In the concall; they had mentioned that net debt levels would start to come down as early as this coming quarter. They had also raised NCDs recenty; but quarter on quarter net debt reduced from 173 CHF to 168 CHF.

1 Like

can you pl share link for concall recording

Note: My bad, they have a 2~3 year perspective to bring the net debt level down to 120m from current 168m.

is there any information on their capacities across countries and info on unit wise utilization, sales and margins.

they have 25 manufacturing units which is very high for a company with 2,500 Cr of sales !!

1 Like

anybody has any research / info on Dishman. Seems to be turning around.. but not sure.

Have been holding them for quite some time. The issues regarding approvals seem to be behind them now. Capacity building capex is also mostly done. Only maintenance costs to be incurred for the near future. That should help to reduce their debt. Guidance is around 10-15% growth, so nothing too extraordinary but should atleast start showing profitability.

One concern in my opinion should be the weakening of dollar and strengthening for the Swiss franc (mainly this April onwards).

2 Likes

My couple of cents -

They are on the cusp of improving the performance. I am anticipating FY26 revenue to be about 3,000 Cr. and with 20% EBITA, their current valuation is at 5.5 times EBITA. I feel the research driven business has good probability of re-rating.

Just in terms of human capital - they have 550 Scientist whereas Laurus has 1,100 which is double. However Laurus’s market cap is 10 times that of Dishman. I understand it not a comprehensive comparison but confined to only one parameter. But definitely sufficient to believe that with capabilities (Human and Plants and Approvals) Dishman has potential for a decent market cap growth in coming years.

Disc - Invested

4 Likes

Have done some research and my findings: Stock price has underperformed for 10 years.. thats a considerable period given company is into CDMO business.. all other peers have done much much better. there are some fundamental issues with the company why this is happening - given below:

1.Company’s revenue from India is only Rs 400 cr (10% of total revenue) and reducing - Q1 FY 2026 India sales are down whopping 40% !! Plants in India have been approved by foreign regulators a year back and India business has not revived

-

about 80% revenue is from Europe where cost of operations are high and very low margins. All CDMO companies are opposite - have main operations in India and small companies abroad - given this Dishman will never be able to generate profits.

-

Since no profits, company has taken huge debt of Rs 2,300 cr to run operations. Since they are not able to repay from operations, they plan to raise equity (as they have taken enabling approvals in last board meeting). So losses are going to be funded by equity - that is if anybody is foolish enough to invest.. Existing investors are anyway trapped. Indian investors funding loss making subsidiaries abroad which will never make money.

-

Investor call of May 2023 summarizes all the problems with the company -

Please refer to the question raised by Mr. Satish Bhatt.

Satish Bhatt: I just wanted to know what is the risk we are anticipating for that 12% to 15% top line and 20% EBITDA growth. Because I have been seeing this company for maybe the last 10, 15 years. And I think every 2 to 3 years, we start having some problems. So, we are back to where we are maybe 3 years back. So, what makes you confident that the next phase of growth will be there and we will have sustainable growth? So, what type of risk can come? We had EDQM risk, it has taken more than 2 years. Some of the products are taking more than 2, 3 years. So, what is the risk you are inbuilding in your modeling. So, where are we going wrong every 3 to 4 years. I think that’s quite a long time and most of the business cycles take place in 3 to 4, maybe 7 years. We are where we were I think 5 to 6 years back.

So, one incident comes, suddenly we are back to where we are in 2019 or maybe something

comes in '22, we are back in 2015, '16 levels. So, what makes the management confident of

delivering the things in terms of the manufacturing things have been done, the marketing has

been done, the R&D has been done, sometimes the erroneous contracts come. So, it is a way I

think we build our contracts. So, something is wrong at the, maybe, say at the company level,

which is always preventing us to grow from some level. Does the Board discuss this any time?

3 Likes

Latest investor presentation - still not clear on what they do.. with all capabilities financial performance is not good. it seems to be a business model issue - majority operations in high cost Europe - while all other Indian CDMO companies have majority operations in India.

Looks like the turnaround continues in the right direction - firing on most fronts

Im not a “technical analysis” person but recently the stock also seems to be rerating upwards, for what its worth.

Q1 excerpts and summary below -

Overall Financial Performance (Q1 FY26)

• Strong Revenue Growth: The company reported a consolidated revenue of Rs. 708 crores , representing a significant 35% growth compared to Rs. 523 crores in Q1 of the previous year.

• Improved Profitability: EBITDA for the quarter stood at Rs. 140.68 crores , a substantial increase from Rs. 28.97 crores in the same quarter last year. The EBITDA margin improved dramatically to 19.9% .

• Return to Profit: The company posted a Profit After Tax (PAT) of Rs. 23.4 crores for the quarter, a significant turnaround from the previous year’s performance.

• Debt Reduction: The company is focused on deleveraging. Net debt (excluding lease liabilities) saw a decline from 157.6 million Swiss francs on March 31, 2025, to 149.7 million Swiss francs as of June 30, 2025. The reduction of nearly 8 million Swiss francs in the first quarter alone is well on track to meet or exceed the full-year debt reduction target of 10 million Swiss francs.

Segment-Wise Performance & Business Updates

The company has reclassified its reporting into two main segments: CDMO and Marketable Molecules.

1. CDMO (Contract Development and Manufacturing Organization):

• Performance: This segment, which includes operations in Switzerland, Manchester, Shanghai, France, and the India CDMO business, generated revenue of Rs. 611 crores , an increase of 45% year-over-year. The EBITDA margin for this segment was 17.9% , a significant improvement from 5.8% in the prior year’s first quarter.

• Regulatory Success in India: The Indian sites have achieved significant regulatory milestones, strengthening compliance. The Naroda site was inspected by the USFDA in June 2025 and received no observations (no 483 Form) . This follows previous successful approvals from EDQM, PMDA, and USFDA at the Bavla site, indicating a robust compliance status across Indian facilities.

• France Facility Update: The French facility (drug product) recorded revenue of €4.5 million but had an EBITDA loss of approximately €2 million for the quarter. However, it has received crucial GMP certifications, leading to an increase in project awards and proposal requests, indicating that the business is picking up.

• China Operations: The Shanghai facility received its GMP certification , which is a “door opener” for the domestic Chinese market. The company is now increasing its sales force to attract more Chinese customers and tap into this new revenue stream. Currently, the China facility acts as an “extended workbench” for the Swiss entity, producing intermediates that are shipped to Switzerland for final API manufacturing.

2. Marketable Molecules:

• Performance: This segment, comprising vitamin D analogues, cholesterol, and quats, reported revenue of Rs. 96.8 crores .

• Strategic Margin Improvement: While revenue saw a slight dip, the segment’s EBITDA margin surged to 32.4% from just 4.5% in Q1 of last year. This was a result of a conscious decision to reduce sales of lower-margin cholesterol SF (used in animal feed) and focus on more profitable vitamin D analogues. The company is also actively working to bring down the cost of its key raw material, wool grease, which is expected to have a positive impact on the Dutch entity’s financials.

• Soft-Gel Business: The company has started commercializing its own soft-gel drug products (vitamins and analogs) under the Dishman Carbogen brand name in various Asian Pacific and South American countries. This marks the beginning of a new journey into producing high-quality drug products.

Outlook and Strategy

• Positive Full-Year Outlook: Based on the strong Q1 performance, management is on track to achieve its full-year guidance for FY26. The overall business outlook for the next three to five years is positive.

• Market Focus: The company’s primary markets remain the U.S., Europe, and Japan, which are home to innovator and biotech companies. The share of business from Japan is expected to increase.

• Tariffs: Management stated that potential tariffs are not currently impacting the business, as pharmaceutical products are excluded. Furthermore, the company has limited direct commercial exports to the U.S.; most products are shipped to European formulation sites, even for U.S. customers.

Disc - invested from lower levels

4 Likes

India is doing very badly. even in Q1 sales were down - this is after a year of getting regulatory approvals. if low cost India operations dont improve how will the company turnaround…

foreign operations are already at peak and making marginal returns - no scope of improvement there.

overall profits are going to be low.. while stock has run up of late.. it keeps correcting sharply..

As pointed out in investor call also company has new problems every year and not able to come out of the problems.. it is clearly a leadership issue.. best to avoid such companies.

Q2 numbers were not as bad as its been made out to be (from the price reaction).

In fact they seem to be on course for the full year projected guidance of about 3000 cr topline and 18-20 margin, which is a good run rate for the ongoing “turnaround”

Next year should be even better with all facilities coming into profitability and margins increasing further with debt also reducing.

2 Likes

Standalone India numbers are very bad.. sales much lower and losses in Q2.

it seems company is not able to turnaround..

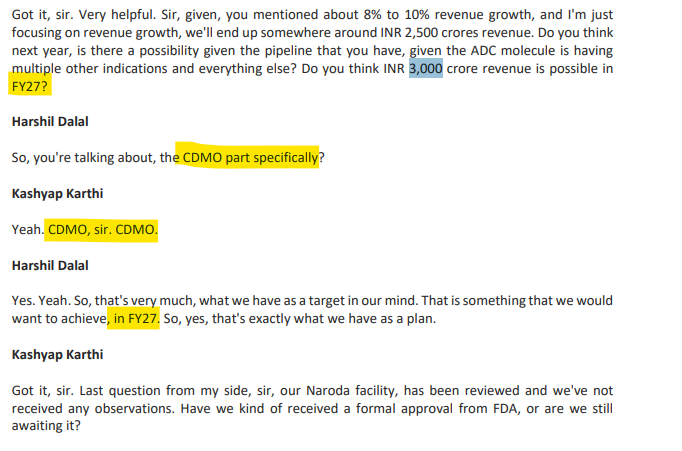

3,000 Cr topline is something I guess management have guided for FY27.

Below conversation can be perceived 3,000 Cr only from CDMO in FY27. However, even if it is total revenue with 20% EBITA and market cap for the company at 3,400 cr. provides a decent re-rating opportunity

2 Likes

Yes , the CDMO targets were being talked for next year - However for this financial year they seem slated and on track for 3000 Cr overall top line with good margins which in itself should be a signalling of continuous Q on Q and year in year improvement probably commanding better valuations.

Next year they expect more ramp up of india operations increasing top line and margins. But thats reading (hoping) much into the future.

1 Like

With 3000cr topline at 20% plus margins expected EBIDTA is 600cr which will be the highest ever for the company. With the planned equity raise and debt repayment, PAT is also going to increase substantially - highest ever.

And with sales and margins expected to increase further going forward, it seems to be a good bet now.. if everything goes as planned shar price could go up 2x of even 3x from here.

Valuation of peers is quite high.

Very poor results.. large decline in EBIDTA leading to losses. Standalone India sales has gone down by 60%. It seems India business is not possible to revive.. lowest every sales.

something fundamentally wrong with company that way underperforming for 10 years.

CDMO companies some time test patience. They have 20 molecules in late Phase-3 trial with majority being for Oncology. Will share the conf call notes on this as soon as I get to listen the recording.

1 Like

Notes from Q3 Conference call

- One molecule rolled out during Q3’FY26. Its for Lukemia with significant commercial size. To be supplied to the customer from Swiss site.

- Potential of Rs. 250 Cr revenue from Balva site for FY26

- ~1200 Cr. RFP submitted. Winning expected for 30-35% value expected to be supplied from India site

- in next 12-18 months, target to have 500 Cr. revenue by end of FY27. In FY28 further ramp up.

- For the breast cancer molecule, CHF 20 Mn. supplied last year, CHF 30 Mn for FY2026, And CHF 40 Mn for FY2027 - Japanese Co-Investment Customer. Indication for first line treatment approval received.

- Phase 3 drugs for especially ADC, in 12-18 months more molecules get commercialized

- On France subsidiary, should be breaking even in FY27. 7 Mn euro revenue from that site in 9 months of current FY. There is huge interest from the customers in France site.

- The co investment for supplying payload and linker to the Japanese customer. Strong demand is expected in next years.

- Capacity utilization 75%-Swiss, 20%-France, 60%-Netherland, 20-25%-India, No capacity constraints.

- Main reason for gross block increase but revenue not increasing by that rate - 1. Foreign exchange 2. India side observation 3. France site just getting ready last year; Over next two years ~ 25% margins

- Utilization from India and France should improve in next 2-3 years. Shanghai facility to improve from 50% to 75%

- Guidance of 20% EBITA target still stands. likely to do 19.5 - 20% for FY26.

- Compared to Neuland and Laurus investments have not yet paid off, reason given that India site is not performing for past few years. With regulatory hurdles are behind India site, and also site is upgraded to handling long term complex orders. For Swiss site, ADC and small molecules are targeted but high volume business had to be let go.

- ADC drug product being block bluster molecule, but the value Dishman get is very small. - 1.5% linker and payload roughly for ADC molecule. With partnership with antibody manufacturer Cellonic, the end to end ADC solution can be offered. Benefitting already from partnership

- Large portion of debt is in CHF, Priority to pare down India debt due to higher rates. Free cash flow to be used to pare down India debt - 750 Cr debt in India, should be completely paid of in 3 years from operations cash flow from India operations.

4 Likes

Thanks for the detailed con call points.

I think the topline and EBITDA is going to be fine and shaping well for growth - the line items below that and hence profits are unpredictable !

Asset utilisation , Goodwill and debt are drags.

Next one / two years should be a full turnaround , as all the ingredients are in place , else management quality is in question.

1 Like