Dolphin Offshore Enterprises- A friend suggested to look at this company. Here is a summary of what the company does and the business it is in.

Dolphin was started in 1979 by an ex Naval Officer and his son. It started with providing underwater diving services to ONGC. It slowly moved up and today offers EPC services in the brownfield offshore segment.

EPC Segment (Standalone operations)- In this segment it plays only in the brownfield offshore segment. It tried to expand in the green field category but didn’t do well. In this category, ONGC is their only customer. They either directly work with ONGC or work indirectly as a sub-contractor for ONGC. This segment is plagued with lot of problems:

- High working capital- EPC is a high working capital business. Dolphin Offshore is no exception. The debtor days extend beyond 240 days. With more than 60% of receivables extending beyond 6 months. These returns are actually 1 or more year old and their recovery is a question mark

- Write offs- The business has written off 35 Crores in FY14 in the form of receivables a similar amount was written off in FY09. The company has ~180 Crores of receivables and there may be some write offs from this as well.

![]()

- Single customer- 100% of their revenues are dependent on ONGC. There is a huge customer concentration risk here. Moreover over the last 3 years the company has not bagged any new orders as a result, there the company is facing losses in its EPC business. Moreover, due to the global slowdown in the oil exploration contracts, many global EPC players entered India. This led to fall in margins and also as these EPC players had idle capacity, they outsourced/subcontracted less work outside. Both these affected Dolphin adversely. Since its peak in FY10 it’s revenues have ~ 1/10th and the has moved into losses

Charter Business- While the EPC business is in doldrums, things in its overseas subsidiaries are not as bad. Infact, they are rather good. There are 2 major subsidiaries for Dolphin- DOEMPL (Mauritius) and Dolphin Offshore Shipping. Through these subsidiary it leases and manages vessels for its clients. It owns 3 offshore vessels 1 anchor tugboat and 1 DP Barge. The DP Barge was acquired in Sep’12 and was leased out in Gulf of Mexcio in Oct’12.This part of the business is like a rental business.They get into long/short term contracts. A large part of their revenue is derived from their DP Barge which is now leased in the Gulf of Mexico for 3 years. The boat is on a bareboat charter

which would mean that the margins are very high here. Due to their 3 year contract they have stable revenues and margins expected over the next 3 years.

As per reports - there are very few DP Barges in the world (only 12) and there is a huge demand for DP barges across the world. That was the major reason that they have been able to get a contract extension even amidst low oil prices

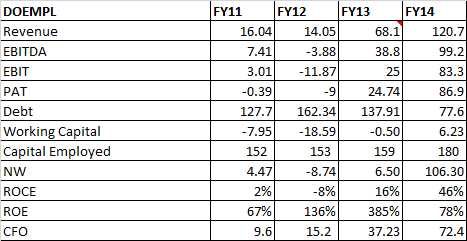

Below is a snapshot of the Mauritius subsidiary’s financials

With clear visibility for revenues, profits and cash flows in its charter business, once can do a simple DCF to value this business. The EPC business is a black box in my view with no visibility of contracts and also no insight into the amount of write offs that could potentially come and hit the company.

The business also has debt - but servicing ability looks ok, given the strong cash flows of the subsidiaries.

The business at present has a market cap of 193 Crores and has a net debt of about 100 Crores. The business is currently trading at an EV/EBITDA of 3, which looks cheap. My valuation of the the charter business comes to be ~ 150 crores without taking any terminal value here (It was difficult to assume the terminal value as I don’t know much about the industry). Assuming a zero terminal value, we are paying ~ 45 Crores for the subsidiary as per current market prices.

While the business looks pretty cheap, but there are many unknowns here and that doesn’t qualify this to be a ‘no brainer’ for me.

Would be great to have other’s views here. If anyone has looked at it.