Dodla Dairy is a south India focused milk player. Installed capacity of 22 LLPD (Lakh Litres of Milk per day) – 19 LLPD in India and 3 LLPD in Africa (Uganda and Kenya). Procurement volume was 13.8 LLPD in FY23 on an average.

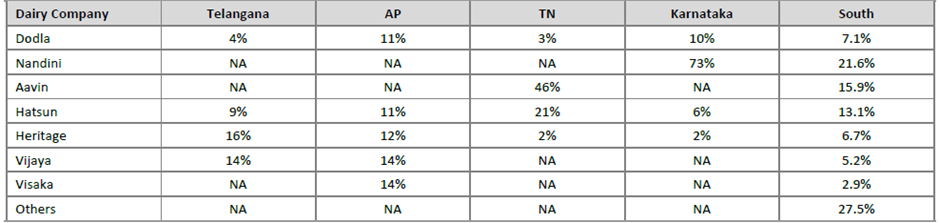

- Procurement is done primarily from 5 states (Andhra Pradesh, followed by Tamil Nadu, Karnataka, Telangana, and Maharashtra) while it is sold in 11 states.

- Presence in Africa (Uganda and Kenya) which are the major milk producing centres in Africa. Company is focused on these markets as margins here are double that of India. Africa is currently 10% of revenues.

- Focus on Value Added Products which was 32% of sales in Q1FY24. 75% of the value added products is contributed by curd and the remaining is divided between ghee, butter, paneer, etc.

Sales Mix

Dodla Dairy got listed in June 2021 at around Rs 425 per share.

Some business economics I could get from their con call and presentations is milk realization in India is Rs 56 per litre and cost is Rs 40. Gross margins of 25-28%. Employee, processing and marketing costs contribute another 15-20% of expenses leading to OPMs of between 7-10%.

The dairy sector went through compressed margins in FY23 which was in turn due to raw material cost increases. This was driven by shortage of milk which in turn was due to cattle disease during that quarters and less cattle due to break of cattle breeding pattern during covid times.

Pros

-

Company has delivered 20% sales value CAGR over the last 20 years. Around 12-14% of that is due to volume increases and the rest is due to pricing increase.

-

Extremely strong WC management. Debtor days has been 1 or 2 days for the last 6 years. Inventory days has ranged between 20-40 days which has been squared off by matching payable days.

-

Has been able to defend market share and premium pricing in Karnataka against co-operatives like Nandini which receives a subsidy of Rs 5-6 / ltr from the state govt. Speaks a lot about their brand positioning and their pricing power.

-

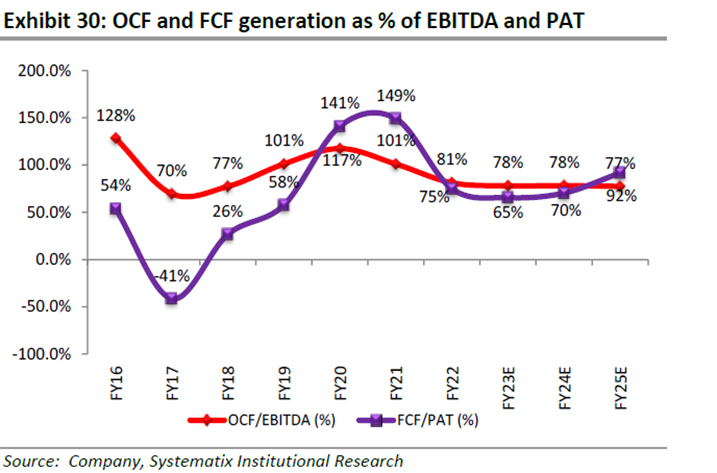

Strong CF conversion business.

-

Favourably placed against peers in industry in terms of size, operating metrics.

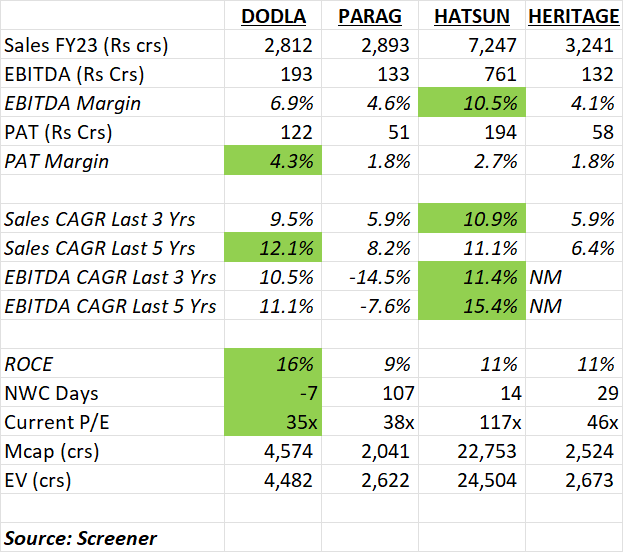

One third the size of Hatsun Agro and similar size as Parag Milk Foods and Heritage Foods. Hatsun Agro and Heritage are both focused on markets in the south while Parag Milk is more focused on north and west.

I fail to understand why peers Hatsun Agro would trade at 117 P/E + others like Heritage Foods is at 42 P/E and Parag Foods at 38 times P/E while Dodla is still at 35 times P/E even after the stock has appreciated by 30% in the last 2 weeks after the results.

-

Company is making use of cash on books by making acquisitions of smaller players in its current markets (KC Dairy – Tamil Nadu market in Apr 2019 for Rs 110 crs and Sri Krishna Milk in Karnataka in March 2022 for Rs 50 crs). Also expanding into Africa (Uganda and Kenya) where margins are double that of in India.

-

Building farmer relationships and backward integration by getting into the supply of cattle feed to farmers (Orgafeeds). Expected to increase capacity by 6x in this business. Could lead to total revenues of Rs 180 crs from feeds. Current revenues is 45 crs from this business.

Cons / Risk

The only con / risk that I could find is that the stock has run up 30% post the results and is currently at 35x TTM P/E. But valuation of similar sized peers gives me comfort that maybe it is still undervalued.

Some reference videos / analysis I found on Tijori finance

- Dairy Sector and Dodla Dairy Stock Analysis | Framework to protect wealth and build wealth - YouTube

- Life After Listing: Ep 06 Dodla Dairy MD, Dodla Sunil Reddy & CEO BVK Reddy - YouTube

Status

Have taken a tracking position (1% of my portfolio) today