I would update the first post and mention it in a comment once I make a new purchase or modify existing stocks.

Regarding Screens, I would rather not point to a specific set of Ratios or a Screen itself, as it would be a really biased opinion. I will give you the general framework of how I go about filtering stocks.

-

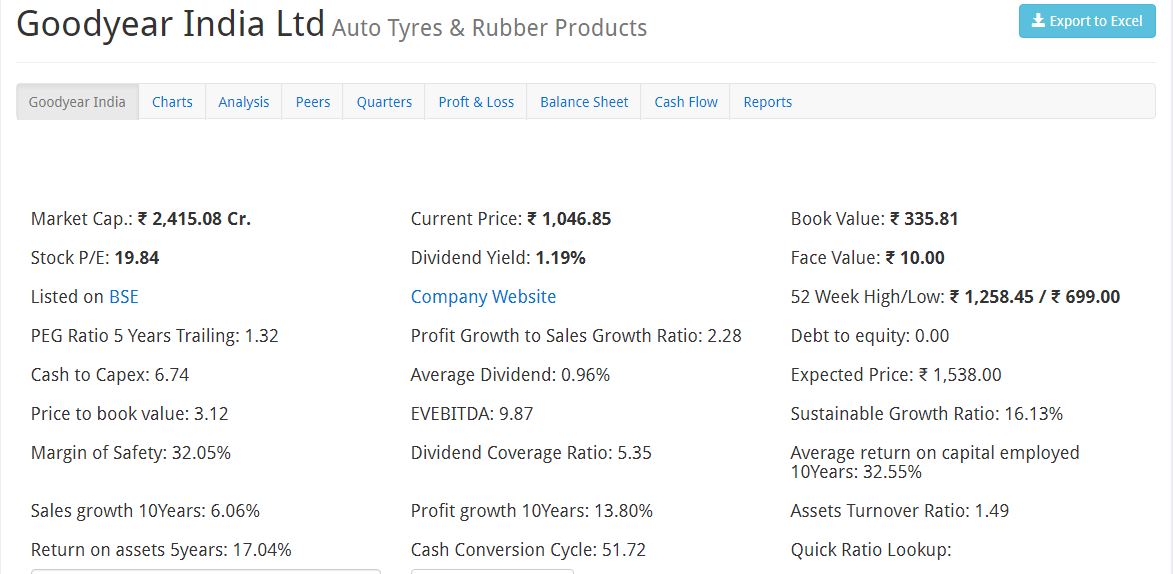

Identifying Pricing Power: Pricing Power is often the first frontier to identify a possible Moat. You can either look at consistent or slightly increasing OPM. There is no magic number for OPM, but it depends on whether the industry is in a near-perfect competition, an oligopoly or a near-monopoly. Lower, but stable OPM is acceptable for industries like, say, FMCG or Auto. But note that companies like Eicher Motors are actually in the Auto industry, but cater to a niche segment in the Auto industry, so the company should ideally behave as if it operates in a near-monopoly. Stability in NPM is also a factor, but I don’t think historic NPM data is available in Screener. Either a low Debt/Equity (<1) or a higher (>3) Interest Coverage could also be used here.

-

Quality of Management: Determining the quality of a management team through financials sounds funny, but there are aspects which can be touched upon. Things like regular dividends, low other income as a percentage of total income etc can be considered. Dividend Coverage Ratio is also something you can manually create. Pledged Percentage and/or Change in Promoter holding is also something you can consider. But that would depend upon your own Risk-bearing tendencies.

-

Compounding Possibilities: The generic RoE, RoCE check and minimal Sales/Profit growth. I often use PGSG Ratio (Mentioned above) and the Cash-to-Capex Ratio as well. But I do not use them in the screens, but separately while reviewing individual companies from the Screen. The SGR is also something to look at. If a company grows at SGR, it maximizes value. If SGR < EPS Growth, then the company is not allocating its capital properly. If SGR > EPS, then that EPS Growth is not sustainable. Of course, don’t use SGR = EPS Growth, because it’s impossible for that to happen. You can probably keep it handy in order for comparison.

-

Valuation Comfort: I don’t believe in anchors like the PE or PEG Ratio to signify value. However, you do need a disciplined approach to investing. So consider using anything ranging from the PE, the PEG (I have a manually calculated PEGY - PEG with Dividend Yield included in the denominator), the P/B, the P/CF or the EV/EBITDA as a mechanical limit. But don’t be stringent. For ex: If I were to use the PE (I don’t), I would even go so far as 40 PE. Putting a downside limit would be advisable, however. Say, if a company is trading at 3 PE or 1 PB, there’s obviously something wrong with it. It could also be a wonderful value buy, but weight of reason would tell you to rather just avoid them. A perfect example would be Lycos Internet. It’s trading at ridiculously low valuation multiples, even when its financials are wonderful. The reason? The stock is highly manipulated and the management quality leaves a lot of be desired. These type of stocks could be avoided by using a lower valuation limit.

Note on Non BFSI Screens: I have separate screens for BFSI and non-BFSI companies. You can easily filter for BFSI companies by using a D/E > 4 or 5. But Ratios such as RoCE or OPM don’t work all that well for BFSI companies, because of Accounting practices. You could use Asset Turnover (Needs to be manually calculated) instead of OPM, PB for the valuation limit and RoA instead of RoCE.

Others: I use manually calculated Cash Conversion Cycle (Quality of Management), Expected Price (Valuation Comfort), Return on Investments (Compounding Possibilities), Owner’s Earnings (Warren Buffet fame), Working Capital Turnover (Quality of Management) etc., as well as an add-on display. But I have never used them to Screen stocks.

And with all the Ratios, I would say, consider using short or long term averages whenever available, as they weed out the noise. Religiously ignore using single-period Ratios. If Screener could implement calculating long term averages for all the financials, that would be wonderful. Unfortunately, that is not an option with many of the important Ratios to be honest. I’m not complaining, but that improvement would make my Screening process way more efficient.

As a final note, the acid test for a good screen, in my opinion is that it should list companies which are already identified as wonderful companies if you tweak around the valuation ratios and maybe loosen the limits on some of your other ratios. For Ex: If I do that on my Non-BFSI Screen, I get companies like Symphony, MRF and HCL Tech, so I know that my Screen is somewhat useful is eliminating the waste.

No Screen is perfect, but if your screen hits somewhere close to the companies which are already great, you can modify your search criteria to find that one specific company among the lot which the market has somehow missed. From, you can proceed with research and valuation.