Company Background:

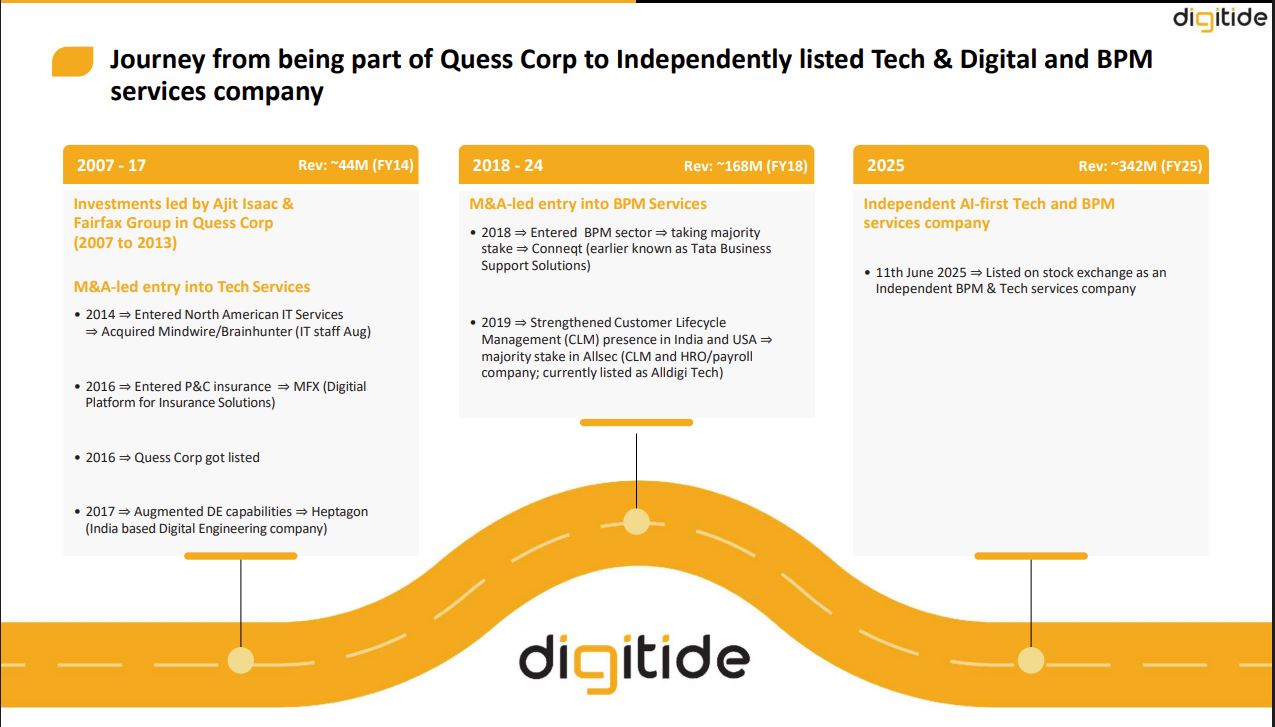

Digitide’s roots lie in Quess Corp, where digital services grew into a powerful capability, building full-scale platforms, delivering enterprise-grade Al solutions and managing critical operations for global clients across various industries. As these capabilities deepened, the need for a distinct digital identity became clear and Digitide was formed in 2024 following the strategic demerger of Quess Corp.

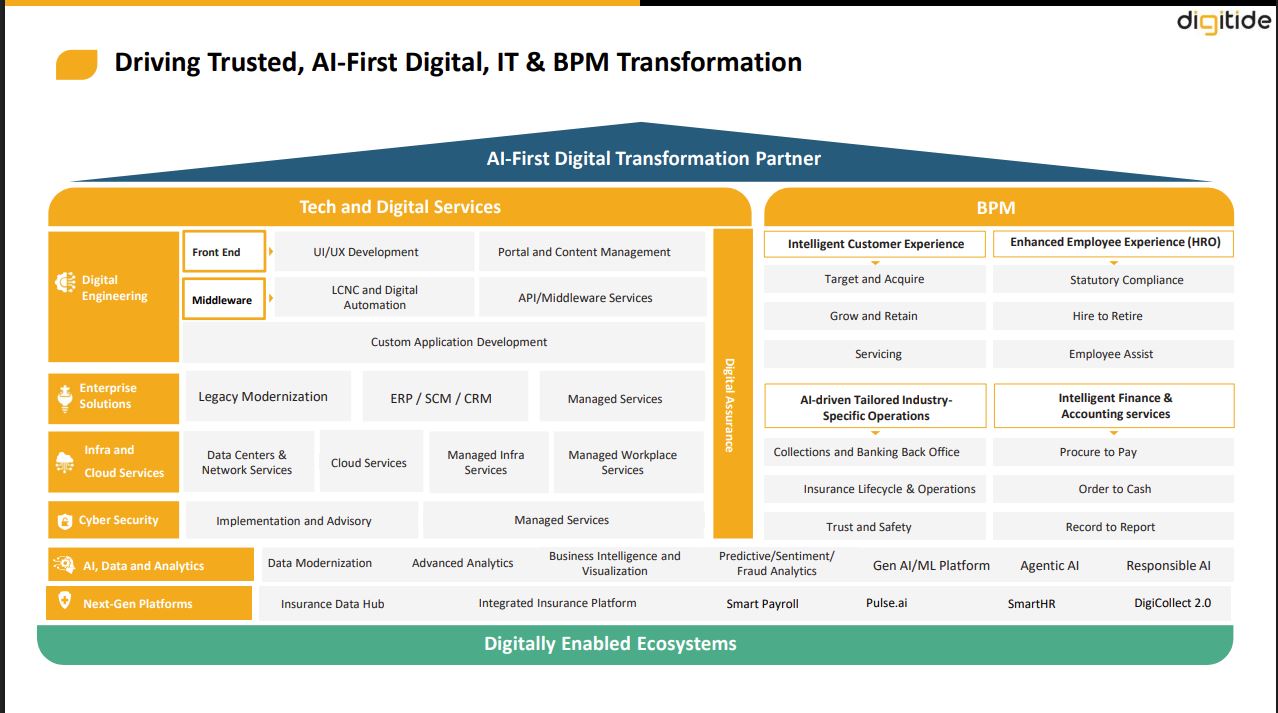

Today, Digitide operates in two broad categories, BPO Solutions and Digital & Tech Business. Business Process Management (BPM) Services remain a cornerstone of Digitide’s performance, contributing 73% of FY25 revenue. BPO portfolio spans Customer Experience Management (CXM), intelligent Back-Office processing, Collections, and seamless Employee lifecycle management solutions engineered to deliver operational efficiency, accuracy, and measurable results. Their core capabilities in BPO solutions include Al-Powered Digital CCaaS, GenAl-Led CX Management, Future-Ready Collections, Back-Office Operations. and Employee Experience Management.

Tech & Digital Services form the innovation backbone of Digitide, focused on building the digital enterprises of tomorrow. Contributing 27% to FY25 revenue. Their core capabilities in this segment include Accelerated application development with Gen Al powered low-code platforms enabling faster deployment, reduced complexity, and intuitive workflows, Intelligent quality engineering through Al-enabled digital assurance, script-less automation, and comprehensive performance testing, Al-driven insurance platform streamlining the policy life cycle with automated workflows, real-time data validation, regulatory compliance, faster delivery, and 24/7 customer support, Unified API integrations and platform-based engineering that eliminate silos, automate processes, and enhance business interoperability, Al-first digital experience transformation (TX) to modernize legacy systems and deliver scalable, customer-centric applications, Smart enterprise modernization through intelligent automation, cloud migration, and Al-integrated infrastructure upgrades. End-to-end cybersecurity built-in including Al driven threat protection, Zero Trust frameworks, identity governance, and 24/7 response. End-to-end SAP solutions including implementation, migration, testing, and automation to optimize enterprise resource planning. Gen Al integrated across service lines enhancing CX, data analytics, digital assurance, and application development for faster, smarter outcomes. Evolving from infrastructure management to Al powered, cloud-native platforms that drive resilience, scalability, and optimized performance.

(Source: Annual Report)

Business & Geographic Mix:

By Business:

• BPM: ₹545 Cr (69.8%)

• Tech & Digital: ₹236 Cr (30.2%)

Geography:

• International: 37.4% of revenue

• Domestic: 62.6%

(Source: Q3FY26 Presentation)

Financials:

TTM Revenue Figures (Consolidated):

- Revenue: 3013 Cr

- EBITDA: 337 Cr

- PBT: 35 Cr

- PAT: 9 Cr

- (PAT is suppressed due to one time Labour & Gratuity related one time exceptional expense in Q3, and few demerger related items in Q1 and Q2)

Q3 Revenue Figures (Consolidated):

- Revenue: 780.30 Cr

- EBIDTA: 87.55 Cr

- PBT: 4.02 Cr

- PAT: -2.05 Cr

- Ad PAT: 24 Cr

- (PAT is low due to one time exceptional items related to Labour and Gratuity)

KEY BALANCE SHEET & CASH Figures:

- Total Shares Outstanding: 14.9 CR

- Borrowings: 49 Cr

- Lease Liabilities: 378 Cr

- Cash & Investments: 164 Cr

- Key Business & Financial Metrics:

- TCV booking of 662Cr in Q3 (Highest)

- Revenue growth of 6.5% YoY and 2.1% QoQ

- 18.6% YoY growth in Tech & Digital revenue

- 10.5% YoY growth in International business

- Improved cash flow realization (from 82 to 79 DSO)

- 34 key logos won during the quarter

- Hyperscaler partnership with all three big ones AWS, Google and Azure

Management Guidance:

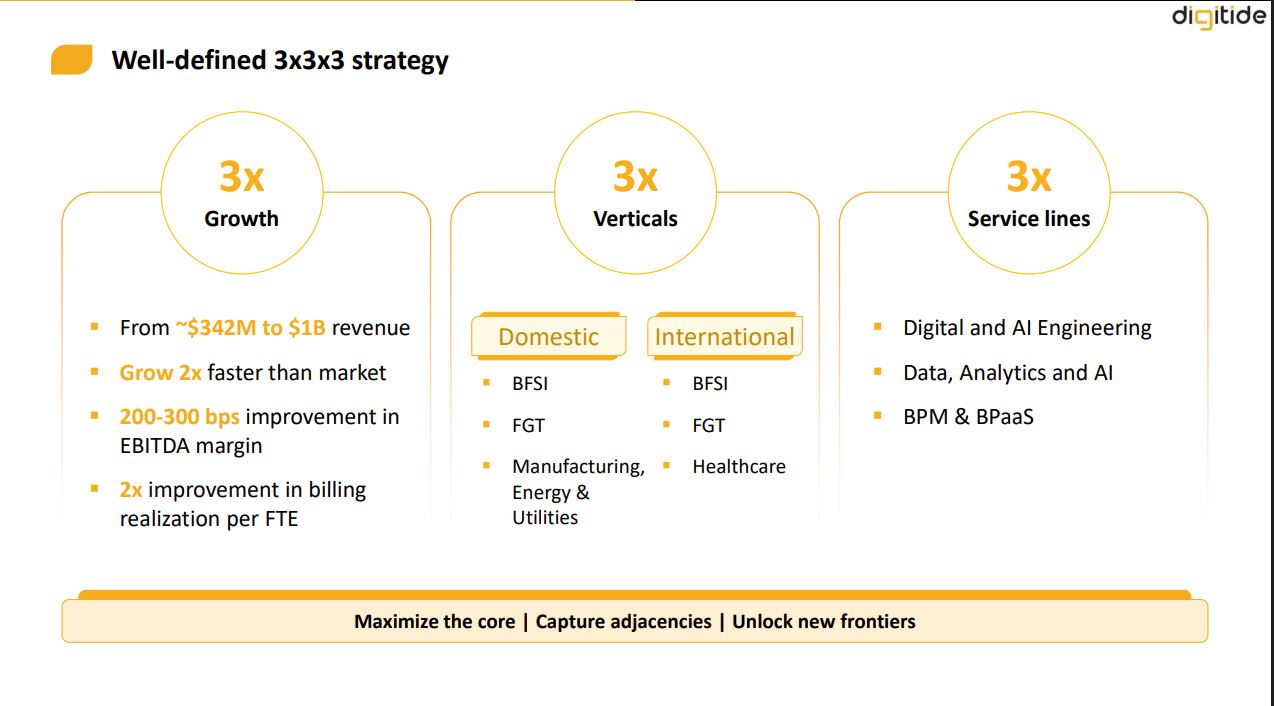

Management is guiding for 1 billion revenues in FY31 by the means of double-digit revenue growth, and also by inorganic route via acquisitions. They have repeatedly mentioned in concalls of shifting business mix more toward Tech & Digital side and also increase export mix. In contracts as per management 70% of TCV gets converted to revenue in subsequent year and rest in remaining two years, totaling to 3 years for complete conversion of their TCV. Also as per management, 70% of their business is annuity business.

Key Risks:

- Domestic BPM Margin Pressure

Large part of revenue still comes from domestic BPM.

This is:

• Labour cost sensitive

• Competitive

• Lower margin

If Tech mix does not increase meaningfully, margin expansion may stall. - Execution Risk on Growth

Management is targeting:

• Double-digit growth from FY27

• $1B revenue by FY31

That implies sustained execution across:

• Sales engine

• Cross-sell

• International expansion

• Inorganic acquisitions

Any slowdown in TCV conversion will affect growth visibility. - Inorganic Growth Risk

Management has indicated active inorganic strategy.

Risks:

• Overpaying for assets

• Integration challenges

• Margin dilution

• Cultural mismatch - AI Disruption Risk

- Customer Concentration

Top 10 customers contribute ~35%.

Loss of large clients could materially impact revenue. - Post Demerger Transition

Management has yet to prove their pedigree

Valuations:

• Market Cap: ~₹1,455 Cr

• EV: ~₹1,806 Cr

• P/E: ~44x

• ROE: ~15%

• CFO: ₹214 Cr

At ₹780 Cr quarterly run-rate:

Annualized revenue ≈ ₹3,100 Cr

EBITDA (annualized at 11%) ≈ ₹340 Cr

EV/EBITDA ≈ 5x (approx)

EV/CFO = 7.7x

Promoters & Holding Structure:

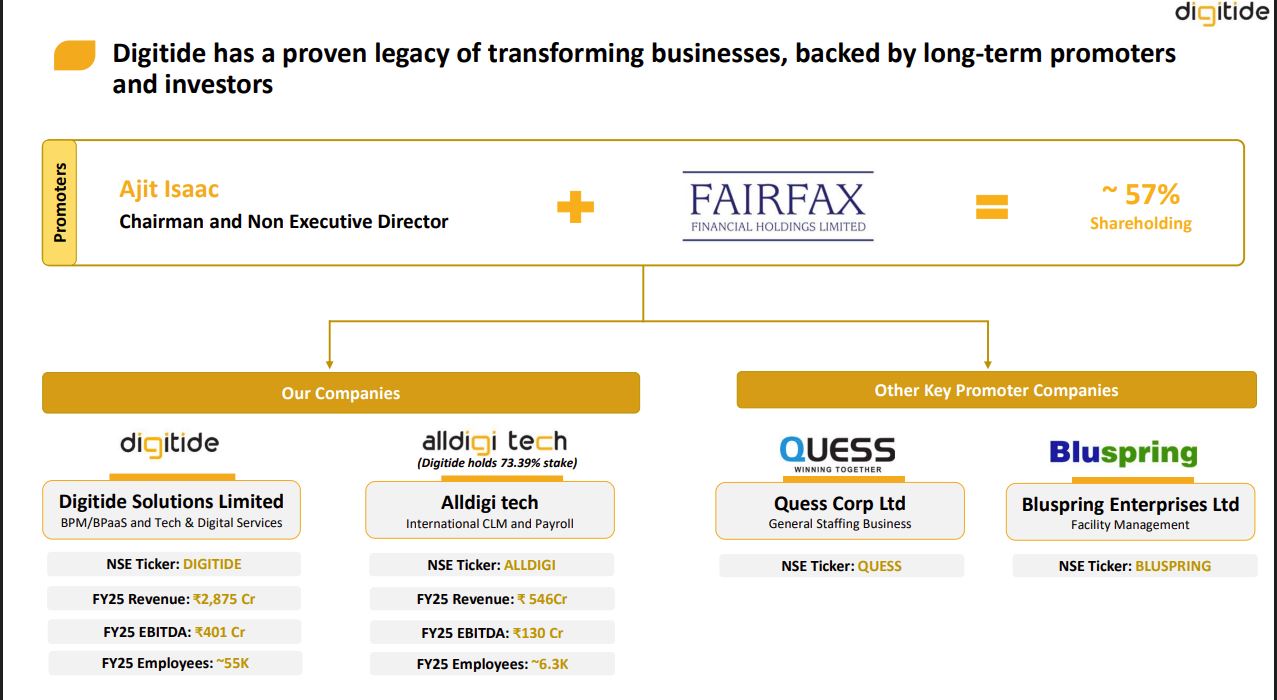

- Majority of the company is owned by Fair Fax Investment (Prem Vatsa aka Canadian Warren Buffet) at 34.14% along with original promoter Ajit Issac still holding 12.02%

- Company is run by professional management in all role, below mentioned are KMPs

Gurmeet Chahal: CEO (Ex- HCL Tech, Genpact, DXC Technology)

Saket Bhatnagar: International Head and Chief Revenue Officer (Ex- AWS, Accenture, HCL Tech)

Vinod Pahlawat: India Head (Ex- HCL Tech, Airtel, Motherson)

Sandeep Malhotra: Chief Strategy, Solutions and AI Officer (Ex- Coforge, Birlasoft, HCL Tech)

Mohan CK: Global Head of Operations & Practices, Tech & Digital (Ex- Accenture, Wipro)

Paresh Vankar: Chief Marketing Officer (Ex- LTIMindtree, HCL Tech) - FII Holding has decreased to 7.64% from 12.61% when it was demerged ( Seems it can continue for few more months)

- DII Holding seems steady at around 12%

- Public holding has increased from 20.97% to 23.38% (Ashish dhwan is holding 4.09% stake is steady)

Optionality:

- Double digits growth for next few years on a smaller base

- If Alldigi is merged with Digitide, as digitide holds 73% in all digittech.

- Cheap and strategic acquisitions to lookout for.

My Initial View:

If FY27 delivers 12–14% growth with margin expansion, stock could re-rate.

But execution for next 4 quarters is critical.

Looking forward to discussion.