A Hospitals revenue is limited to real estate. And that we know is a huge problem.

The company is way too small, <300 mcap, yet it’s sales growth is slow. Therefore, I wouldn’t pay 35PE as the price would include all the near term gooodness. I would like to wait to see when a new building in a different geographic location is being commissioned.

When scalability is not clear, I would not want to pay such a high PE.

OPM is less than 20

RoE less than 25

Debt 0.5

For such numbers I would get a mid or even a large cap. Pls provide clarity Dinesh Bhai.

I don’t understand what you mean. Please do elaborate. If you’re hinting at the difference between operating a greenfield hospital Vs brownfield ones, then yes, that’s a valid risk. But that’s why I’ve mentioned I’m okay with them not opening a new one in Chennai. The opportunities in Coimbatore itself is bound to increase and there are a host of problems with operating a brownfield hospital.

First, KMCH’s TTM P/E is not 35, it’s ~12-13. Not sure where you got the 35 figure from.

Second, growth and margins are a part of value. They’re not independent of value. A company with very high growth is likely to quote a high P/E, a company with a high RoE is likely to quote a high P/B and so on. But the way these Ratios interact with value remains the same.

Yes, and the financial position is likely to remain weak for a few quarters from now, as they are in expansion mode. It remains to be seen how they will handle the new expansion (Medical College). That’s why my allocation is on the lower side. Don’t get me wrong, I might still buy more of KMCH when price and my own liquidity permits, but it will still remain under 5-7% allocation until all this transition phase is over.

I saw a recent post by you where you mentioned that you added to your position in DHFL. If I remember correctly it was quite high in your 5-6 stock portfolio at the beginning of the thread.

One thing that really scares me is the kind of price chart DHFL has had in last couple of months. Speaking frankly, my reaction would have been exactly opposite to yours. I would have sold off my position promptly and seeing you raising your stakes speaks volumes about your conviction in the company.

So I would like to know the views of someone whose views seem to be exactly the opposite of mine atleast in the case of DHFL. Doesnt this kind of fall shake your confidence in your investment thesis? Do you ever feel that there could be something that doesnt yet meet the eye with the kind of market reaction the stock price has seen? I lack the courage to catch falling knives so would like to know the logic of someone who does it with elan.

Yes, right before the fall, DHFL was probably around 10-12% of my portfolio. At the time of my initial purchase, I wanted to do a basket approach for buying HFCs. But DHFL was the only undervalued company in my eyes. Now, I’m willing to admit that I was mistaken. I valued it then at Rs. 580-600 and purchased it around Rs. 500. In hindsight and an honest admission of the wrong valuation on my part, I wrote it down by 30%+ to Rs. 400-430. Even after the fall, I thought about the basket approach once again. But being a “Value” person, I can’t help but see just how cheap DHFL is in relation to is value.

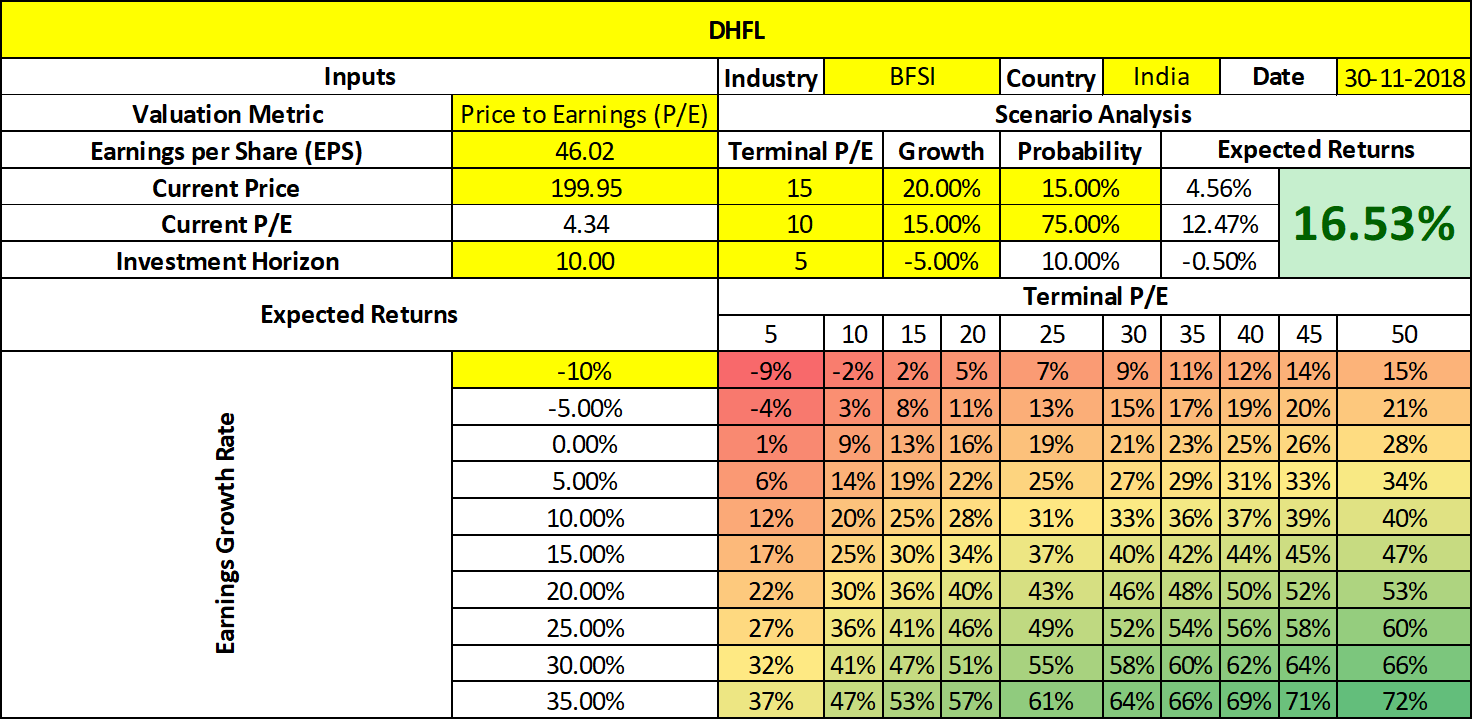

Here’s a small snapshot of how I feel about the investment:

This is just the standalone numbers, so if I add the subsidiaries, my expected returns would probably be around 18%, in spite of the poor to mediocre growth rates and exit multiples I have assumed for the investment.

Absolutely. Skeletons in the closet is the most prominent value destroyer in the Indian markets. That much I agree. But I’d much rather see it pop up somewhere, rather than go with rumors, exaggerated news and panic. As far as TA is concerned, I’m a dud. I never understood how it worked, with the exception of basic support and resistance levels.

At the very core, my reason for investing in a HFC is of course, India’s need for credit. Even if the current creditors in India doubled in size, there would still be room left for more. DHFL, being one of the biggest in the HFC space, is sure to find its spot somewhere.

Hi Hitesh…looking at the latest quarter for DHFL, the numbers look quite good. Don’t you think that a business that is capable of generating these kind of numbers under normal circumstances is trading ridiculously cheap due to the ongoing panic. I feel a lot of perception around DHFL has been shaped due to the recent price action instead of the long term potential of the underlying business. Of course if the price action is hinting at any serious underlying problems then its a different matter altogether. But we are yet to hear anything on that and as Dinesh said it has mostly been rumors. My opinion is it all depends on how soon situation returns to normal as i feel things will not remain like this forever.

Basically, in your scenario analysis you have assigned 0% probability to there being skeletons in the closet, and that is why you are getting a higher value than market price. Is that right?

The stock market price behaviour is itself a rich source of information. Market reflects the collective expectations of different individuals, many of them being much smarter than us, while many have access to better information. is it wise to ignore the probabilities that market is assigning to different outcomes?

There’s a saying in Statistical Analysis: “Garbage in, garbage out.”

If I truly believed that DHFL’s management could be doing more than they’re letting on, then I shouldn’t be invested in the stock at all. The numbers become immaterial, because the driving force behind the numbers (The management) itself is wrong.

Obviously I don’t think that. What I was trying to say is that, I’d much rather see some kind of proof to this end, rather than assuming that it’s most probably the case purely based on the share price action.

Problem is, by the time public will have the proof, there will be no buyers left. It would be much safer to fold your position, partly if not fully, and wait on the sidelines. You may sacrifice part of the gains, if the stock recovers, but your first aim should be capital preservation. You must survive to make the next bet.

Anyways, to hold your position and even add more to it, shows a lot of conviction. I hope it works for you.

So, is the solution selling a part of the shares whenever a company you hold drops 30%+? Even the much-loved Page Industries has dropped more than 30%+ three or more times in the past.

The NFBC scare and the liquidity crisis that followed were very scary indeed. I believe this has distorted the way investors think about the Risk-Reward in this space. I also believe that the scare is short lived. It will impact the space for two or three quarters or at the most a year, then it should be back to normal.

At least, that’s what I think is likely to happen. If it doesn’t and DHFL continues to post mediocre numbers, the CMP still offers a chance at a decent return profile (13-15%). It’s all about taking smaller risks, for a chance at an outsized reward.

Companies like Page are exceptions, not the norm, that is why they are so popular with investors. (Doesn’t mean it will always stay an exception)

And you must see their fall in context, if the whole market fell at that time, then those dips are worth buying. (It represents a fear of macros, not doubt on the fundamentals of underlying business)

On the other hand, look at companies like Kitex. I purchased its share for 300, only to sell it for 220, now it’s half of my exit price. Since then I have taken the study of technicals seriously, and now I avoid stocks in downtrend.

That said, for some people, who are putting in enough effort, buying stocks in downtrend may also work out profitably. Just that, I don’t belong in that category.

Dhfl and yes bank have committed the same sins, from what I understand. There are several other people who have tried to deal from the back doors, their names will come to the forefront too.

Precisely. This fall wasn’t standalone. It was perpetrated by the ILFS default and spread by credit yields tightening. The entire NBFC listed space crashed. I agree that if a stock fell 50%+ on its own without rhyme or reason, I will be tempted to look for clues of mismanagement as well.

I second your thought. Infact I wrote the same in rich dreamz portfolio today.

Now coming to price fall… Lets take 30% kind off. If the index is correcting in tandem, it often becomes an averaging down opportunity. But if stock falls severely… I mean ROC is much faster than market, or falls uncorrelated to the market then its better to completely exit. I have huge respect for cash even if it yields 0 interest. Cash gives you flexibility and chance to place alternate bets. I think 30% fall should be reviewed critically and without any bias. Also by the time 30 % kind of fall happens atleast 70 % of the story behind the stock gets clear. With sufficient information, one should analyse whether this stock will rise up V shaped from here or fall further by 60 % . All this is more important for concentrated portfolio.

Someone with 20-30 stocks may not look at individual stock crash so critically. Just my 2 cents.

With due respect, nobody can analyze how a stock’s price will move (Unless you are indicating a TA, which as I’ve already admitted, is outside my gamut).

DHFL has reacted very well to the crisis and performed the necessary steps to avoid severe backlashes. In the latest con-call, Mr. Wadhwan indicated that the company needs a change in its business model towards a more RoE-additive business, rather than a growth machine.

Even assuming this doesn’t work out exactly as planned, and DHFL is only able to grow its profits by just 15% in the next decade, as opposed to the 30% in the last one, I think it still offers value. If the CMP were closer to Rs. 400, I wouldn’t be as enthusiastic to purchase it.

My thought process was that, while yields have pushed up costs for all players, yields for DHFL “type” companies have gone up even more. If there was ever such thing as a competitive “disadvantage” this looks like it. Very very (a few more very’s) few companies do well in a cost escalating environment (last quarter even Asian Paints had muted numbers). DHFL, I thought, is far from being the greatest. My assumption was that with yields on liability side going up significantly, it would be hard for DHFL to grow at 15%, unless they start to push up leverage even more (they are already at 10-11 and dont know how much more room they have to increase levering) as I just dont believe they can maintain their ROE at 15-17%. This is the reason I have been tracking but did not buy as yet.

It would be interesting to see what had happened in 2013, the last time they were so cheap in 2013. How they dealt with it and came out strong. If they are able to repeat that feat somehow, this might be a multibagger.

I dont have technical knowledge. the price seems to move in the channel drawn (as shown in the chart). Interesting thing is that a few other HFCs like lichf, gichf also seem to be moving in similar channels.