Came across this article from a search on “Disruption” in my RSS Feed Reader (InnoReader - Recommend as an alternative to Feedly Premium).

http://www.valuewalk.com/2016/08/disruption-the-companies-to-avoid/

The mention of the Credit Suisse report made me immediately search for it in google using the focused search terms shared during the meet.

site:doc.research-and-analytics.csfb.com + pdf

The 54th result (meaning on the 5th page) gave the actual report “The age of disruption”.

https://doc.research-and-analytics.csfb.com/docView?language=ENG&source=ulg&format=PDF&document_id=1058629661&serialid=q9Cfg%2FtflZrtPm2ST0rHMqltrNaTGVxlKYuIEh4DYdQ%3D

Brief Summary:

As a result, we have collected the degree of business risk to each of the major disruptive forces for over c1,500 companies whose combined market capitalisation is similar to c75% of the MSCI AC World index.

Disruption is a fact of life, and it is not always positive for the disruptor and not always negative for the disrupted

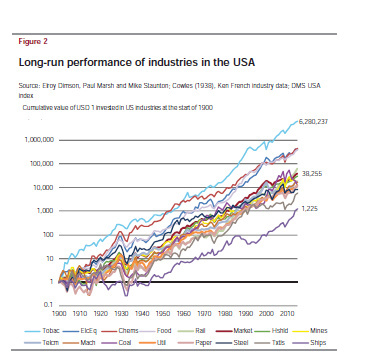

History is full of examples of how new technologies disrupt existing industries and impact equity markets. For example, rail companies made up c50% of the US and UK equity markets in 1900. Today their sector weighting in these equity markets is minimal.

Future disruption likely dominated by three factors

■ First, we highlight the impact of globalisation. With China as the obvious mediumterm

threat and likely joined by India in the long term, we see continued pressure on

margins and reduced pricing power across a multitude of industries.

■ Second, we highlight technology. Technological innovation introduces new products

and services at a cheaper cost, which makes incumbents obsolete. Areas we see at

risk include both consumer end-markets as well as multiple industries (see Figure 34

for details) and the wider workforce as increased automation puts more jobs at risk.

■ Last, we highlight tightening regulation or government policies as key disruptive

forces. Stricter financial regulation, tighter environmental standards, rising minimum

wage policies and a greater focus on health-related policies all impact many

industries.

Who’s at risk and who’s not?

We refer to data from page 23 for an overview of the most and least exposed sectors and

companies, globally and by region. Figure 2 summarises the trends on a sector level. The

most and least exposed sectors are as follows:

■ Sectors that look most at risk from disruption include Energy, Autos,

Pharmaceuticals, Semiconductors, and Health Care Equipment.

■ Sectors that appear to be most insulated include Household & Personal Goods,

Transport, Telecoms, and Food, Beverage & Tobacco.