Companies have started adopting IND-AS instead of GAAP. Is there any substantial differences between the 2 methods ?

I do some work on the Revenue Recognition side of these changes (similar rule changes are rolling out in the USA). From the RevRec perspective, companies which long-term contracts or those working on a project basis (e.g. engineering, realty) will be affected. Many companies will show lower revenues since multi-year sales will now be pro-rated over the life of the contract.

I think there might be opportunities when uninformed investors lose faith due to ‘poor’ results, not realizing that the company’s fundamentals have not changed, - just the way they are counted.

5 Likes

Can the change in accounting method from Indian GAAP to Ind-AS also lead to higher revenue numbers for the previous year when recalculated as per Ind-AS?

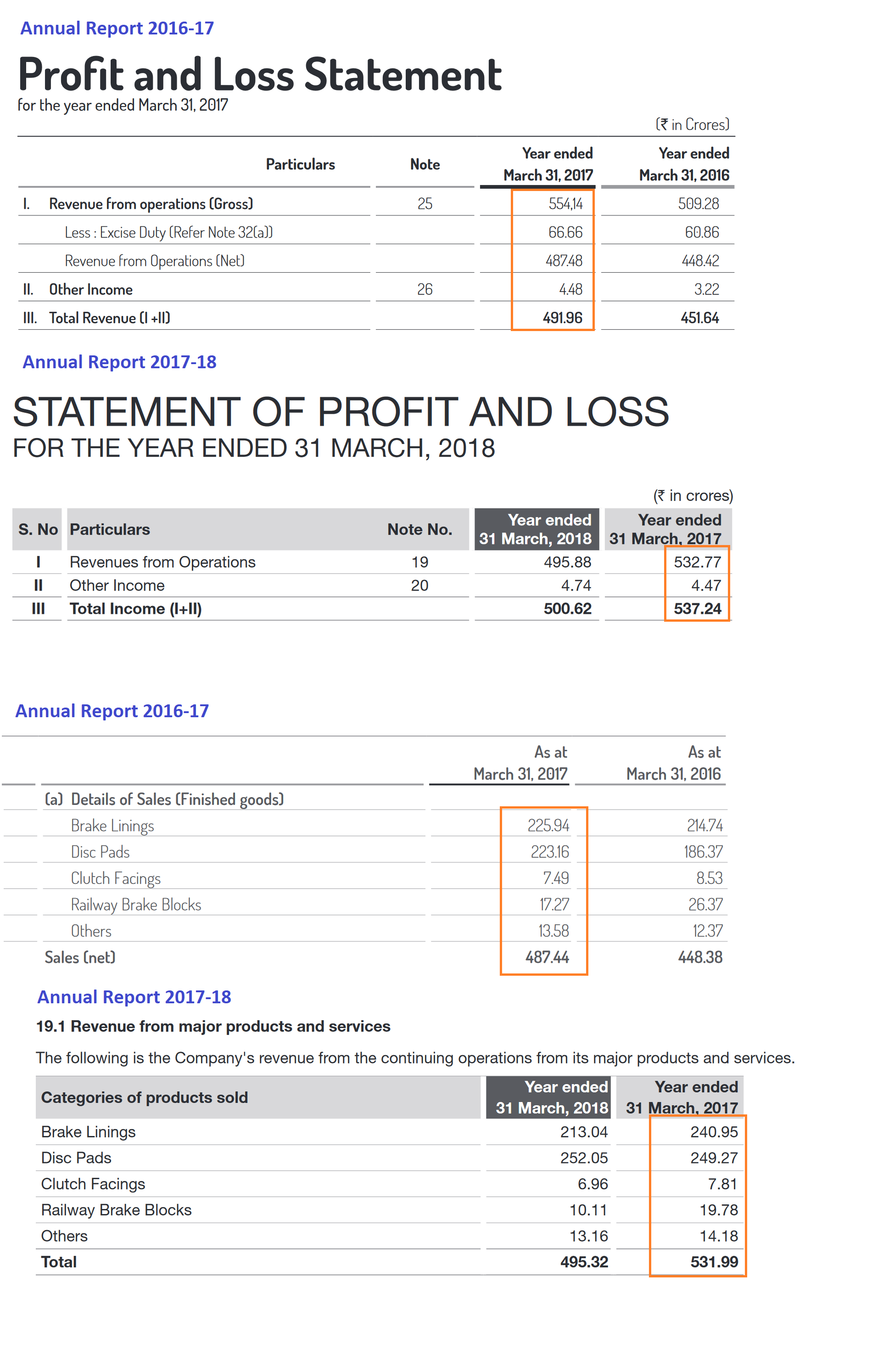

For example, please see below the discrepancy I noticed in the 2017 revenues of Rane Brake Linings Ltd. as reported in Annual Report 2017 and Annual Report 2018.

Even if we go into the notes, the discrepancy is not addressed and the segment wise revenues are different too.

What could be the reason behind this discrepancy?

1 Like