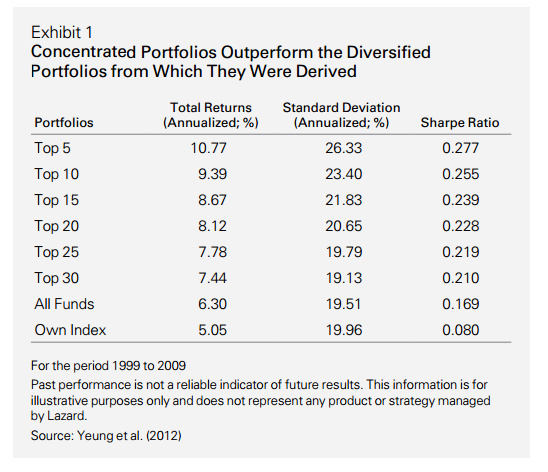

The authors made a case for concentrated portfolio vs diversified portfolios. Authors argue that concentrated portfolios allow portfolio managers to invest only in their best ideas. they back tested their theory and concluded that concentrated portfolios outperform diversified portfolios from which they were derived.

In other words, if a manager creates a concentrated portfolio of anywhere between 5 to 25 stocks out of his/her own diversified portfolio (which in most cases has over 40 to 50 stocks), he will outperform his own portfolio. The explanation provided by the authors is that a portfolio manager does have some good investing ideas but no manager can have 50 good ideas at a time. Other than the top 10 to 20 ideas, rest of the investment ideas are only marginally good. Such marginally ideas dilute the performance of the top ideas resulting in under performance of diversified portfolios. Weight of a stock in a portfolio represents manager’s conviction behind the investment idea.

Intrigued by this research, I performed same analysis on my own portfolio and found that I would have earned a CAGR of 35% on a concentrated portfolio of 10 stocks compared to my actual return of 21% on a diversified portfolio of over 50 stocks over a period of 10 years. Such concentrated portfolio has higher risk than a diversified portfolio but earns a far higher return. Return per unit of risk is higher in a concentrated portfolio than a diversified portfolio.

To test this theory further, I gathered top 10 stocks and their weights for ICICI Pru Value Discovery Fund for last one year and build a virtual portfolio of just these 10 stock keeping their relative weight same as in the original portfolio. I took the data from monthly fact sheets published by the fund. I found that this concentrated portfolio would have outperformed the diversified fund by about 3% in a 3 month, 6 month and 1 year periods.

This is just a litmus test performed on a single fund for a single year but it does validate the theory that concentrated portfolios outperform diversified portfolios from which they were derived.

One of the main argument of the theory is that a manager can have only a handful of good ideas at a time. There are many good funds run by good managers and they all have few ideas each. However, there is not much overlap between their high conviction ideas. i.e. if you analyze top 5 stocks of 5 to 10 different diversified funds, you are likely to get 20-40 good ideas. thus a portfolio of 20 to 40 best ideas from multiple funds can be constructed that is supposed to outperform even the top performing funds while keeping the risks low. I have to try that next.

I am posting this to get opinions of VPs on this theory.

This goes back to the diversification vs concentration debate. Having 50 stocks in an individual portfolio is way too many. The optimum number needs to be decided based on one’s risk appetite. Always be wary of hindsight bias in the type of studies of data back testing. A lot more things could have happened than would have happened.

Did you select Random set of stocks and got to this result? Did you repeat the randomisation for about 5 or 6 different sets and looked at the range of the results?

@butun I did not select stocks randomly.

I took the top 10 stocks based on their weight in the actual portfolio to build my virtual portfolio. Weight of these 10 stocks in the virtual portfolio is proportional to their weight in the actual portfolio. I repeated the process for each week of the past 10 year period to ensure that my virtual portfolio always represented my top 10 positions at any point in time. The logic is that weight of a stock in the portfolio is directly proportional to my conviction in the stock idea. I glanced at that composition of the virtual portfolio as on some key dates during 10 year period and indeed this portfolio mostly represented my high conviction ideas at that point in time.

I also build more virtual portfolios of my top 5, 10, 15, 20 and 25 stocks using the similar methodology and found that as the number of stocks goes up, return and risk goes down but return goes down more than the risk. Exactly as suggested in the research. Even my top 25 portfolio outperformed my actual portfolio.

Similarly, I build another virtual portfolio of my low conviction stocks using the bottom 10 stocks based on their weight in the portfolio. This one under performed the actual portfolio. A quick analysis reveled that these stocks turned out to be low quality stocks so I had low conviction in them but I bought them anyway because they appeared to be cheap (classic value trap).

So conviction and concentration matters. A combination of a high conviction concentrated equity portfolio and short term govt bonds will be a good balanced portfolio. classic Markovitz efficient portfolio.

@basumallick there was no hindsight bias in this analysis as I selected top 10 stocks at a given point in time. On a weekly basis, the virtual portfolio was rebalanced to represent top 10 stocks in that week.

@Yogesh_s Hindsight bias is built into stock weightage as its dependent on the performance of a stock vis-a-vis a portfolio. One stock that does very well will have its weightage increased in a portfolio of stocks. so, in a way you are looking at only those stocks which has performed well. The point I am trying to make is for most fund managers, they do not know which stock will outperform the most.

@basumallick, Hindsight bias exists if you take your current top positions and build a portfolio going back few years using the these stocks. I build the virtual portfolio by using the top positions as they existed during each week of the past 10 years. i.e. my virtual portfolio as on 1/1/2008 represented my top 10 positions in my actual portfolio as on 1/1/2008. Most of my top 10 positions over the years don’t even appear in my current portfolio.

There has been attempts to incorporate the best of both concentrated and diversified portfolio. A model portfolio of this kind would have concentrated nature for 70-90% and rest 10-30% heavily diversified. The concentrated part would contain maybe 5-9 high conviction and predictable companies. The diversified part would contain 5-15 high risk high growth companies. Hitesh ji follows a similar approach as far as I know.

Generally we think that if number of stocks increases then returns of that portfolio started mean diverting to Index Returns. But this need not be necessarily true. Just take a case. If we find some good stocks out of Midcap 150 stocks , fulfilling basic parameters like Return on equity, Debt etc…So if even 50 good stocks are selected, returns can be way better than index returns…There are so many Mutual funds which are giving high returns like SBI Small Cap …where more than 50 stocks are held…This is a fallacy that more number of stocks give average returns like index…It depends on which stocks you have selected and not number of stocks…If u select 50 stocks which all are giving 30% CAGR, then why the portfolio will give 12% CAGR of Index?

I think there is a bias here

Better would be to report based on initial invested capital

What you are doing is adding to stocks that have performed well

I did a 3 months test and an equal allocation on top 30 ideas beat the 10 best stocks I invested into.