Company name - DIGISPICE TECHNOLOGIES LTD.

Price - 29

Market cap - 670Crs.

The company was earlier engaged in the Information and Communication Technology business providing value added services and mobile content services to domestic/international telecom operators. The business was loss making and is still loss making.

Anyways what got me interested in the company was what work they have been doing for the past few years. The main revenue as of now for the company comes from an Application which they have developed for rural India SPICE MONEY.

So SPICE MONEY is essentially an application building a last mile digital services platform for rural India. So how it works is they have enrolled merchants and entrepreneurs in semi-urban and rural India on to their platform to serve as a human interface for the consumers in rural India and provide them access to the same services that the urban people enjoy. The entrepreneurs are attracted to earning potential the company offers as the company shares with them a part of the transaction fee which they receive from the businesses which are looking to reach out to service their customers in rural/semi-urban areas using digital channels. These entrepreneurs are spice money adhikaris.

A few points to note about the Spice money business -

-

The company as of now has a network of 1 million or 10 lakh adhikaris on their platform.

-

The adhikaris are present in all the districts and almost every pin code across the country.

-

The GTV (Gross Transaction Value) was around 82000 crs in FY 21 and is expected to cross 1lk crs. in FY22

-

The main reason for growth in transactions and GTV was on account of growth in cash withdrawal transactions from DBT (Direct Benefit Transfer) accounts.

-

The Aadhar enabled Payment System (AEPS) run by NPCI is the backbone on which the company runs its cash withdrawal services.

-

The company has a share of around 16.5% of the AEPS market.

-

The app also handles utility payments like electricity, water, gas, telecom, insurance etc.

-

The app also handles cash management services for microfinance companies, NBFCs and for banks to a certain extent.

Company also has a travel related product for Rural India called Travel Union. It is a B2B traveltech platform targeted towards travel agents in small towns in partnership with Sonu Sood.

Ok now lets look at the business front -

-

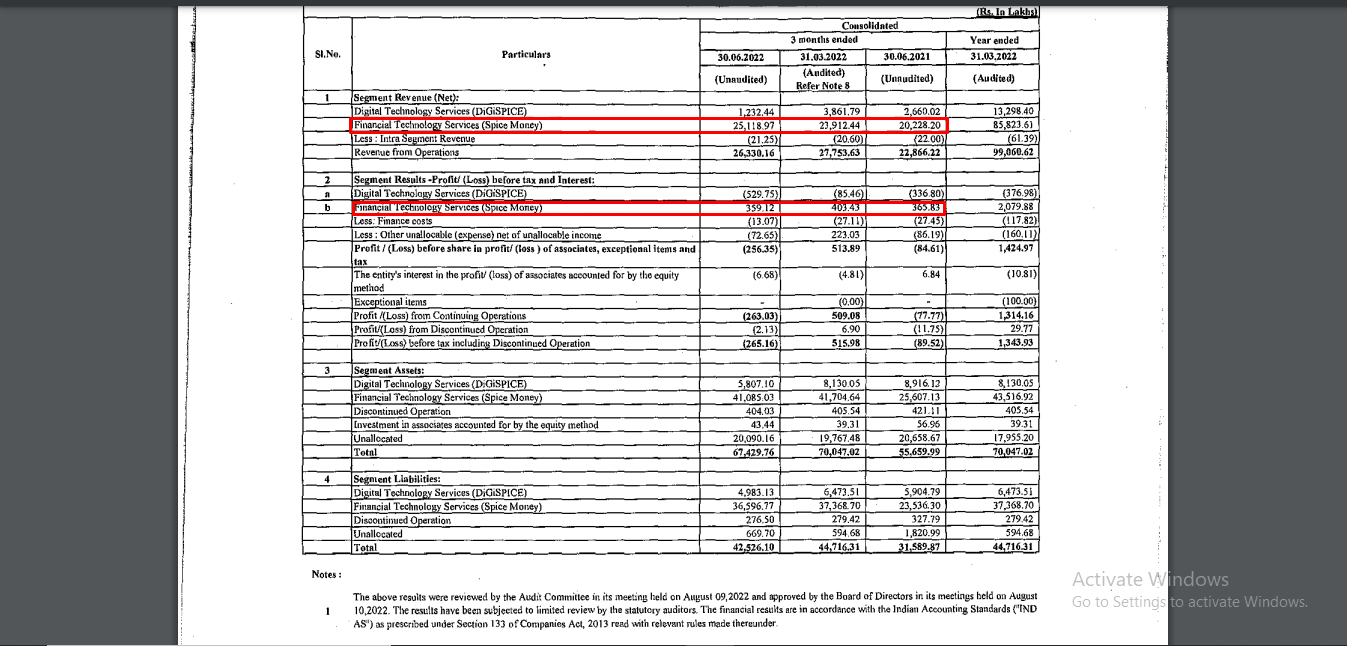

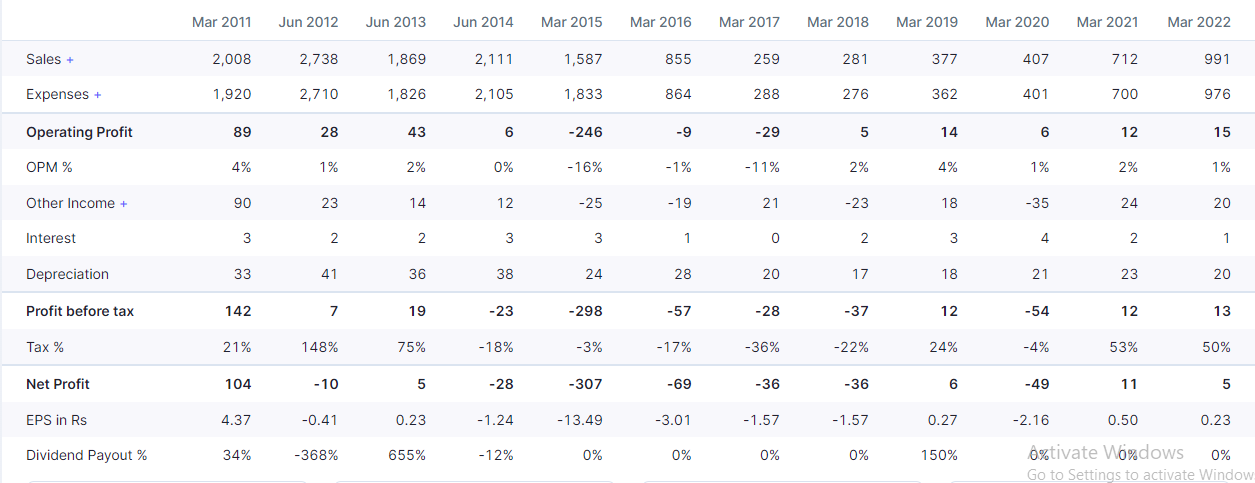

Over last 2 years revenue has grown from 407crs to 712 crs in FY21 and to 990crs in FY22. Growth has been driven mainly by Spice money where revenues have grown from 250crs to 850 crs in 2 years.

-

EBITDA has moved from 7crs in FY20 to 14crs in fy22 driven mainly by spice money. Current EBITDA is not reflective of the potential EBITDA since the company continues to be in a growth phase.

-

Spice money now contributes 87% of the total revenue in FY22.

-

Rural india has 336 million internet subscribers and rural india has 20% more internet users then urban India. Smart phone availability in rural india has doubled in the last 3 years.

-

Right now the company is continuing to balance between growth and profitability. Operating leverage will come with growth.

-

The whole business model is centered around enabling the adhikaris to serve the consumers more. The more they serve the more transactions there are on the platform and more data comes in. With more data the company gets opportunity to innovate new products and the new products then hits the platform in turn giving more opportunity to the adhikaris to service the consumer and this is the flywheel the company operates in.

-

Certain trends will emerge as rural India will get more digital and the company is in the right ecosystem to take advantage of the same.

Valuations -

Well I am not particularly sure how to value the company but at present the market is valuing the company below 1x sales whereas other platform companies are valued at probably 5-10x sales. So valuations I think is comfortable rest market is supreme.

Risks -

-

The telecom business has been a drag on the company. The company would be better off selling off the division.

-

Govt. Thrust towards DBT has been the main contributors of revenue any deviation from the govt can affect the topline.

-

Business requires continuous innovation and addition of newer products any shift in focus will not be good for the company.

DISCLOSURE - INVESTED AND VIEWS CAN BE BIASED. PLEASE DO YOUR OWN STUDY BEFORE INVESTING.

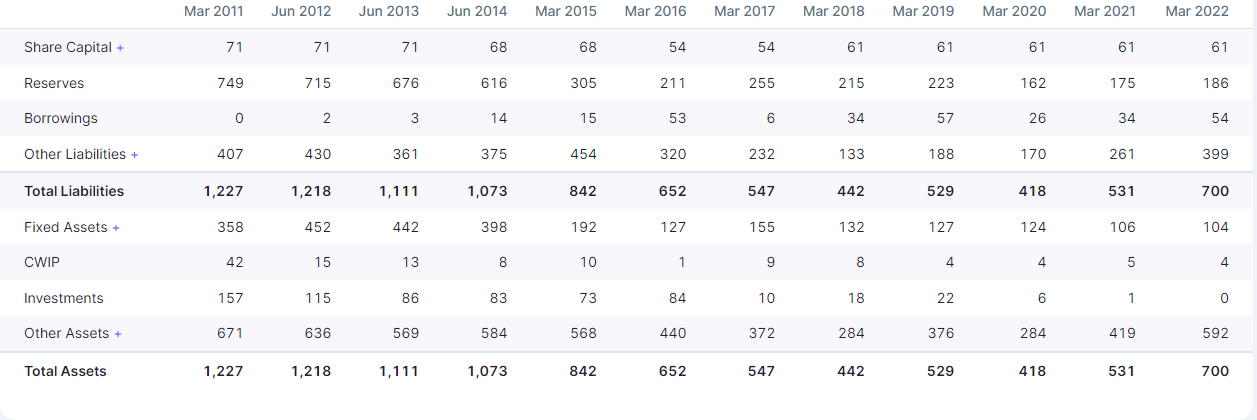

Below are the financials of the company and the balance sheet

P&L

BALANCE SHEET

CASH FLOWS