The Company is involved in manufacture and sales of Networking equipments like Wireless routers, LAN cables, Switch, Hubs, etc.

Recently they have added innovative products like networked CCTV, Cloud based storage, wifi extender, tablets etc.

The company does seem to have a monopoly in terms of brand name and marketing in the networking domain. In my circle of competence I have observed Dlink being used in LAN/ OFC cables, Switches, Hubs, Wifi Routers etc,

The reasons I find that it is a value buy is as follows.

As more people get smartphones they will need Internet to use. As traditional 3G Internet packs are too costly, Many will turn to unlimited broadband connections on WIfi to use internet. Wifi Routers will penetrate the market just like smartphones have done. And Dlink being a major branded player will reap the benefits.

Good management as it is a part of international Brand. Global presence in 66 countries.

The product (the Wireless Router I bought ) is good with 3 years warranty and they have a huge product portfolio, From Large buisness to travel sized wifi hotspots there is something for everyone. Also They have a wide service network as mentioned in their annual report. I think of this as a moat as other manufacturers do not offer such a wide portfolio of products.

Digital india initiative may cause a huge demand.

if the future plays out nice they will get a good share of the sales.

The negatives:

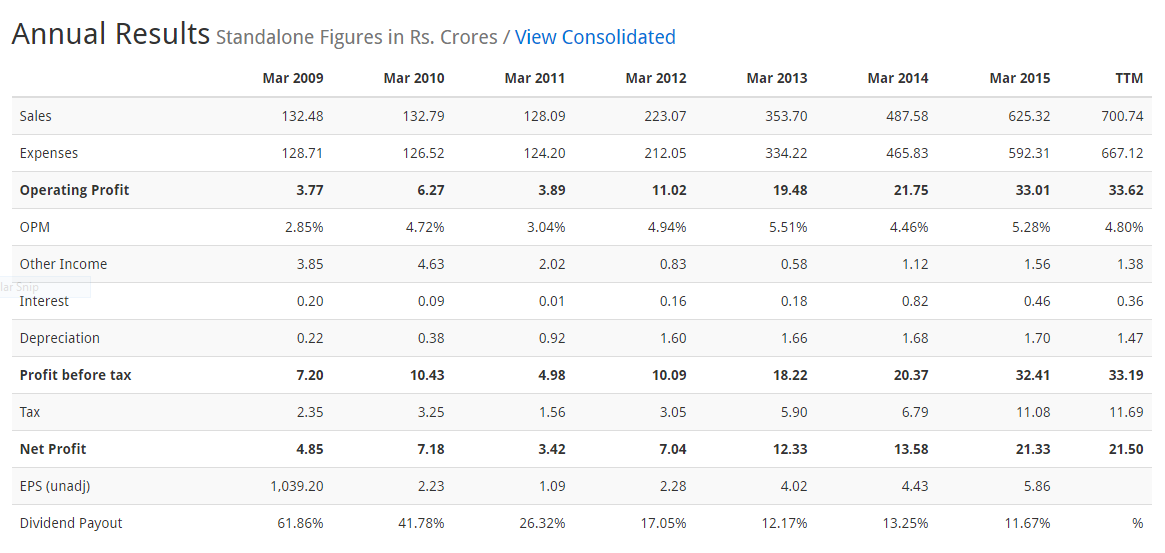

As of last year the company has only 10% growth in sales, Also there is slight decrease in the profit margin. Seems that company doesnt have pricing power as Wireless routers are a common item and people generally prefer cheapest ( also because of online sales ). Also mostly new installations are offered by the Broadband installer who go for the cheapest product.

Chinese products may take market share.

Since it is technology based company it may get overthrown by some other player with a more competitive advantage or feature rich product ( e.g samsung overthrowing Nokia )

I have tried a basic valuation and find that the stock is correctly priced as of now . However the stock story seems good enough and I am planning to hold on for the next few quarters and see if the results improve.

Can anyone else kindly check the company and provide an unbiased opinion about the same.

Thanks for the reply. I like the way you have made a research . Very simple yet effective. I would like to add that I myself have bought the 1st model posted by you coz it was the cheapest among the branded ones and even saw it stocked in physical stores.

Some unique features offered by this particular D link model.

Offers both wireless access point and additional 4 wired points so that you can connect devices which require LAN PORT and not WiFi.

After buying I observed that dlink provides free static DNS to its customers. Its a big plus for geeks and would enable them to have repeat customers.

3 years warranty so no tension in spending the premium compared to Chinese products.

Read the report and was surprised to find the similar thought pattern. Also found that the parent firm from taiwan owns 51% and has recently gone down by 2/3rd of it mcap.

Yes. There is a ICICIdirect report from June 2016 too which highlights the same issues.

However interesting point is that both the reports maintain a “BUY” on DLink.

The Cash Flow statement does not back the Income statement in that the CFO lags the Net Profit by a wide margin. Seems to me most of the profit is accumulating on the balance sheet as Inventory and Account receivables. Not a healthy trend in my humble opinion.

Looking at the screener numbers has been the limit of this research if it can be called that.

in addition to that, also look at the OPM. I consider dlink to be comparable with an electrical appliances company like Havells. (You may disagree but just stating my thoughts). Now Havells has an OPM of 9-10% whereas dlink has an OPM of just 5% or so. This means that despite their reach and brand name dlink has not managed to extract a premium comparable to other appliance cos. At a pe of 20 further pe expansion is possible only when the brand power translates into pricing power ie higher OPM.

Having said all that, I believe Dlink has a huge and growing market to tap into. Wifi penetration in India is so low that every flat and every office is a potential customer. With Google providing free wifi to people at railway stations, more and more people will become aware of wifi and want it. If you believe the upcoming iot hype then the optionality is immense.

I bought Dlink router and stock when the isp technician who came to setup internet at my place insisted on Dlink (no matter where I bought it from) because of his good experience with Dlink. I categorized it as a Peter lynch stock and went for it.

Disc: invested at higher levels with a 3-5yr horizon and will average down if it falls

What about reliance jio ? If reliance jio give you very cheap internet, why people will install wifi modem at home ? As said if jio giving 10 GB in 100 RS, why people will install wifi ? Which is location based internet, rather buying one mobile internet ?

Latest Annual results are out, The revenue growth is very less approx 12%. I have exited the stock. I think this is a classic case of a company that has a great story and a awesome product however the numbers dont seem to be good.

Also from the recent trends market seems to react to the dismal performance,

Hi everyone! The profits for D-Link have grown at a good clip but my concern always was that the profits don’t seem to be supported by cash flows. Cash flows from operations have been consistently well below the net profits (adjusted for depreciation, finance costs and other income) for each year. The trade receivables and inventories just keep piling on! Anyone having a take on that?

Quarterly results have been quite bad. I fail to understand the degrowth in revenue. Seriously reconsidering my position now. Inexplicable why revenues would go down.

Request you to please read technology hardware section in 5 rules of making money in investing by PAT DORSEY of morning star and reconsider your decision to hold.