I am new to ValuePickr forum, and have learnt a lot by reading good analysis of various businesses done by experienced investors. Though I have been investing since 2004, I have learnt the art and science of value investing after joining some paid forums and also exploring ValuePickr forum post April 2012.

I have managed to generate around 25% CAGR so far, thanks to the positive gains in market post September 2013.

My stock selection strategy is as below:

Look for business with ROE and ROCE close to 20%.

Moderate or High growth (12-30% EPS CAGR) depending on the stock.

Good management quality.

Debt to Equity ratio of less than 1.

Stocks which are reasonably or undervalued compared to industry.

Avoid real estate, power, cement, commodity stocks as far as possible.

Look for minimum 15% CAGR for next 3-4 years in case of Large Caps and higher in case of small caps and midcaps.

Believe in diversified portfolio of about 20 stocks, as much as possible. At times, I have gone till 22 stocks but not more than that.

Being from IT background, comfortable with IT business apart from Auto, BFSI, FMCG, Textile, Chemicals and few others.

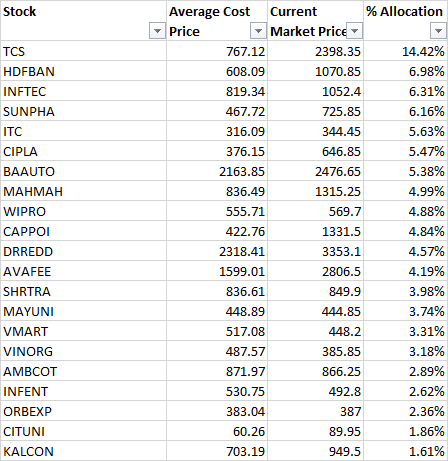

Following is my current portfolio.

I am looking for suggestions about this portfolio.

I would like to continue with strategy of having 60-70% in large caps, and remaining 30-40% in mid caps + small caps, but I am open for some new upcoming businesses which can give me 25% CAGR returns. My horizon is up to 8 years or so considering that most of the goals are in that time period or after that.

I am looking for alternative for Accelya Kale, since upside from here looks limited to me. Also, I am aiming to reduce TCS to 10% of the portfolio since believe in diversification and trying to identify an alternative for it. CYIENT have been identified as one of the alternative and also exploring some product based IT companies.

I am also exploring Deccan Cements, Nitin Spinners, Gulshan Polyols, and Chamanlal Setia as few small cap additions to this portfolio.

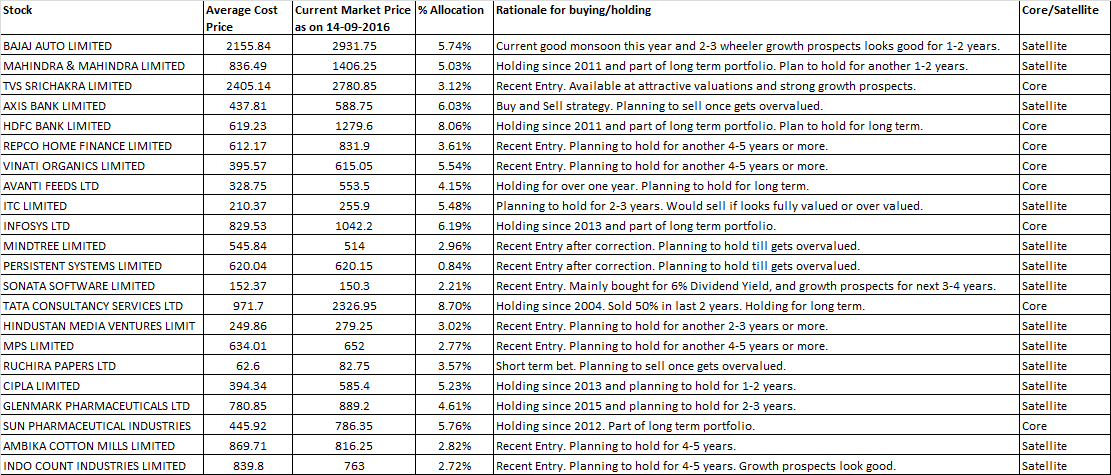

You can consider buying more of bajaj auto on dips. Reason- super duper margins, New avengers are a big hit, KTMs are doing really well. If quadricycle fires, the stock price can reach the sky.

Consider DB CORP on economic and domestic consumption revival.

@gsapte The kind of stocks you have shortlisted and the target you aspire gives me a feeling that it would be better if you buy a mutual fund instead which closely follows the index. SENSEX has historically grown at a CAGR of 17%

I can understand that, ValuePickr forum mainly looks for small caps and mid caps which can generate 20-25-30% CAGR on annual basis. Reason for having large caps in my portfolio is to protect the downside considering that I do not have very long time frame for my financial goals.

Also, I have learnt in the past that, even such a large cap oriented portfolio can give returns of up to 25% CAGR if stocks were bought when undervalued and sold when get overvalued. I have always followed a stringent process for this and it has worked quite well.

Reason for TCS being high in portfolio is due to investments since IPO days, and comfort with the management, vision and ability to grow in tough conditions. Also, I understand that, now onwards it will not give me 20% CAGR returns hence have reduced it from 25% to about 14%, and may reduce it further. TCS is a high ROE/ROCE business with good cash flows and good dividend yield.

Mutual Funds can generate returns close to this, but I do not have control on the portfolio, and they keep holding overvalued stocks for a long time. I have more control on the portfolio and can follow my own style of investing. I do have separate MF portfolio.

I am slowly learning the art of identifying small caps which can give 25% CAGR returns and hence there are some quality small caps in the portfolio now. Due to tendency of not overpaying for some of the quality names I do not have Page, Gruh, Repco, Ajanta in the portfolio.

If you are medium risk taker then you can re-shuffle your portfolio… You can invest 45% in large caps and the remaining 55% in Small and Mid cap stocks… Just make sure that you do a good research and invest in small and mid caps which can yield better returns… You can look at NCL industries a south based cement company which is an small cap… Considering the growth of AP and telengana I’m personally bullish on this one… Also the management has taken several steps in reducing their debts and is in the verge of an turn around! The Company has also posted good set of numbers in the last quarter and expected to post good set of numbers in H2 as well.

Another small cap in which I’m super bullish is Krebs bio chemicals a south based Pharma company… Co., holds 2 USFDA approved plants… IPCA’s take over will be a trigger for this one to be a turn around. You can buy on dips…

You can allocate 10 to 15% on these two. You should have enough patience.

And one more thing 22 seems to be very high number for me… If you are able to track the business of all the stocks then you should not hav a problem, if not, you can reduce it to 10 and can have a very concentrated portfolio.

Disc - NCL, Accumulating since Rs.90… Krebs, Accumulating since Rs.79.

Ajanta no longer looks so expensive on a comparative basis after the recent correction. I have just started adding some more after 7 months waiting for it to correct. I recommend buying some at this level.

Disclosure: Ajanta forms 30% of my portfolio, accumulating since 2 years

Your best stocks have been TCS and Caplin Point, but your allocation to Caplin Point is very low. I assume your allocation to TCS might also have been low but due to price rise the allocation might have gone up.

One problem with diversified portfolio is that it moves in line with the index if the stocks are good. Otherwise it always underperforms.

I believe that you will be able to generate similar returns if you buy NIFTY ETF.

Think on reducing the number of stocks in your portfolio.

I have identified Deccan Cements, as a good 2-3 years growth story from ValuePicker forum, and have built good conviction in the story.

I have bought V-Mart, Vinati Organics at little higher valuations hence there is some loss on these 2 stocks. So I have learnt that, my style of value investing should be strictly followed as much as possible. From that perspective, there are very less buying opportunities even after market corrections.

My process of buying large caps on lower valuations and selling at higher valuations have worked well in the past, but I am tweaking portfolio to cover some mid caps and small caps but need to wait for more opportunities at right valuations.

You should listen to the management interview of Deccan cements. They are not planning for any expansion and they are already running at 60% capacity to which they said that maximum they can go to 75%. So for short term till they reach 75% say within next 8-9 months you should hold and then plan to exit accordingly.

Sorry for the very late reply, couldn’t get time (drenched in chennai rains)… Yes the company did not do very well in the past… But with the recent developments and managements decision to review the company and IPCA’s takeover plan are something which is attracting… If you look at the future then this is an company to be considered for investment… This the only company in India and one of the very few company in the world to manufacture pharma prods through fermentation process… It may take another 2 to 3 qtrs for the company to show some sign of improvements. Also the company own’s two USFDA approved plants and hefty land (which can be considered for expansions in the future as well). I strongly believe things will materialize positively.

Please do your research as well and let us know if you find any mishap… I’m invested in this stock with a long term view.

I have been reading Value Pickr stock discussions and also member of one equity advisory service currently.

Advantage of being member of equity advisory service is that, you can refer to their detail in depth analysis and build your conviction based on financial data and future prospects. Being in full time job, I do not get sufficient time for self study.

Drawback is that, there are lot of recommendations in a year and I tend to buy more stocks than I would like to buy (Say only 6-7 new stocks per year after selling overvalued stocks if any, or even less). I am aiming to reduce portfolio churning to reduce brokerage costs, but not able to do so.

In parallel, I also read free forums and build my own convictions and allocation strategy.

Currently, after recent churning, my portfolio is as below:

My plan was to restrict portfolio to 15 to 20 stocks but I am not able to do it even after long 10 years of direct equity experience.

I request all members to see, if you have any suggestions which can help me reduce this portfolio to about 18-20 stocks.

Note that, I do have separate MF Portfolio for some financial goals.This is my Direct Equity Portfolio with vision to generate 20%-25% CAGR per annum. I have generated about 18-20% CAGR by holding 60%-70% in large caps and remaining 30%-40% small/mid caps in past 4 years, but aiming to improve my allocation based on conviction. I am comfortable with 20%-25% CAGR but would like to have portfolio with less stocks.

@Yatharth : As per my analysis TCS and Infosys can command P/E of 22 + in good conditions, and global scenario. Due to current subdued sentiments in IT area, these two stocks have corrected from their peak and hence can provide 15% CAGR for next 2-3 years. This is off course may or may not happen. This is as per my strategy to hold few good large caps in portfolio for stability and dividend yield. For me Dividend yield in TCS was 4% earlier and now also it is 3%, so I have continued to hold these.

Addition of Persistent and Mindtree has been done to generate slightly higher returns than TCS & Infosys. Due to tie up with IBM, prospects of Persistent look good. Mindtree is long term 25% CAGR story and currently available at P/E of 13.

I have aligned my portfolio to more small cap/mid cap companies than earlier, which are on growth track but were available at decent valuations.

Query to this forum is - I purchased STFC about one and half years back with rationale that, as economy would pick up, its NPA may go down and that may increase its profitability to earlier mean. That does not have happened. I am looking to replace it or focus only on other BFSI stocks which I have namely, HDFC Bank, IDFC Bank, Repco and Edelweiss.

I have checked Q1 2017-18 results of STFC today and there is some positive trends visible, like good 19% PAT growth, AUM growth and stable NPA(s).

I am looking for any views on its merger with IDFC. Is it a positive trigger?

I always look at large complex mergers with negative bias, since chances of such large mergers being successful are low.

Any views on this would help me.

Consider these three points, regarding your portfolio:

Most stocks are small to mid cap

Large Caps are mostly IT and Pharma, both sectors are beaten down due to hawkish stance of the new presidency in the US.

Banks have a huge negative NPA undercurrent, which will be highlighted in a bear market.

Now my worry is, your portfolio is majorly vulnerable in case the market starts to fall, like some wise investors believe will happen soon.

What would be your state of mind in such a correction? What will you do, knowing that your portfolio may lose as much as 50%. That is my worry. Not the kinds of stock you have, they are all good.

Sorry, if I sound gloomy. But, this is the first thing I thought looking at the portfolio.