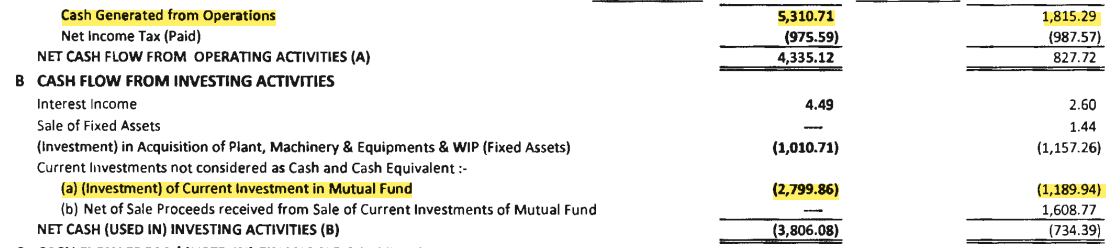

Apart from 100+ crore sitting in investments, I wonder if the reason the stock not getting enough traction is also because the company is not able to fully convert their profits into cash. as per the numbers on screener, the net profit for the last 6 years between FY 18 - fy 22 is 87 crores where as the cash from operations for the same period is only 48 crores.

What percentage of Natural gas usage in EU is for cooking? My guess is it would be single digit percentage. Vast majority would be home heating or energy generation.

Yes, Percentage wise, it seems like it is around 6% based on the link below.

However I am not sure if the percentage of gas would matter. Even if the usage is high or low the meter/regulator is required in a house, camper van, etc. Not sure if a single regulator/meter can be used for cooking and heating. Or if there’s different supply for for both heating and cooking.

However given the limited research i did it seems like it is being widely used.

In my view the poor performance in Q3FY23 is some what related to what is happening in Europe right now.

Energy crisis (high energy prices)

High inflation (moderation in demand)

For a company that manufactures for the European market these could be very bad times. My sense if Q3FY23 results and maybe few more quarters have to be looked at from that point of view.

I can see that the Fixed assets on the BS have doubled from 10 cr from March 2021 to 20 cr in Sep 2022 and hence Q3FY23 would have been a quarter with low utilisation levels and hence leading to negative operating leverage. Employee cost was somewhere in the range of 7-10% and that has increased to ~14% this quarter.

When you are investing in micro caps one should expect this sort of volatility in earnings. The stock has corrected almost 50% from 1600+ levels. We remain positive on the business and believe the situation should improve once Europe starts improving. Given that there is very little communication from the management side, we can only assume what might have happened.

Disc: Invested in client portfolio and hence biased; Not a recommendation; Please consult your advisor

Results published over the recent quarters were pretty much inline with volumes showing here… Q4 more likely will be see muted numbers which will drive out many weak hands who accumulated in the last 1 year. Sub 600 will be a good re-entry level.

Cannot give up based on a single quarter performance. Let’s see what the results are to say today. Price has held up reasonably well over last 3 months despite the worst quarterly performance in a long time.

Another bad quarter can get the hammer down hard on the stock with a possible 600 in reach. An average & above can get the price moving higher from here.

Not to forget the investments company is holding alone are worth 400/share. Entry at 600-700 will be a heavy bargain.

Results today are still far below the highs seen in 2021 & 2022. Topline still struggling to pick up is a major worry.

MTM gains of 12 cr takes the valuation of investments alone at 425/share. God knows how long the company will keep carrying this without any productive use to business or to shareholders.

With EPS in the range of 60, fair value should be at least above 1000. Will hope to see the price crossing this in next 3 months, provided the broader market continues to remain sideways if not growing.

Certainly, neither a time for fresh entry nor for a hasty exit. Patience will be the key for those continue holding.

MTM incremental gains for Q2 todate is 11 cr already translating to ~ 140 crores which is 55% of its current market cap and 81% of its equity. Company keeps throwing peanuts to its shareholders each year paying a paltry 1.2 Cr as dividend.

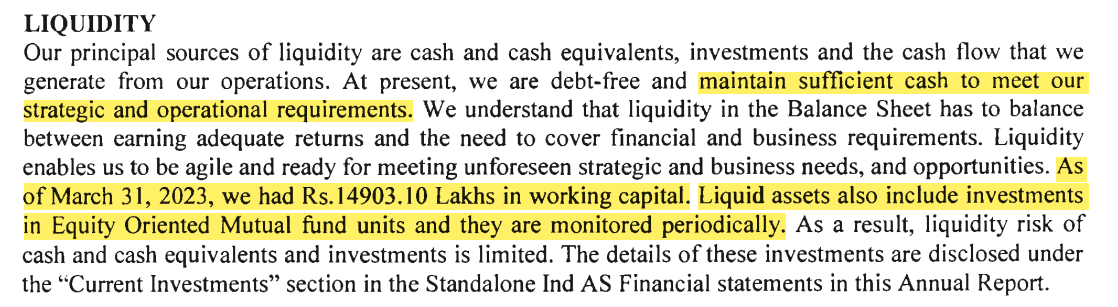

2023 Annual report is no different from its past, without explaining the rationale for exposing so much cash in the business entirely to market risks on which company’s management has no control.

Wonder what kind of strategic and operational requirements are prevailing over last 5 years that forces the company to lock 80% of its equity in mutual funds and not bothering to explain them beyond these few lines.

MDA segment of the annual report is another joke which no one in the company seems bothered to modify over last many years.

Hope the statutory auditors have exercised their full independence in verifying all stated investments and utilization of cash generated from operations, else the minority shareholders can write off their capital as a donation to company management.

No wonder the stock has consistently been derated despite such super strong balance sheet.

Discl: Still holding patiently a large chunk expecting more transparent communications from the company to its minority shareholders.