there is 496cr onetime gain from sale of stake, in the EBITDA

1 Like

Numbers are quite weak. Adjusting for one time other income and minority interest, only 15% YoY PAT growth. 15% growth for a 100+ pe stock is a crime. It should see correction on Monday.

4 Likes

This came on 14th and the market ignored the report…let us see how the results are viewed

3 Likes

Agree on this, the speed of growth is decreasing, and PE is Still Hanging High

@vipraw_srivastava @KS16 Finally, the market realized

3 Likes

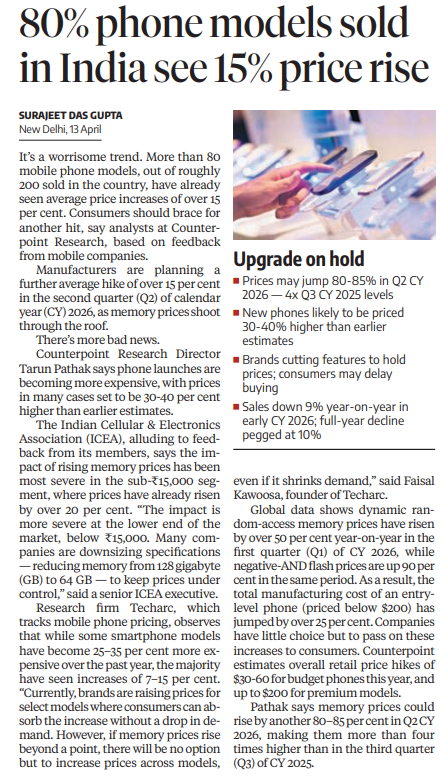

Really interested in this company, especially since the PE has come down to 50 now and want to invest. But with the increase in RAM prices, phones will become much more expensive next year? Isn’t that a huge headwind?

1 Like

@Ankit_Mishra Yes, it is. Wait for clarification post results next month

1 Like

Smartphone retailers forced to pay salaries out of their savings as sales dry up - The Hindu Smartphone retailers forced to pay salaries out of their savings as sales dry up - The Hindu

4 Likes

We’re finally moving past just putting parts together and actually starting to own the whole tech stack.

Green light from the government under the ECMS scheme to start making camera modules. By getting into these high-value components, Dixon might not just be a low-margin assembler now.

It’s definitely an exciting time to watch the industry evolve. As all major EMS have cooled down from high valuations. Dixon itself is trading around 55x P/E (TTM)

4 Likes

Dear fellow boarders,

Please be mindful when relying on Screener data.

- The TTM P/E is not 55 as shown on the website. In fact, it is neither the reported TTM P/E nor a correctly adjusted figure.

- To the management’s credit, they have been voluntarily disclosing adjusted PAT figures in each relevant quarter’s PPT.

- Adjusted for non-recurring one-time benefits, the adjusted TTM P/E comes to 67x. Mostly, these adjustments are for gains from Aditya Infotech’s listing.

- Images for your reference below.

Disclosure

- Not invested. Not recommending anything.

- Not a SEBI registered adviser or research analyst.

- Only sharing for improving our collective understanding.

Snapshot from Screener.in

Snapshot from 2QFY26 PPT

Snapshot from 4QFY25 PPT

Adjusted PAT and TTM P/E working

13 Likes

This also is actually incorrect. TTM PE is around 80x. You have to adjust for minority interest. Management has disclosed it in earnings PPT. Adjusting for that PE is 80x+

4 Likes

Oh yes. I missed that. Thank you for pointing it that out!

If we also (1) remove minority interest, (2) adjust the exceptional items for tax effect and (3) subtract Aditya Infotech stake, then the P/E is ~75x. Which means the P/E at the time of my previous post was >80x!

3 Likes

1 Like

There is also a fierce competitor in the unlisted space by the name of Bhagwati who has increased revenue growth by 128% this quarter when dixon has just managed 3pct growth……interesting thing is that Dixon’s JV partner Longcheer is actually giving this incremental volumes to it’s competitor….seems that mobile assembly has no moat….lowest cost provider wins….dixon must do component manufacturing to add value if it wants to survive here.

3 Likes

Excellent points, I would like to add a few things here. Bhagwati is currently the challenger with a massive growth base, having started from a much lower revenue base.

Secondly, it’s a tough quarter for Dixon for a few reasons beyond just Bhagwati.

Firstly, a global surge in DRAM and SSD prices has squeezed margins for the brands they manufacture for, leading to lower order volumes.

No Brainer why SK Hynix is doing so great lately in the Korean Markets. Secondly After the 2025 festive season, brands are sitting on high inventory, leading to the flat 3% growth.

Yes, Dixon’s management isn’t blind to this. They are pivoting towards backward integration; they are moving into Display Modules, Camera Modules, and Mechanical Enclosures.

3 Likes

Dixon Technologies Uncertain About Mobile PLI Extension After Budget Silence https://share.google/IXMxYhenSj9qfrVdr

2 Likes

Low end phones have gotten a 50% price increase. Purchased a phone for my grandfather in sep/oct for 6.2k, today that same phone at amazon costs 9k, samsung’s lowest offerings are currently at 10.3k. High end phones might hold at the same price cos there the %cost for memory is a lower share and services is a now focus for companies(only for apple, pixel, samsung) but what choice do companies like Vivo and Moto have

2 Likes

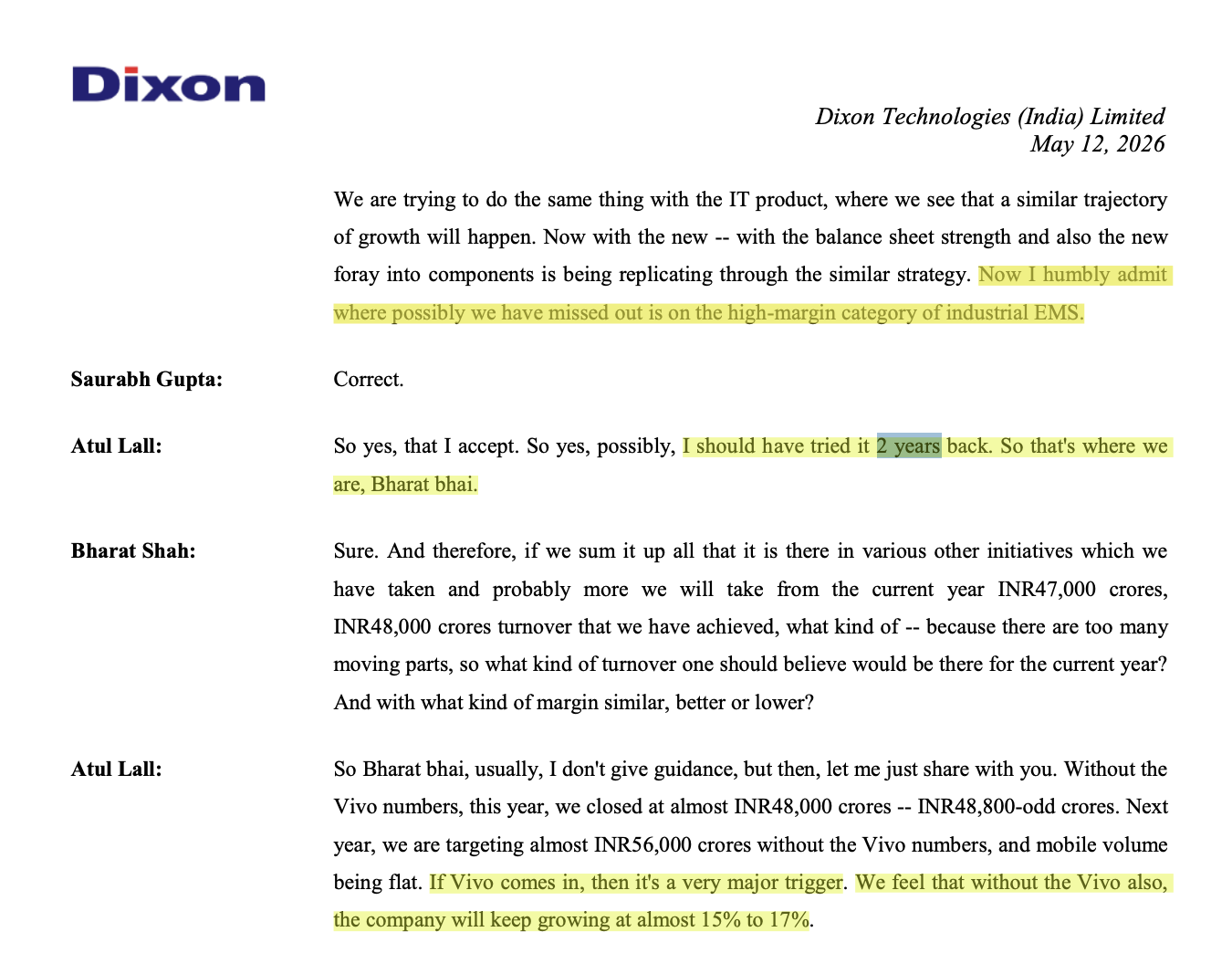

Growth Drivers:

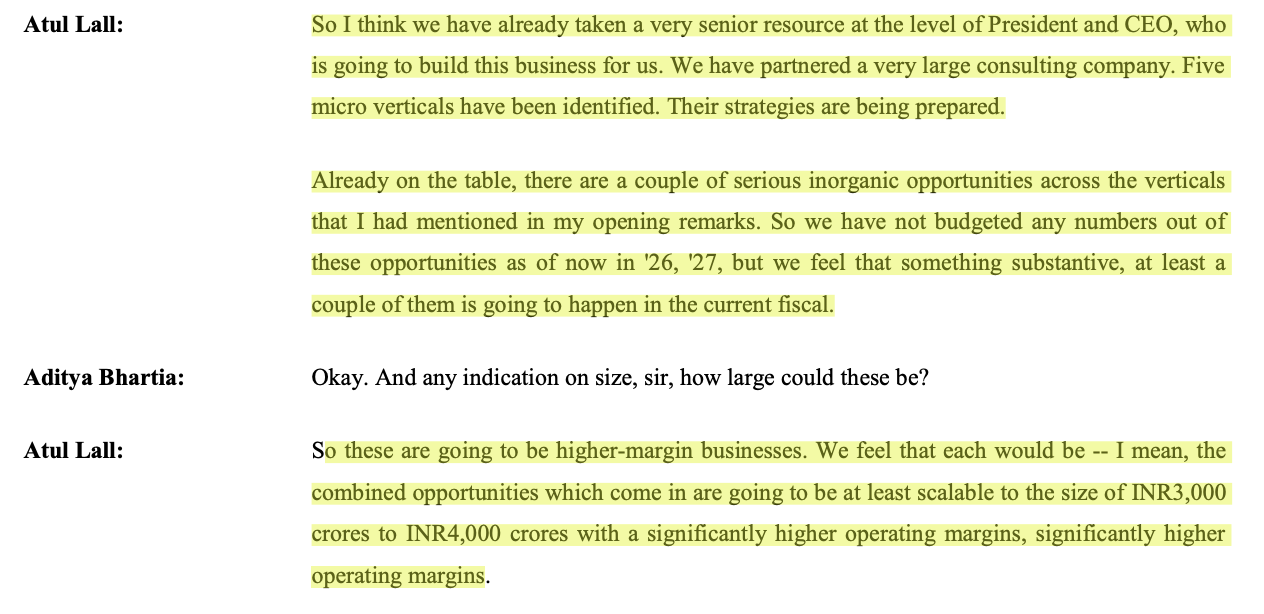

- Management admits their mistake of not venturing into the high-margin industrial EMS business, and they are looking for inorganic opportunities in this business. The company has already hired a very senior resource at the level of President / CEO who is going to build this business for them. They are looking at a 3000 ~ 4000 Cr business with high-teen margins. (This is almost equal to what Syrma and Kaynes does right now.) The valuation of this business alone can be somewhere around 20~30K Crores

- Targeting telecom business around 7500 ~ 8000 Cr which is 50% higher than the last year of 5000 Cr.

- The lighting business, which was laggard last year, would grow 100% to 1700 Cr this year.

- Revenue growth of 15-17% at a consolidated level without the Vivo business, and Vivo business is a major growth trigger, which would contribute almost 20 million smartphones per year, without which it is currently 30 million smartphones. ( so 66% growth if approvals come by)

What I feel is the major re-rating driver would be entering the high-margin EMS business (which is growing at 25~35% for at least the next 5 years, based on the comments of other EMS players). And given the balance sheet strength of Dixon (free cash flow of 700+ cr after capex of 1050 cr for FY 2026), it shouldn’t be difficult for them to grow fast in this business.

4 Likes