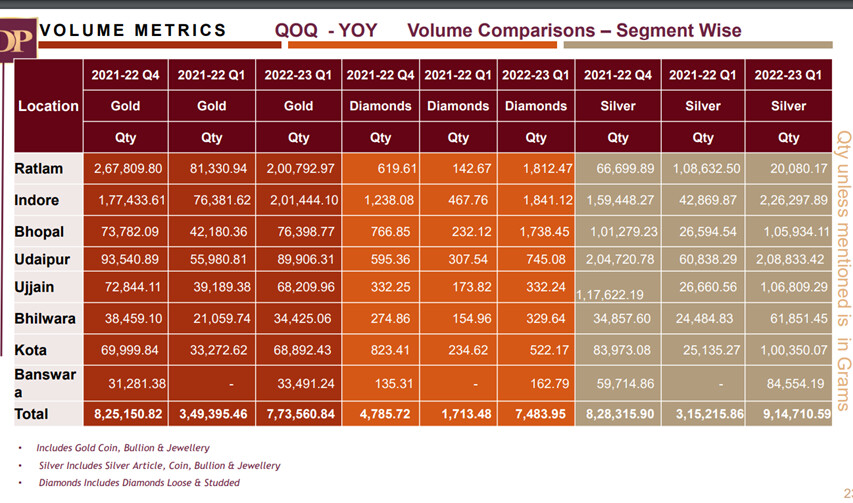

Volume metrics analysis for any Soniji here:

Disc: Not a registered analyst. Invested and biased.