Background – DPL, promoted by Kolkata-based Dhanuka group, operates like a holding company with cash & cash equivalents of INR 222 crore as on Sep 30, 2018 and 50% stake in two operating PET resin unit along with the world’s largest PET resin manufacturer (Thailand-based Indorama Ventures Public Company Ltd). The details of two operating units in which DPL owns 50% stake is provided below:

a) IVL Dhunseri Petrochem Industries Private Ltd: operating 696 ktpa PET resin capacity in two locations – Haldia & Panipat

b) Egyptian Indian Polyester Company S.A.E: operating 540 ktpa PET resin capacity in Egypt. Restarted operation in August 2018 onwards.

Investment Rationale

-

Limited downside risk – DPL holds unencumbered cash & cash equivalents of INR 222 crore as on Sep 30, 2018 in its standalone balance sheet as against current market capitalization of INR 400 crore. Please refer to the audited balance sheet and H1FY18 result for reference purpose.

-

Second largest PET resin manufacturer in India (after Reliance) and top 15 PET resin manufacturer in the world

-

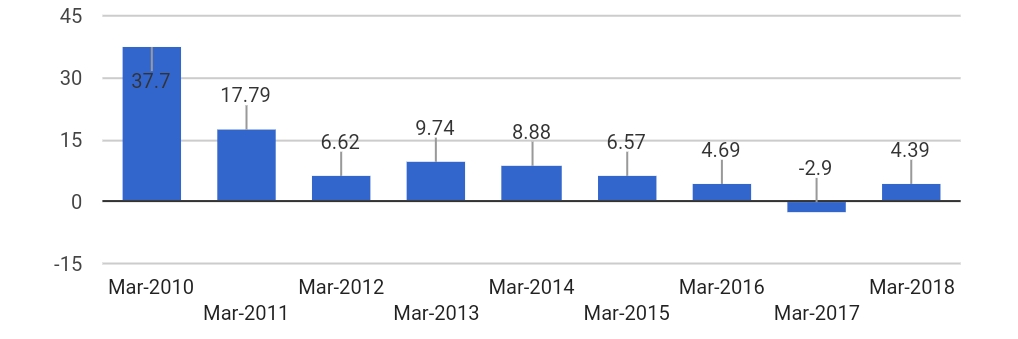

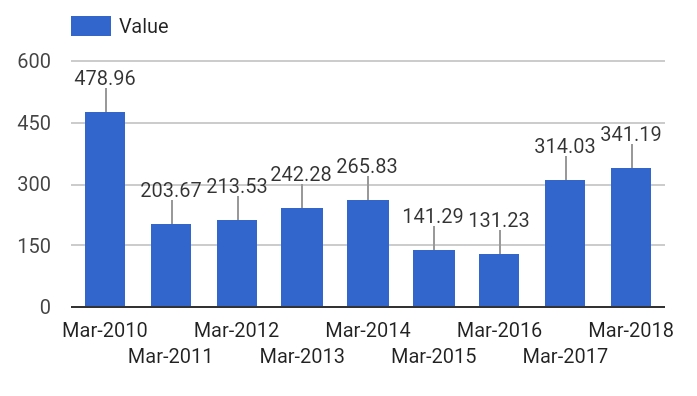

Highly profitable Indian operation (IVL Dhunseri Petrochem Industries Ltd) – The company owns 50% stake in a PET resin manufacturing operation in India, which is a cash generating business. The Indian business unit is generating quarterly profit of around $6-7 mn, translating to around INR 50 crore.

For FY16 & FY17 – please refer to http://www.careratings.com/upload/CompanyFiles/PR/IVL%20Dhunseri%20Petrochem%20Industries%20Pvt%20Ltd.-01-19-2018.pdf and

For quarterly data – please refer to quarterly MD&A section of Indorama Ventures: http://www.indoramaventures.com/en/investor-relations/downloads/mdna

-

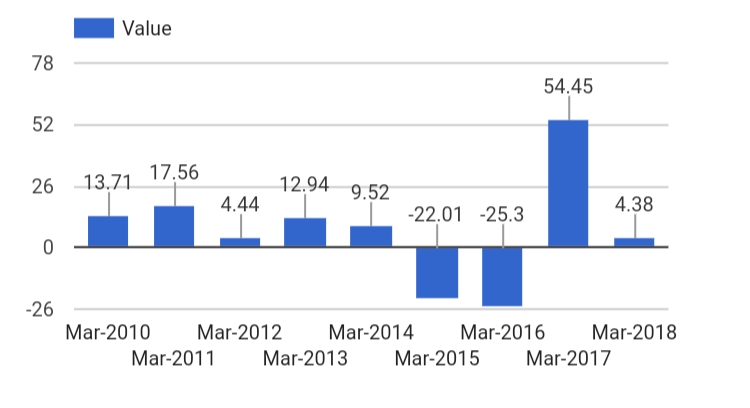

Restart of operation of Egyptian subsidiary ( Egyptian Indian Polyester Company S.A.E): The Egyptian subsidiary restarted operation in August 2018 and currently running at 50% capacity utilization. The plant is expected to run at full utilization by March 2019. At full capacity utilization, the plant is expected to generate topline of $500 mn and generate profit in the range of INR 100-200 crore.

-

Promoter accumulating stock from open market since June 2016 and near to 75% holding limit - https://beta.bseindia.com/stock-share-price/disclosures/insider-trading-2015/523736/

-

Valuation

Replacement cost model: The replacement cost of a new PET plant is estimated to be $600/t. Based on that the replacement cost of the Indian & Egypt JV unit is estimated to be INR 5400 crore. DPL has 50% stake in Indian & Egypt business, which comes to be INR 2700 crore. In addition, the company hold cash & equivalents of INR 222 crore. Egyptian subsidiary has no term loan and Indian subsidiary has limited term loan. Thus, the company’s valuation comes to be around INR 3000 crore. Assuming 50% holding company discount, the company can get a valuation of INR 1500 crore vs current market cap of INR 400 crore.

P/E model: The combined PAT of Indian & Egypt JV unit is estimated to be more than INR 300-400 crore in FY21, of which 50% DPL stake is estimated to be INR 150-200 crore. Applying 10x P/E multiple, DPL can get a valuation of around INR 1500-2000 crore. Assuming 50% holding company discount, the company can get a valuation of around INR 1000-1200 crore vs current market cap of INR 400 crore.

- Key Risks: Sharp volatility in crude oil prices or forex, extended winter season in western countries, poor corporate governance practices (ex- multiple restructuring in the past, poor information disclosure standards), low liquidity in the stock (as roughly 75% is owned by the promoters).

Disclosure: I have vested interest in the stock due to investments made through family members.