About the company: Dhruv Consultancy Services Limited (DCSL), incorporated in 2003 is a leading infrastructure consultancy firm specializing in highways and bridges. It offers design engineering, project supervision, maintenance, and advisory.

The company has 15% market share in the Indian Infrastructure Consultancy segment. The Company’s clients primarily comprise of government agencies like MoRTH, NHAI, UPEIDA, PMGSY among others. DCSL was present only in two/three states 3/4 years back (predominantly Maharashtra), now company has expanded its presence in over 25 states.

Products and segments:

-

It provides Authority’s Engineer, Independent Engineer and Supervision consultants (this was ~70% of revenues in FY23, EBITDA margins are in 10-15% range). As projects are tendered by government or government agencies, it is difficult to have governments own personnel in all projects. Hence, government agencies outsource this to agencies like DCSL. It has completed 1400km of Construction Supervision and is currently working on 2000 kms of highways all over the country. Revenues is billed on quarterly basis however there is lag of 45-60 days as invoice is raised post expense incurrence. Company has to incur expenses on resource mobilization few days/weeks before even the project kicks off. Resources/spending involved is rental paid on stay and commute of of personnel and other equipment’s used. However good things is that almost all of the onsite staff is on contract basis. So as soon as contract ends there is sharp fall (~80%) in numbers of staff, rent and/or salary paid. ~70-80% of contracted revenue is earned in 2.5 to 3 years, while rest is earned during defect liability period (also called as maintenance period) which is about 60 months. During maintenance period staff deployed will be only 20% of what was deployed during construction.

-

Detailed Project Report (DPR) also called as design engineering: It is a feasibility study covering: economic analysis, design of highway and structures, preparation of tender documents, land acquisition, forest clearances and utility shifting, environmental and social impact assessment. It has completed detailed project reports of 2000 kms. Revenue is recognized based on milestone basis. 15% of revenues and margins in 20-25% range.

-

Advisory business such as traffic survey – DCSL has robust expertise in carrying out technical audits using high-tech machineries namely Network Survey Vehicle (NSV), Falling-weight deflectometer (FWD), Horizontal and Vertical Retro reflectometer, Mobile bridge inspection unit (MBIU) and Automatic traffic counter-cum-classifier (ATCC). 5% of revenues and margins ~30%.

-

Others: design services, design of highway, design of structures that mainly provided for private contractors (margins ~40%).

Industry landscape: 20-25 consultants, top/tier-1s are Intercontinental Consultants and Technocrats Private Limited , RV Infrasolutions, Sa Infra, LN Malviya infra, and Dhruv Consultancy. Many of the smaller consultants have fallen off from bidding process as government tightened the requirements in the past few years. So main contenders are limited to less than ten owing to size and other requirements.

I want to highlight various red flags and risks. Please note that I have reached out to company for some of the questions and I am awaiting the response:

Red flags:

- Unbilled revenue (43 crores as of FY23) and receivables (18 crores) was ~75% of revenues (81 crores in FY23). I don’t understand why do we have such high numbers in unbilled revenues as they mention billing cycle is about 90-120 days. This also does not tie-up with their statement that unbilled revenues are mainly from IHMCL (~5% of revenues) and DPR (~15% of revenues). Hence, both segment account for 20% of revenues but unbilled revenue is over 50% of revenues.

- One of the promoter Prutha Pandurang Dandwate is continuously selling shares.

- Related parties are in adjacent or similar areas of business. In fact, in one of the interview company’s management talked about acting as financing support to related or relative’s companies who shall execute projects on their behalf (sub-contracting?)

- Couple of independent directors resigned two months back: https://archives.nseindia.com/corporate/DHRUV_05072023125805_OutcomeREG30DCSL.pdf

- Many relatives in board/senior management

Risks:

- Cash flows are highly concentrated and exposed to government agencies

- Political regime change in upcoming elections may result in change in transparency (in bids/tenders and payments) and pace of order flows

- Low liquidity in the stock

Order book: Order book is ~270 crores to be executed over next 3-years. Company expects 150-200 crores of order inflow during current financial year driven by pre-election increased activity. Company has already received 50 crores plus orders in the last two months. I have summarized below some of the recent orders below:

| Date of filing | Type | Order size (crore) | Contract period (month) |

|---|---|---|---|

| 30 August 2023 | Authority Engineer | 7.0 | 78 |

| 25 August 2023 | Independent Engineering Services | 6.0 | 48 |

| 23 August 2023 | DPR | 3.8 | 12 |

| 16 August 2023 | Independent Engineering Services | 9.4 | 48 |

| 31 July 2023 | Independent Engineering Services | 7.4 | 48 |

| 21 July 2023 | Project Supervision Services Agency | 1.2 | 12 |

| 15 July 2023 | Independent Engineering Services | 5.6 | 60 |

| 14 July 2023 | Independent Consultancy Services | 1.4 | 36 |

| 11 July 2023 | Authority Engineer | 9.7 | 84 |

Source: company exchange filings available on NSE

Talent mix: 300 engineers out of 400 total staff. CV of personnel needs to be on Infracon website (a government portal). Person cannot move anywhere before the completion of the project. 25% senior and 75% junior staff. 70% of staff is onsite and on contract basis.

Entry barriers – moderate levels

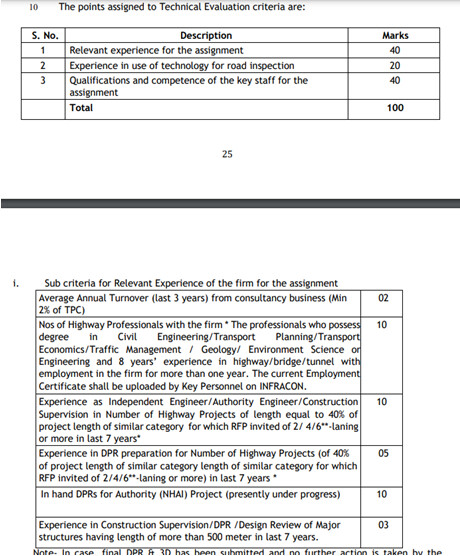

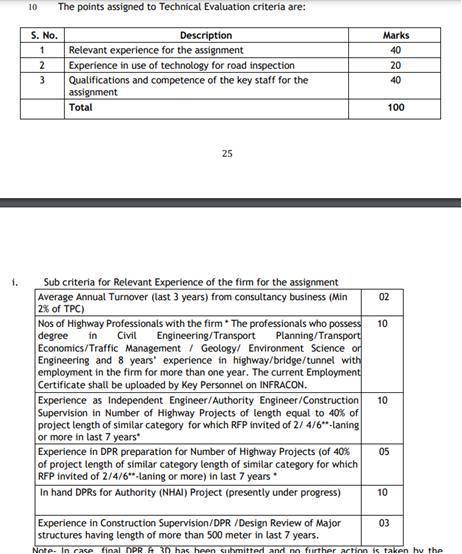

- Minimum Technical requirements for tender participation: an extract from tender terms below:

“The two parts of the proposal are Part1: Technical Proposal and Part2: Financial Proposal. For a given EPC Project, Stage -1 of the Evaluation shall consider the evaluation of the Technical Proposal (i.e. Part 1). The firms scoring the qualifying marks (minimum 75%) as mentioned in RFP shall only be considered for further evaluation. Under stage 2, the financial proposal of such firms as selected above shall be opened and evaluated. Proposals will finally be ranked according to their combined technical and financial scores as specified in clause 5 of section 2. The weightage of Technical and Financial score shall be 80% & 20% respectively. The final selection of the firm shall be based on the highest combined score of Technical and Financial Proposal”

Source: https://infracon.nic.in/WriteReadData/consultantprojectsAETWO/605_File3378349816.pdf

DCSL’s technical score has improved from 88 points 3-4 years back to 95 recently. I believe strong peers are close to ~97. DCSL expects to close the gap with its strong peers soon.

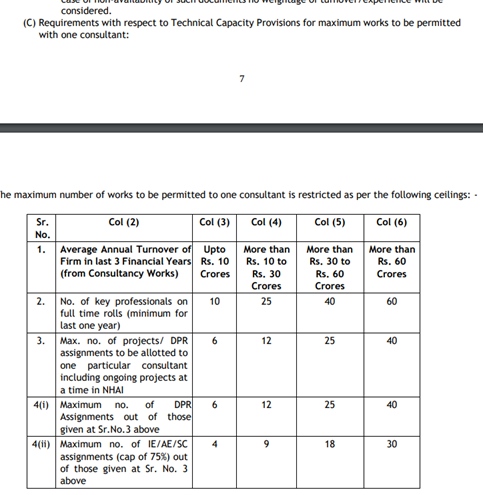

- Financial strength and size requirements: Tenders contain minimum size and experience requirements for participation:

Source: https://infracon.nic.in/WriteReadData/consultantprojectsAETWO/605_File3378349816.pdf

DCSL mentions that now their size is allowing them to have no cap on maximum orders they can get.

Requirement of bank guarantees another constraint for smaller players. Extract again below from tender:

“Bank Guarantees: PERFORMANCE SECURITY 7.1 The successful consulting firm shall have to submit a Bank Guarantee (BG) for an amount of 3% of the Contract Value within 15 days of issue of LOA. The BG shall be valid for a period of 92 months i.e. upto 2 months beyond the expiry of the Contract period of [90 months].”

Source: https://infracon.nic.in/WriteReadData/consultantprojectsAETWO/605_File3378349816.pdf

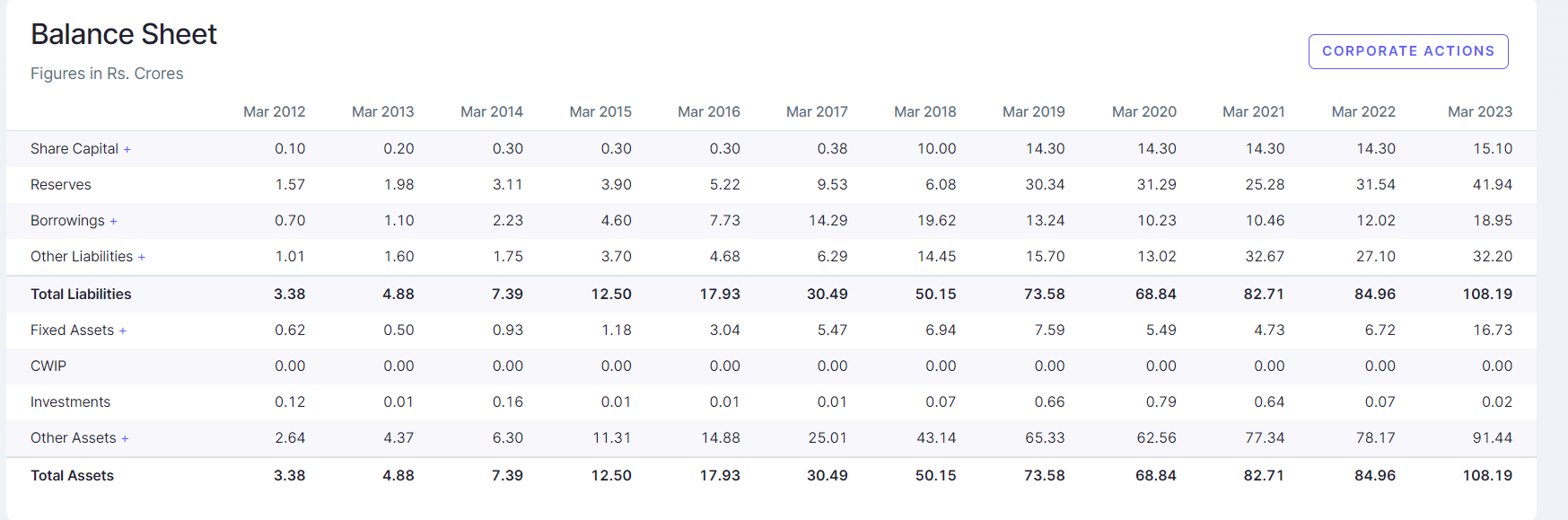

Financial snapshots from screener.in:

Short-term (1 to 3 years) growth trigger: Increased order flow is likely this year as India goes into election year.

Medium term (3 to 5 years) growth trigger: Company has started bidding for international projects which are of larger ticker size (20-25 crores vs. 7-10 crores in India). Margins of international contracts is higher than domestic contracts. Counterparties on international contracts are multilateral institutions like world bank, ADB etc. However, this shall start fructifying only from 12-18 months down the line.

Recent key development: Company has issued preferential allotement of shares to some non-promoters at 63 rs.

Sources: Company filings such as annual reports, conference call scripts and other announcements by the company on exchanges (mainly NSE).

Disclosure: I have initiated position in the stock just last week (between 28th August to 4th September). It accounts for less ~1% of my portfolio.

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example and learning purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation.