Tata Elxsi is a good company and as you mentioned, it might not fit the SMAC label. They have carved out a niche in design of Electronic products among other things.

As far as I know the only listed company that fits this bill is RAMCO - they have a cloud based product that can compete with the big MNCs. IT Services companies will jump on the bandwagon, but that is understandable as they try to compete for SMAC projects and build practices and COEs. But I am not really sure, if I would term these as SMAC companies.

Would love to know what other listed companies are out there.

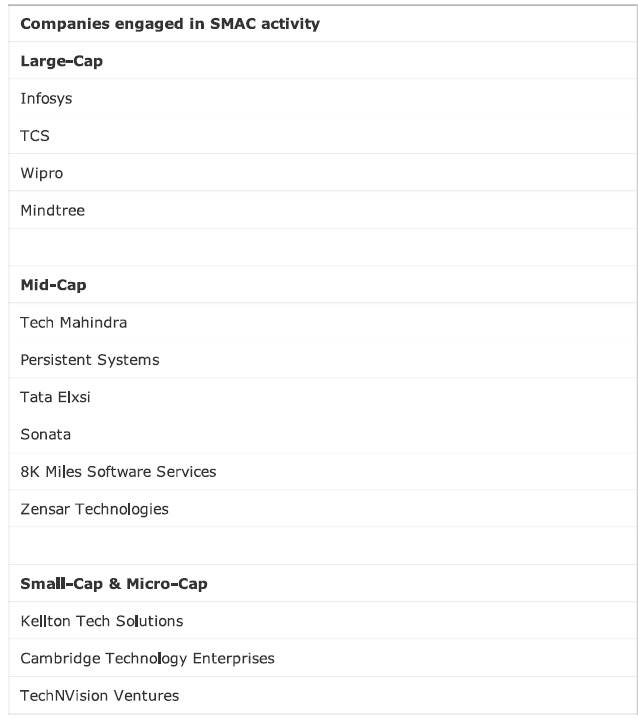

kelton tech and 8k miles are the leaders and rapidly growing

while 8 k miles have established track record … kelton tech is on acquisition spree

and is growing more than 100% annually

there could be leaders in this segment as the BIG IT company will not ab able to grow much

in this segment due to divergent focus .

one of the examples is IMOBI they very swiftly grew in the mobile advertisement sector even before other BIG IT companies could find a clue .

Latest valuation of IMOBI is 2.5 billion dollars .

similarly we will have leaders in SMAC sector and IOT (internet of things) which will reach multi

billion dollar in valuation.

@vijay18 thanks for giving the IMOBI example. That is the kind of IP creator, I have in mind, when I think of a SMAC company. Are there any such companies listed on our markets?

Both 8K Miles & Kelton Tech are IT services companies. 8K Miles is an IT Services company with focus on SMAC - especially on the C - Cloud. But it still is a consulting/services company at the end.

SMAC is certainly a disruptive set of technologies which is real and is gaining more and more visibility and momentum. Undoubtedly it is going to be big, and our lives are already revolving around it. IOT will probably still take time and I dont see any major impact of it till 2020. The objective is to find companies which have sustainable competitive advantage over a whole set of large, medium and small companies getting into this space. Most of these companies are acquiring companies as if there is no tomorrow, it needs to see if these acquisitions are bringing something to the table or will just be a drag.

Companies like 8K miles and Kellton, seem more as pure plays in the ISMAC space. Kellton in particular going by its past couple of years of spectacular growth and comparatively lower valuation seems very interesting. However I cant seem to dig much information about the management. Any further information about the management and digging about the company would be helpful.

Since these technologies are touted to be the harbinger of the 4th Industrial revolution, I thought I might share this rather compelling conversation at Davos.

This is sure shot recipe for disaster/manipulation

Highlight a sector as hot based on some one’s casual remark >> Push shady mid-small cap stocks (which may have/may not have any connection) to gullible investors

I agree that there is lot of noise but there are some genuine stories as well. Cambridge, Kellton and 8k miles are services play but I doubt they will be sustainable value creators over the very long term. There are many ways to skin the cat and I think playing it through product companies is a safer idea.

Insurance vertical : Majesco

Healthcare vertical: Take Solutions (not quite a cloud player)

Horizontals: Ramco (still doing my work)

Pure Services: Cambridge, Kellton, 8K, Sonata etc

I would love to play it through deep domain experts in stable industries along with high growth services players. I was pleasantly surprised to see BM endorsing this strategy in his recent interview.

Disc: Bought Majesco and Take in the recent corrections and continue to hold Cambridge and Kellton. Cambridge is a hope and faith play while I am still not fully convinced with Kellton’s model. without full history these pure plays will remain punts for some more time.

Though i dont have nuch knowledge on investing…i searched for SMAC and found that there is no listed company working purely on SMAC. Since , SMAC is very wide concept… There is IBM,General Electric, Intel working on SMAC since long. Few of Indian companies had tied up with them recently for SMAC.

Hcl tech and IBM

Infosys and GE

Tech mahindra and Bosch innovations

In the mid cap space …persistent is on buying spree and they have acquired companies working on SMAC. Its only company that has started looking at the potential of SMAC .

kellton tech and lycos internet are also leaders in internet of things.

I agree with you that the gap is quite wide. One of the reasons could be type of projects that the company is working on and the margins. e.g. Kellton is currently working on a project for UP government (Project cost around 28 crores). The company developed and deployed mSehat, an initiative by SIFPSA (State Innovations in Family Planning Services Agency) to minimize mortality rate of mother and the child in Uttar Pradesh. In that project, they have some hardware component also which has almost no margin. Management explained this after last quarter result.

I will not call Lycos Internet anything close to SMAC. Their products look like rip-off’s and for a SMAC company, they social media pages are not anywhere closer.

Research: I contacted Kellton posing like a client. They said they will come back to me with a list of their products and services.

8K miles looks like a placement agency with them collecting money for training to send people to the USA. Please refer 8K miles thread.

The management of 8K miles has a good track record and understanding of the technology but I read here on VP that the rest of the management is not trustworthy.

Working in a sister industry, I just cannot fathom the valuations though

The current management of Kellton & Cambridge have bought over existing companies and reworked / reshaped their business model or domain. Hence, the legacy numbers are still in the calculations. You will need to wait for 1-2 quarters to get true picture, when the company has completed atleast 4 quarters under new ownership. This is also the reason that growth rates are nearly 100% YoY. A good measure will be after 2 quarters to see how the growth pans out.

SMAC is just a buzz word. Truly no company is currently working in all four. However biggis are investing to take advantage of the euphoria.

I have been tracking Mold Tek Technologies for last 2 quarters and found an interesting play. They are into M and C other than regular support business.

What I like about this company is their competency into Salesforce. They should be among top 10 salesforce providers from India. Salesforce is on top of the list for CRM market and have been offering cloud solution since long. Considering size of Moldtek, it’s on sweet spot for take over by any biggis who is looking to expand their foot print into salesforce consulting.

I like Moldtek for it’s competency which they have built over the period. Also having clean balancesheet and fair management.

Disclosure : Invested a little. This is not a recommendation.

IMHO there are broadly two broad models. One where they have a large (or fast growing) services horizontal that caters to these services. At this stage for most Indian providers it is “migrating” to digital and just an extension. Our Indian companies benefit because they have incumbent relationships with large customers globally that the specialist US companies do not. The other model is companies that are creating distributed product solutions that work well with the new platforms and interfaces usually in specialized verticals that leverage off SMAC environments. For companies with the first model, one should see more from a traditional point of view (proven size, employees, growth, margins, little capital employed except training). Examples Infosys, TCS, Mindtree. For the second model one should look at size of addressable opportunity, quality of clients, license and AMC revenues, certification credentials, team credibility, time to positive earnings. Relatively earlsy stage but provide a non linear growth opportunity. Examples include Intellect, Majesco, Take, Ramco.