Company Name: Digikore Studios Ltd (DIGIKORE)

Website: https://digikorevfx.com/

CMP: 490

MCap: 310 Cr

No. of Shareholders: 1007 (Promoters: 66.54%, FII: 2.79%, DII: 7.89%, Public: 22.79%)

About the Company: Incorporated in 2000, Digikore Studios Limited is a visual effects studio that offers a full suite of visual effects services.

Business Profile: The company offers Visual Effects (VFX) services for Films, Web Series, TV Series, Documentaries, and Commercials and has a studio in Pune.

Services: Rotoscopy, Reflection Removal, General Cleanup, Wire and Wig Removal, Muzzle Flash, Composting, Green Screen Composting, MatchMove, Driving Camps, Day to Night, CG Blood Camps, Beauty Fixes, Crowd Multiplication, Set Extension

Projects: The company made its mark in animation and VFX. It worked with projects like “Thor” - Love and Thunder, “Black Panther” - Wakanda Forever, “Glass Onion” - A Knives Out Mistery, “Deadpool”, “Star Trek”, “Jumanji”, “The Last Ship”, “Titanic”, “Ghost Rider”, etc.

Approvals: The company has approvals from major production houses like Disney/Marvel, Netflix, Amazon, Apple, Paramount, Warner Bros., Lions Gate, etc.

Matchmaking Business: The company has started a new venture known as Digikore Matchmaking, which is the world’s first Televised Matchmaking Show hosted by Bollywood Celebrity Bhagyashree

Clientelle: Digikore Studios’ clientele mainly comes from India, Australia, New Zealand, the US, and European markets.

Geographical Revenue Bifurcation:

North America - 86% in FY23 vs 42% in FY22

Europe - 11% in FY23 vs 12% in FY22

Australia & NZ - 2% in FY23 vs 0.11% in FY22

Rest of the world - 1% in FY23 vs 46.5% in FY22

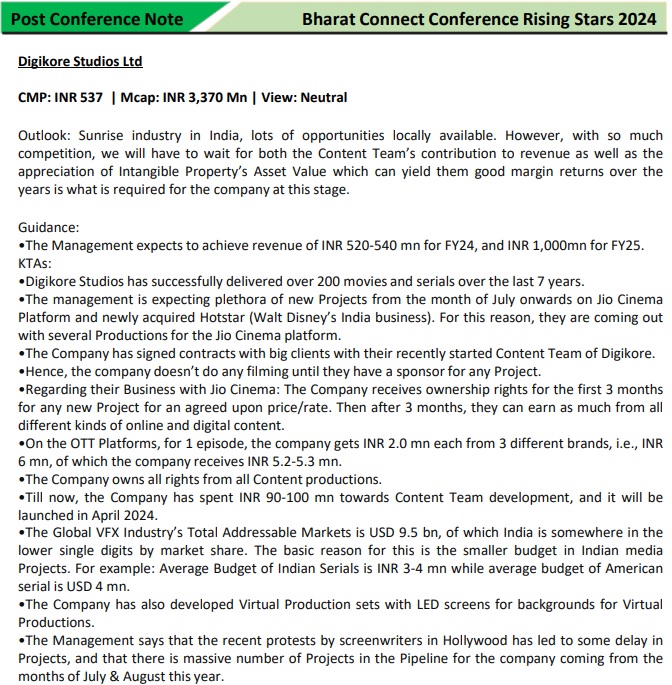

Takeaways from Q2FY24 Concall and Q3FY24 Investor Presentation

If one looks at their screener page, they’d find this stock to be trading at a PE of 71. However, this is based off the FY23 Net Profit data. I confirmed this from the H1FY24 EPS of 9.85 mentioned in screener.

H1FY24 - Net Profit: 6.24, EPS: 9.85

FY23 - Net Profit: 4.37, EPS: 9.85 * (4.37/6.24) = 6.90

PE = 490/6.90 ~ 71

If I extrapolate the H1FY24 performance for FY24, the EPS would come to 9.85*2 = 19.7, giving us a current/TTM PE for FY24 of 24.87. There is most likely going to be some more growth in H2FY24 relative to H1, leading to an even lower PE, but for now let’s assume a linear projection.

This gives me an attractive valuation, given how its peers command a PE of greater than 20:

Prime Focus: 20.66 (TTM -16.90)

Basilic Fly Studios: 31.23

Phantom Digital Effects: 40.49 (TTM 29.31)

Now, let’s look into the projections given by the compny’s management. If we see the Investor Presentation PDF released in Jan 2024, on page 39, we can find the management forecasting a revenue of INR 120 crores by FY26. This would be 2.4x from current figures (again, I’m going by extrapolating H1FY24 sales).

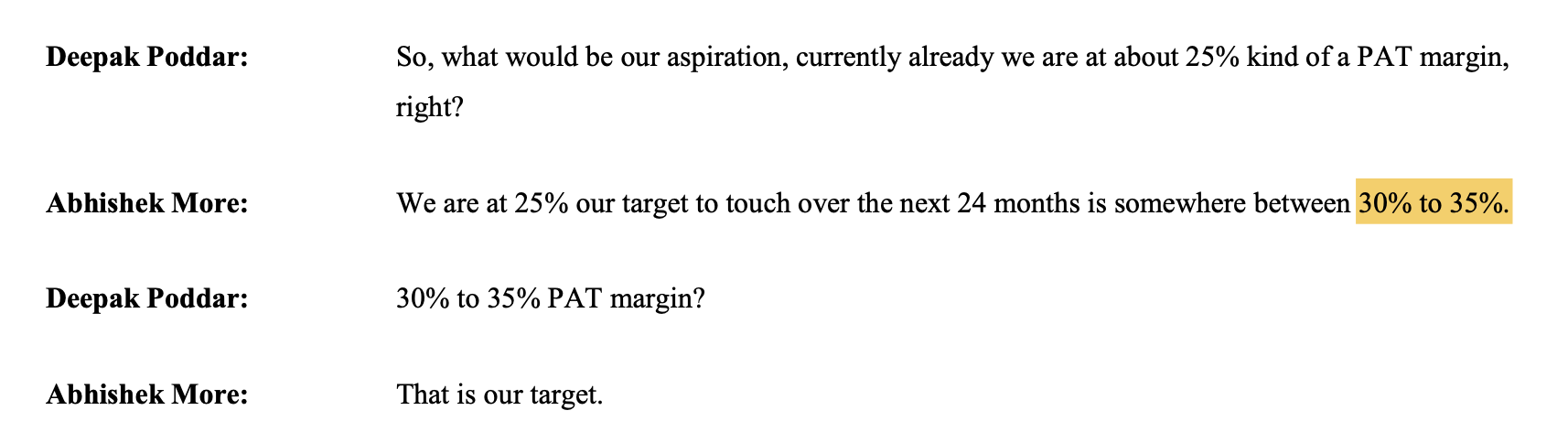

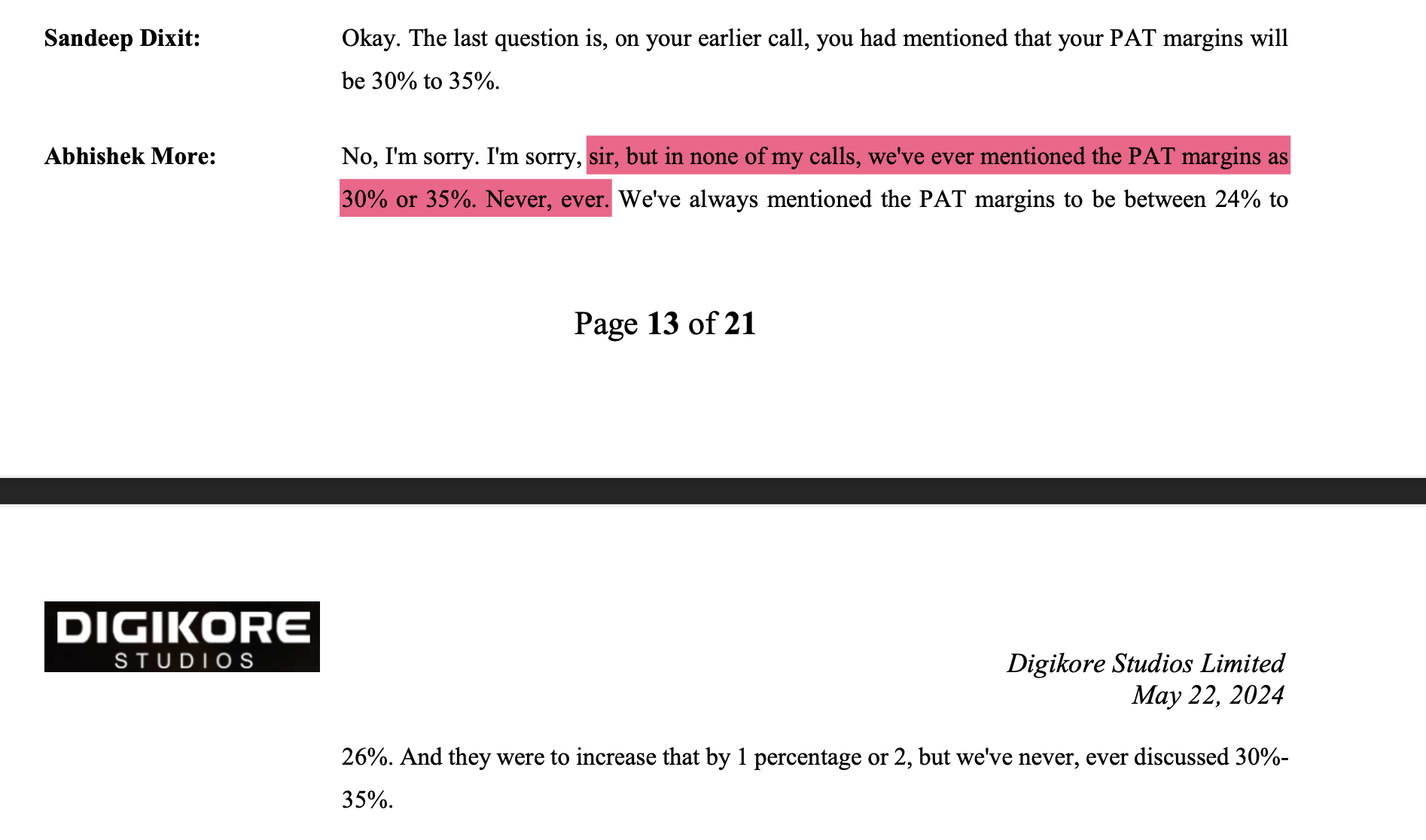

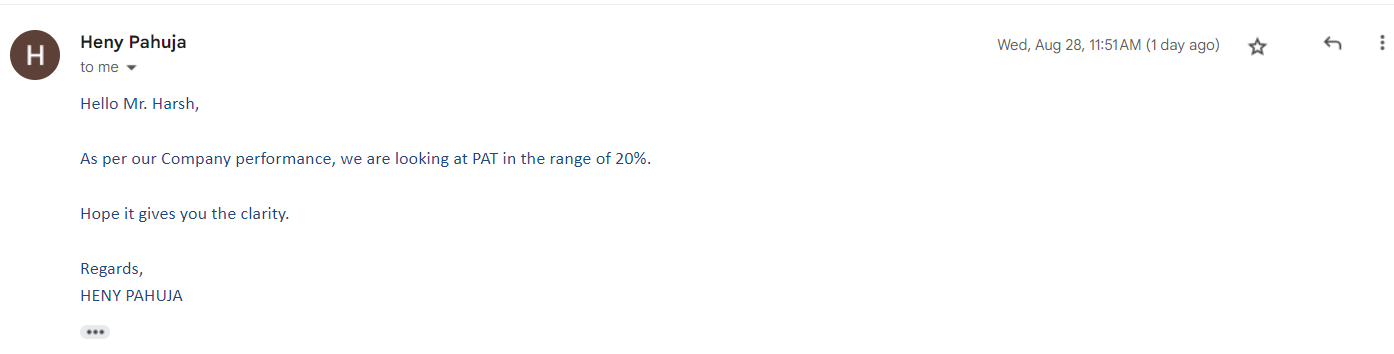

Also, on page 8 of the concall transcript of Nov 2023, their CEO Abhishek More says that the company will target a PAT margin of 30%-35% by FY26. This means a PAT of 36 cr to 42 cr, taking the EPS between 56.83 (at 36 cr PAT) and 66.30 (at 42 cr PAT). Calculating the forward PE at current price, we get something between 8.62 to 7.39. This is mouthwatering value, and assuming no PE rating change, a price target of 1420 to 1657 at 25 PE can be expected in the next two years.

Disclosure: I am not a SEBI registered analyst. Please do not consider this post as a buy/sell recommendation. Unfortunately, since it is an SME stock, buying a tracking position in this stock is beyond my budget. However, I would have bought it if I could afford.