Sharing some notes on the company if one wants to study from scratch. The company is coming out of bankruptcy with new promoters and is present in sector which is going through tailwinds. Also they are focusing on capacity expansion as they can see the demand in transmission sector.

Company Profile:

Diamond Power Infrastructure Ltd. (DPIL) is a leading integrated solutions provider in the power transmission and distribution (T&D) sector in India. Established in 1970 by Mr. S N Bhatnagar as a conductor manufacturer, the company has expanded its operations to include manufacturing of power cables, transformers, transmission towers, and providing EPC services. DPIL is headquartered in Vadodara, Gujarat, with multiple manufacturing facilities across the region.

Product Portfolio:

- Conductors: Offers a range of conductors including EC Grade Aluminum Wire Rods, Aluminum Alloy Wire Rods, AAC, AAAC, ACSR, AACSR, and more.

- Cables: Manufactures low, high, and extra-high voltage cables under the brand name "DICABS”.

- Transformers: Produces power and distribution transformers up to 220KV.

- Transmission Towers: Designs and manufactures durable transmission towers.

Business Operations:

- DPIL operates across various segments including cables, conductors, transformers, and transmission towers.

- The company provides turnkey services for transmission and distribution projects, including planning, design, procurement, erection, and commissioning.

Resolution Plan

- Approval and Successful Resolution Applicant: The resolution plan was approved by the Committee of Creditors (COC) on January 6, 2022 and subsequently by the National Company Law Tribunal (NCLT), Ahmedabad bench, on June 20, 2022. The successful resolution applicant was a consortium led by M/s GSEC Ltd in partnership with Mr. Rakeshbhai R. Shah and affiliate groups.

- Takeover and New Management: The new management, led by the successful resolution applicant, took over the control of the company on September 17, 2022. This triggered the reconstitution of the Board of Directors.

- Financial Restructuring:

- Payment to Creditors: The resolution applicant proposed to pay a total of ₹501 Crore against the total admitted claims of ₹3308.88 Crore. This amount was to be paid in various forms, including upfront cash and unsecured redeemable bonds.

- An upfront cash payment was made to the Financial Creditors on the trigger date, September 17, 2022.

- The first instalment of ₹30 Crore was paid to Secured Financial Creditors on March 17, 2023.

- The fourth instalment of ₹29.87 Crore was paid to Secured Financial Creditors on March 16, 2024.

- Unsecured Redeemable Bonds: Unsecured redeemable bonds aggregating to ₹1900 Crore with a coupon rate of 0.001% per annum were issued to the Secured Financial Creditors. These bonds have a maturity period of 30 years, and the company holds the right to repurchase them at their Net Present Value (NPV) discounted at 16% per annum at any point within this period. The NPV as of the takeover date was around ₹25.67 Crore.

- Term Borrowing Liabilities: Term borrowing liabilities of ₹367.41 Crore (after a payment of ₹29.70 Crore) were to be paid to secured financial creditors within a total period of 5 years.

- Resolution Cost and Other Payments: Part of the ₹501 Crore was allocated towards resolution costs (₹20 Crore), operational creditors (₹5 Crore), and employee liabilities (₹2.40 Crore).

- Share Capital Restructuring:

- The existing equity share capital was reduced by 99% w.e.f. September 17, 2022.

- 5,00,00,000 new equity shares of ₹10 each at par were issued and allotted to GSEC Ltd and its affiliates on September 17, 2022, amounting to ₹50 Crore.

- The preference share capital was fully extinguished.

- The final paid-up equity share capital stood at ₹52,69,71,060 divided into 5,26,97,106 equity shares of ₹10 each.

- An offer for sale of 25,72,605 equity shares was executed to comply with minimum public shareholding requirements.

- Backward Integration: The plan aimed to leverage DICABS’s unique position as a manufacturer with facilities for cables, conductors, and transmission towers under one roof, enabling backward integration.

- Implementation Period: The period for the implementation of the Resolution Plan was stated as 60 months from the date of the order approving the plan (June 22, 2022).

- Binding Nature: The approved Resolution Plan is legally binding on the Company, its employees, members, creditors, including government authorities, guarantors, and other stakeholders involved.

- Accounting Treatment: Accounting adjustments, including write-offs of excess liabilities and impairment of assets relating to the pre-takeover period, were made with corresponding effects to the Capital Reserve account as per the approved plan.

Few Red Flags

- Historical Financial Distress and Resolution Plan: The company has a recent history of severe financial distress, culminating in a Corporate Insolvency Resolution Process (CIRP). While a resolution plan was approved in June 2022, the company underwent a significant financial restructuring, including a substantial haircut for previous creditors and a 99% reduction in existing share capital. This indicates that previous investments faced significant losses, and the long-term financial stability is still relatively new.

- Audit Qualifications and Disclaimers: The financial statements have a history of audit concerns.

- The FY23 Annual Report notes that the Statutory Auditors did not express an opinion on the financial statements due to a lack of sufficient appropriate audit evidence.

- The FY22 Annual Report also contained a disclaimer of opinion from the auditors for similar reasons, citing ongoing investigations and lack of access to historical records.

- While the FY24 Annual Report has a qualified opinion, this is subject to the effect of pending updates to the Property, Plant & Equipment register, including physical verification and reconciliation, and the related impact on depreciation and capital work-in-progress. These ongoing issues create uncertainty about the true asset values and financial performance.

- Low Credit Rating and Non-Cooperation: Credit rating agencies have consistently rated the company poorly. Brickwork Ratings has repeatedly given a rating of ‘BWR D’ and placed the ratings under ‘ISSUER NOT COOPERATING’ categorydue to the company’s failure to provide necessary information for rating reviews. This signifies a very high risk of default and a lack of transparency.

- Pending Legal and Regulatory Issues: The company has a history of legal and regulatory challenges. Although the new management believes they are protected under the IBC, there are still pending legal proceedings related to the Enforcement Directorate’s attachment of assets. Additionally, there are ongoing appeals related to past income tax demands. These outstanding issues could potentially impact the company’s financial position.

- Material Related Party Transactions: The FY24 Notice of Annual General Meeting proposes the approval of material related party transactions with promoter companies (GSEC Limited and Monarch Infraparks Private Limited, and Premjayanti Enterprises Private Limited) for FY24-25 and FY25-26, with values potentially representing a significant percentage of the company’s turnover. While these are stated to be on an arm’s length basis and in the ordinary course of business, investors should scrutinise these relationships for potential conflicts of interest or unfavourable terms.

- Recent Changes in Management: There have been several recent changes in the Board of Directors and Key Managerial Personnel, including resignations and appointments. While management changes are not inherently negative, frequent turnover, particularly in key roles like CFO and Company Secretary, could indicate instability or challenges within the organisation.

- Operational Turnaround Still in Progress: While the FY24 report shows a significant increase in revenue and a profit, this follows a long period of being largely un-operational during the CIRP. The sustainability of this turnaround and the ability to scale operations efficiently remain key concerns. The company itself acknowledges facing strong competition and volatility in raw material prices.

- Share Capital Structure Changes: The significant reduction and subsequent increase in share capital as part of the resolution plan have fundamentally altered the ownership structure and per-share metrics. New investors should fully understand the implications of these changes on their potential returns and the dilution that occurred for previous shareholders.

In summary, while the company has emerged from CIRP and is showing signs of operational recovery, a new investor should be mindful of the company’s distressed past, ongoing audit qualifications, very low credit rating, pending legal issues, significant related party dealings, and the fact that the operational turnaround is still relatively recent. Thorough due diligence and a careful assessment of these risks are crucial before making an investment decision.

Attachment of assets by ED

- Trigger for Investigation: The ED’s actions were initiated following a First Information Report (FIR) registered by the Central Bureau of Investigation (CBI) in March 2018. The CBI’s FIR alleged cheating of banks to the tune of ₹2654.40 Crores involving the Managing Director, Joint Managing Director, and other public servants.

- ED Case Registration: Based on the CBI’s FIR, the Enforcement Directorate, Ahmedabad (ED), registered a case under the provisions of Section 17 of the Prevention of Money-Laundering Act, 2002 (PMLA) in April 2018.

- Search and Attachment: The ED conducted searches at all of the company’s premises on 5th and 6th April 2018 and again on 9th April 2018. Subsequently, the ED issued a provisional attachment order for the properties of the company and its directors.

- Filing with the Court: The ED filed an ECIR (Enforcement Case Information Report) sheet on 22nd December 2018 with the Hon’ble Court of Principal District & Sessions Judge (Ahmedabad Rural) and Hon’ble Designated special court under the prevention of Money-Laundering Act, 2002, at Ahmedabad. The matter remains under legal proceeding.

- Impact on Resolution Plan: Despite the National Company Law Tribunal (NCLT) approving the resolution plan submitted by M/s GSEC Ltd in consortium with Mr. Rakeshbhai R. Shah on 20th June 2022, the Enforcement Directorate has not yet released the attachment on the assets of the company.

- Company’s Efforts: Diamond Power Infrastructure Limited has filed petitions with the relevant Honourable Courts, including the Supreme Court, seeking the release of the attachment on its assets. The company’s management believes that the new management and the assets taken over are protected under Section 32 of the Insolvency and Bankruptcy Code (IBC) and are therefore eligible for release from the ED’s attachment.

- Ongoing Legal Process: As of the latest reports (FY24 Annual Report and July 2024 Credit Rating), the matter concerning the release of the ED’s attachment remains an ongoing legal process.

Negative equity capital

Drawing on the financial statements in the sources, particularly the FY22 and FY23 Annual Reports, the book value of Diamond Power Infrastructure Limited (DIPL) is negative primarily due to a significant deficit in its other equity. This deficit has accumulated over time, largely stemming from substantial losses incurred by the company in previous financial years.

- Accumulated Losses: The Statement of Profit and Loss in both the FY22 and FY23 reports reveals substantial net losses. These losses are accumulated within the equity section, typically reducing retained earnings, which is a component of other equity.

- Impact of CIRP and Resolution Plan: The Corporate Insolvency Resolution Process (CIRP) and the subsequent approval of the resolution plan have had a significant impact on the company’s book value.

- The resolution plan involved a 99% reduction of the existing share capital.

- A significant portion of the liabilities owed to financial and operational creditors was written off as part of the resolution plan. These write-offs, along with the share capital reduction, were accounting entries directly impacting the equity section, often through capital reserves.

- As noted in the FY23 Annual Report, the company passed necessary accounting entries in compliance with the NCLT-approved resolution plan, writing off/back/adjusting creditor and liability amounts and adjusting asset values directly through the capital reserves account. This process, while restructuring the liabilities, did not necessarily eliminate the pre-existing equity deficit.

- Negative Other Equity: The balance sheets clearly show a substantial negative balance in “Other Equity”. This line item encompasses accumulated retained earnings (which are negative due to past losses) and the net effect of the adjustments made as part of the resolution plan impacting reserves. The reduction in share capital further contributes to the overall negative equity when not fully offset by positive reserves or future earnings.

In essence, the negative book value reflects the cumulative impact of years of financial losses and the accounting adjustments made during the company’s restructuring under the CIRP. Even after the fresh infusion of capital by the new promoters, the historical deficit in equity remains significant, resulting in a negative overall book value.

Now lets look at the future

The company is undergoing significant capacity expansion

*The correction in presentation at AL-59 conductor capacity, should be 1,00,000 KMS total capacity.

Medium Voltage (MV) Cables:

- In February 2025, the company commenced commercial production of one new Medium Voltage extrusion line at its Vadodara plant, capable of producing 175 kms of MV Cables per month.

- Prior to this, the company already had three MV Cables lines in operation.

- There was an ambitious plan to commence commercial production of six more MV Cables lines by September 2025, bringing the total to nine lines at a single location.

- With the commissioning of the line in February 2025, the company had four lines capable of making 600 kms of MV Cables every month, which was projected to increase to 1350 kms per month before September 2025.

- In June 2023, two CCV lines and one SIOPLAS MV cables line were commissioned.

- As of September 2024, three CCV lines were under commissioning.

- Further commissioning of two 11KV lines was planned for November 2024, and another two CCV lines were planned for commissioning between December 2024 and March 2025.

AL 59 Wire Rods and Conductors:

- In March 2025, DICABS announced the commencement of commercial production of its first rod mill to manufacture Next Generation AL 59 Wire Rods at the facility of its Wholly Owned Subsidiary Company in Vadodara. This mill has a processing capacity of 80 Mt per day, i.e., 2400 Mt per month.

- The subsidiary is setting up a Green Field project comprising 3 rod mills with a total daily capacity of 250 Mt per day, i.e., 7500 Mt per month, at an estimated cost of Rs. 55 crores, expected to be completed by June 2025.

- DICABS’s existing mill had a capacity of 1200 Mt per month. The addition of the new mill increased the company’s conductor top line substantially. The proposed production of the subsidiary is 75,000 MT per annum.

- The company also had plans for a new rods mill for EC grade aluminium with a capacity of 40,000 MTPA, expected around April-May 2025.

- DICABS was in the process of increasing its AL 59-HSSC next-generation conductor facility with in-house rod mills to a capacity of 72,000 kms / 100,000 MTPA.

- Throughout March 2024, significant conductor capacity was commissioned, including 36,000 kms per annum of 765 KV - 61 strand conductors (AL59/HSSC), 36,000 kms per annum of 37 strand conductors (AL59/HSSC), and 60,000 kms per annum of 7 strand conductors.

- Further commissioning of 765 KV - 61 strand conductor capacity (18,000 kms per annum each) was planned for September and December 2024, and March 2025.

EHV Cables:

- A hybrid CCV line for EHV cables up to 400KV was commissioned in June 2023. The company had a manufacturing capacity of 2000 kms per annum for EHV cables.

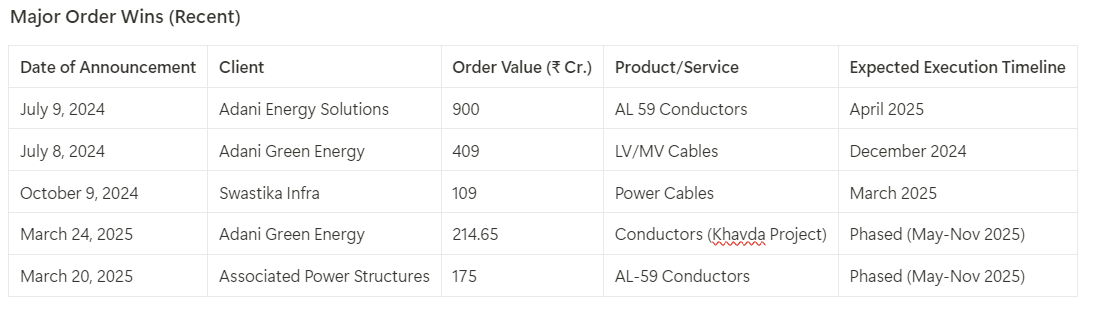

Recent Order wins

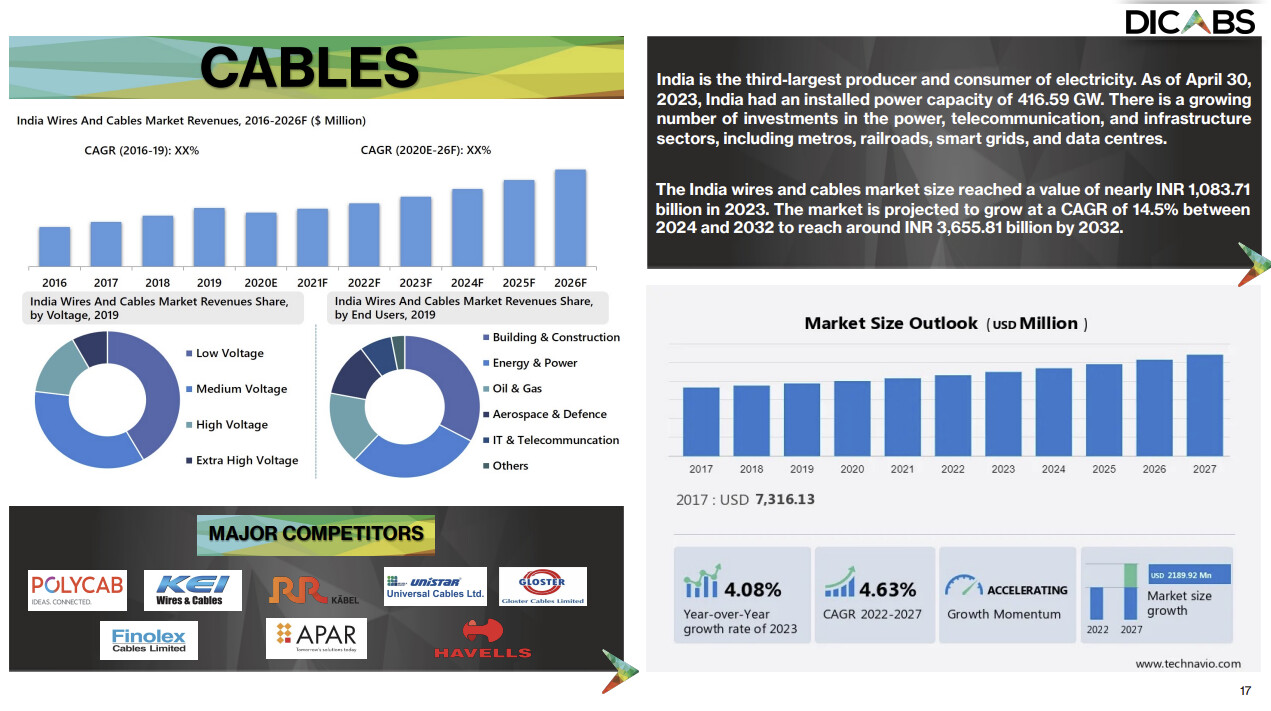

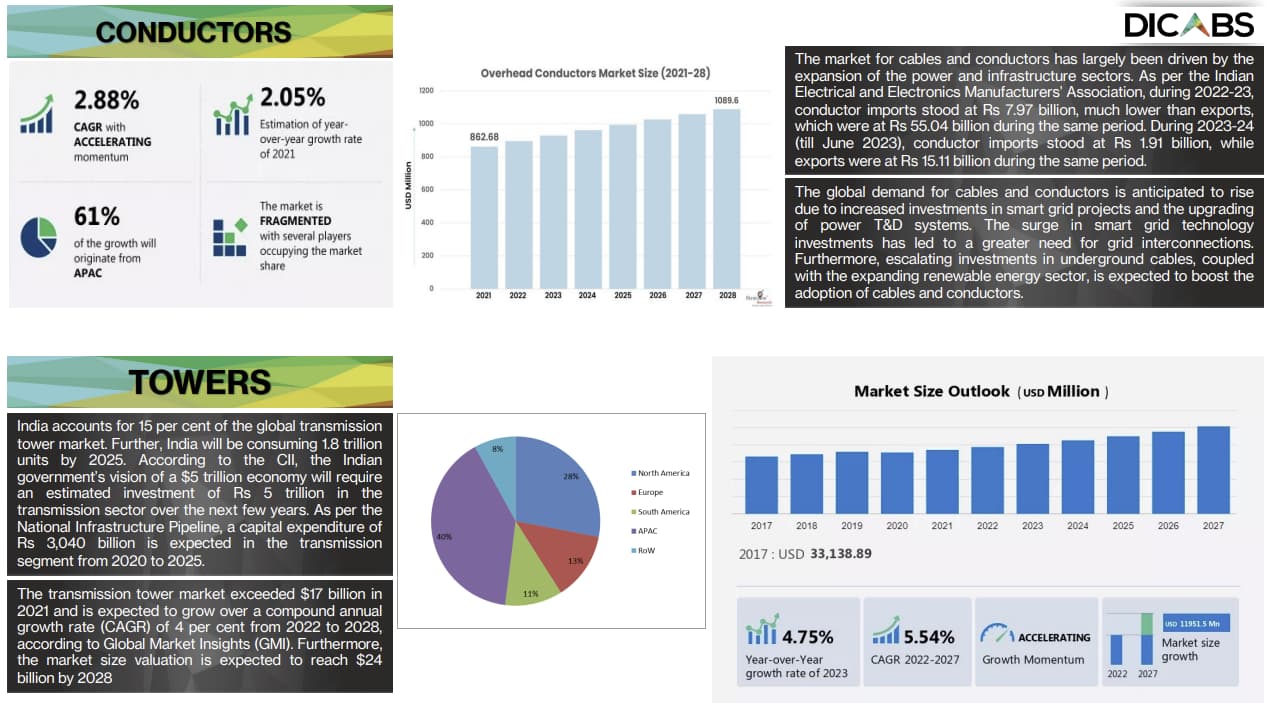

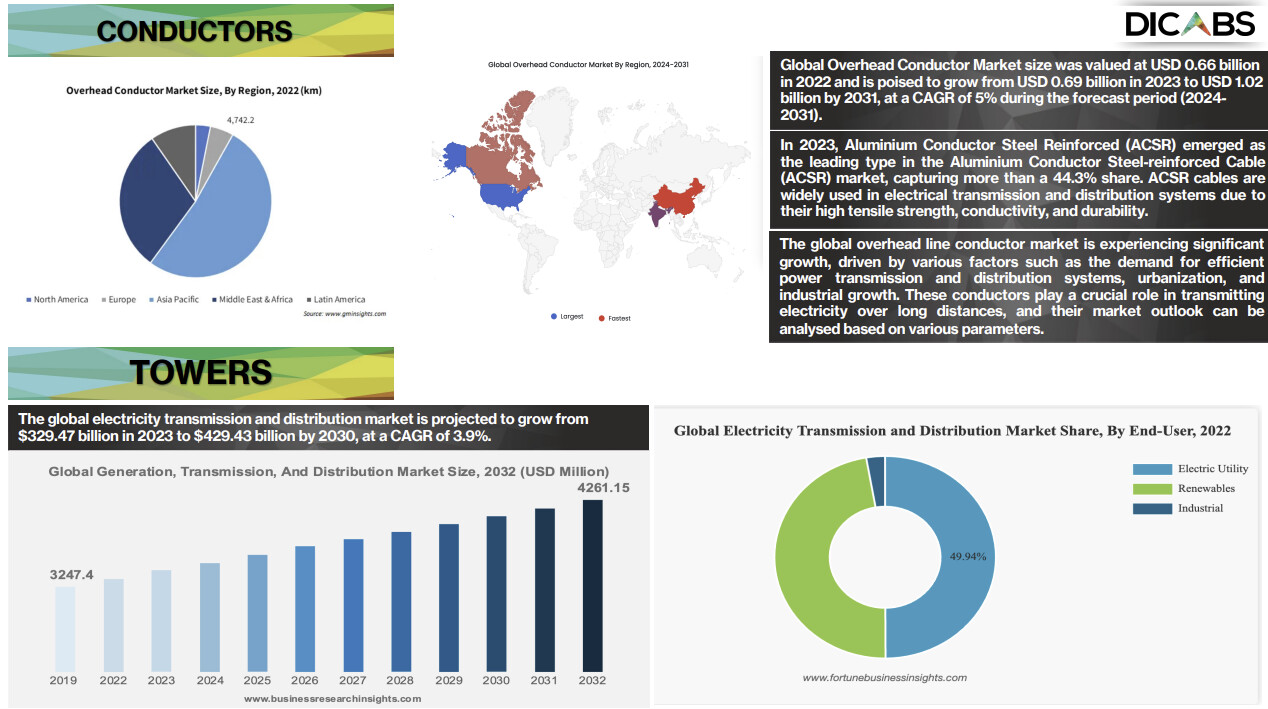

Industry growth as given in presentation