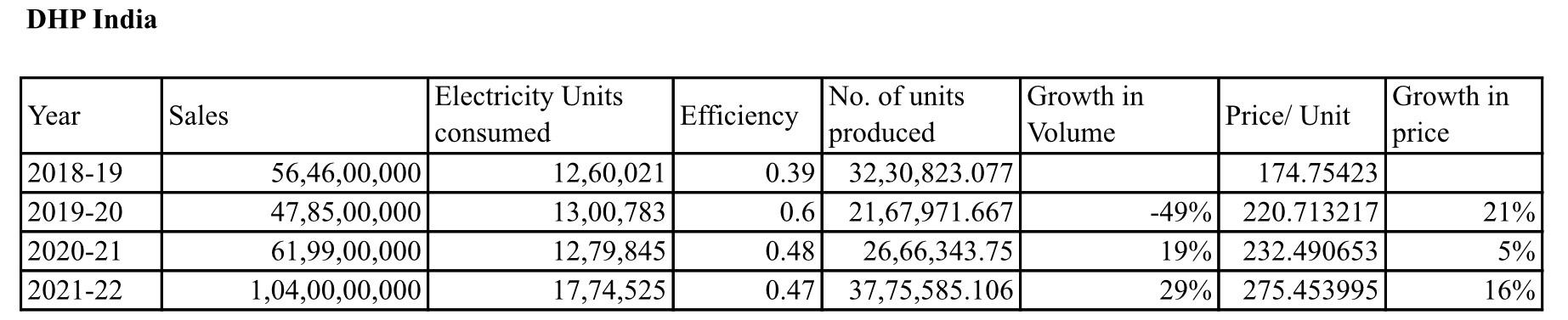

I was trying to find out the volume growth and realisation growth over the past years

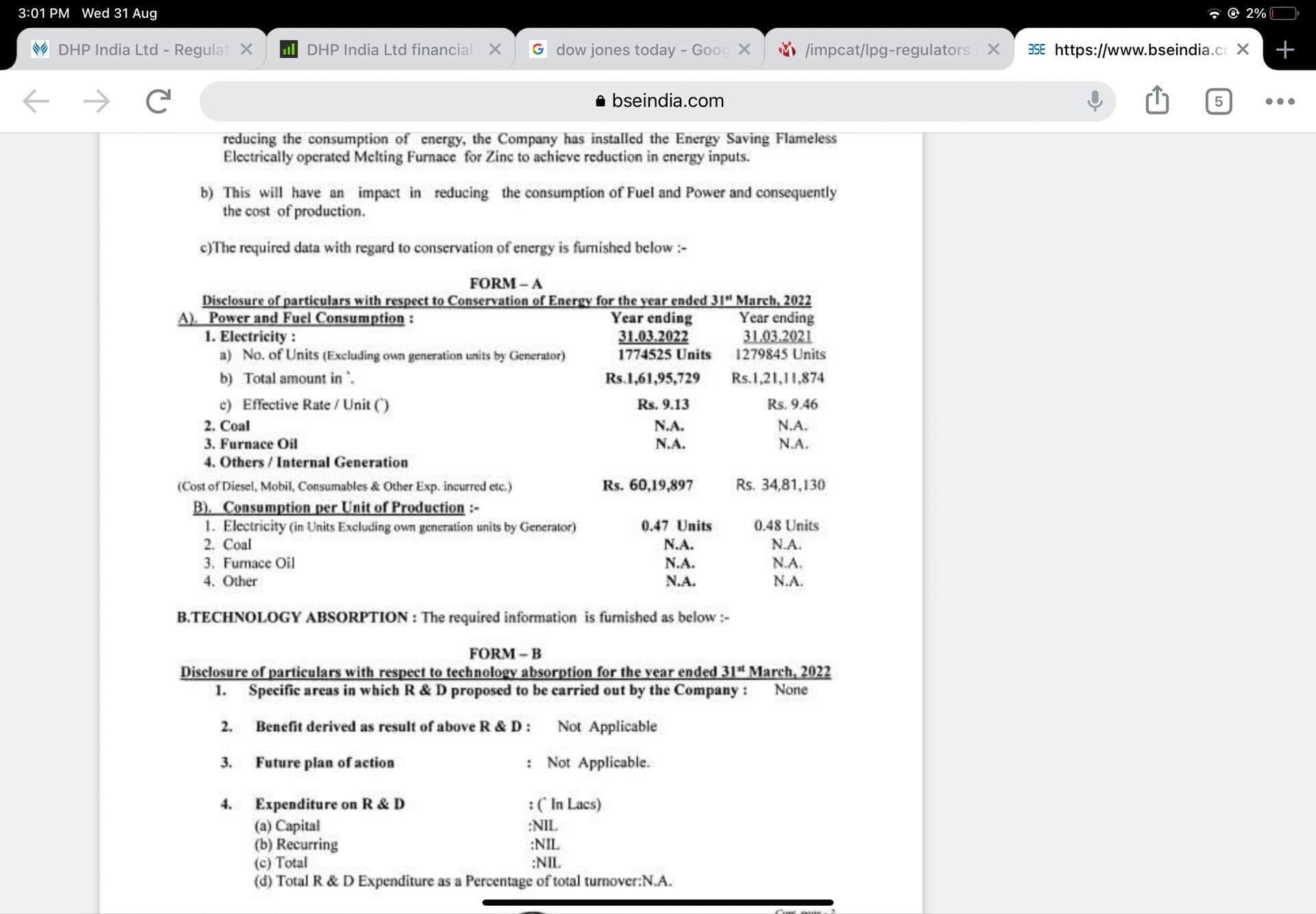

This might be wrong details of internal generation is missing

I used fuel and power consumption data mentioned in annual report.

I was trying to find out the volume growth and realisation growth over the past years

This might be wrong details of internal generation is missing

I used fuel and power consumption data mentioned in annual report.

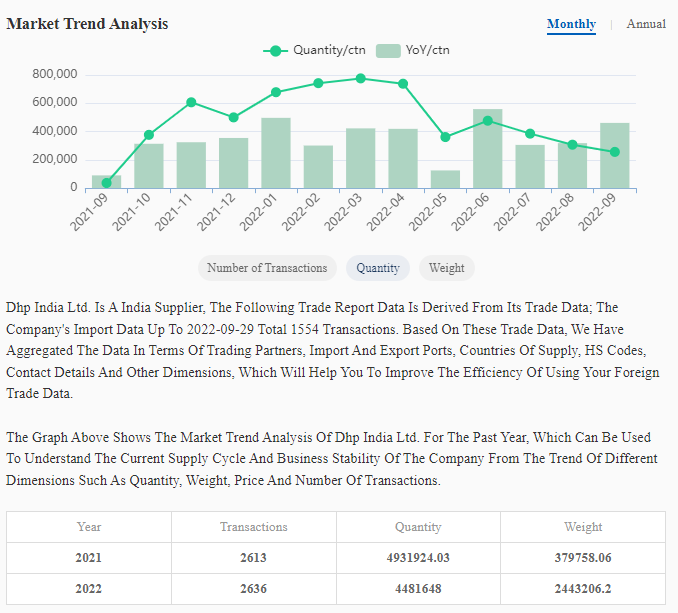

The realization per unit might not give a correct picture. Company has multiple products classified under these 2 HS codes. Just did a scuttlebutt from home depot & lowes where a propane automatic changeover regulator costs around ~$28 per unit.

Even from amazon fairview sells for $36

In the absence of any other data, not a bad way to deduce the average realized price, assuming uniform margin% across different product lines and uniform $ exchange rate.

Last FY has indeed created a new base with 25%+ volume growth as well as the company’s ability to pass on the raw material cost increase to its customers, which by itself will be another 25% addition to topline.

As some one pointed out earlier, fall in copper / brass prices instead of acting as a headwind for selling price and margins, will actually be a tailwind for a higher margins in % terms which when combined with volume growth can more than offset the impact of reduced selling price.

Agreed but we don’t have access to granular data.

Ultimate aim is to do correlation analysis of quarterly sales figures with gst data

SYSTEM ON INDIA's MONTHLY TRADE<br>(Harmonised Classification of Commodities).

Is anyone going to attend the agm.?

There are plenty of website which provide real time info about exports but one needs to be subscriber. I don’t have access.

Having seen the fundamentals play out for last 10 years, the price movements in the last few months is a compelling case to focus on technicals.

The energy crisis in Europe is forcing industries and individual to shift from piped Natural Gas from Russia to the much cheaper and cleaner fuel alternative - LPG. I think we might see highest sales from DHP in times to come. Views?

I’m yet to see evidence that this is going to be a fundamental change.

I really wish the company was open to more Shareholder Communication. They’d be best placed to confirm or deny such news.

I don’t really regret management’s inactions to reach out to their shareholders to update their business position in the backdrop of energy crisis in Europe. They have been doing their job thoroughly all these years in the best interest of their business and let the results do the talking.

Neither they have any control on the macro events nor on the speculative price actions in their stock.

For many long time shareholders who believed in the company, it’s time to rejoice the occasion on crossing 500cr mcap.

I don’t know if the current price action justifies the business outlook in the near term, but I will continue my journey as a shareholder albeit booking some profits on the way.

@Lakshmi_Narasimhan_B : I believe you had been invested with DHP for a very long term now. Just wanted to know, have you built your positions over a period of time (how long did you take if you did so) or you went for the full stake in a single purchase itself.

I think, you are still bullish on DHP, would you be looking to increase your stake over a period of time.

Disclaimer- Not Invested.

@WomenInvestor It took 5 years from 2006 to 2010 to build my position in this stock. With consistently growing free cash flows year on year in the business, never felt the need to exit. Regret selling though a major chunk in 2010 premature for a meager profit.

I still believe there is good potential for growth in the business and will continue following the results closely as done in the past.

I see point in what you said. also heard EU will import lot of LNG to compensate for loss of PNG from Russia, can products made by DHP usable with LNG? I think yes but need to confirm.

Invested

These LNG will be imported via ports using floating storage regasification unit (FSRU). Once regassification is done they will send the gas to the existing Natural gas pipeline. I really doubt this will require lots of valves aka demand for DHP

Discl: No holding and no transaction last 30 days

@rajanprabu Thanks for providing clarity.

Seeing the scale of LNG imports that Europe will be embracing to offset the shortage in natural gas, existing FSRU facilities may grossly be insufficient to handle the volume resulting in feeding to nearest onshore regassification facilities from ports. This still would result in transporting LNG to those plants and increase demand for company’s products.

However, LNG’s application being so wide and robust in other places in the world, there may be new opportunities for increased storage and distribution methods deployed in European countries which will open up more avenues company’s products.

Looking at consistent price action in the stock over last 3 months, it seems market is reading more than what we all understand out of the developments happening in LNG market.

Without any sort of communication from the company management, these speculative price actions are only going to get worse.

AGM Notes? Anyone attended?

Interesting leads available in the above link on monthly export shipments. Q2 volumes appears to be lower than Q1. Not sure if this data source is reliable. Comments from those familiar with this site will be useful.

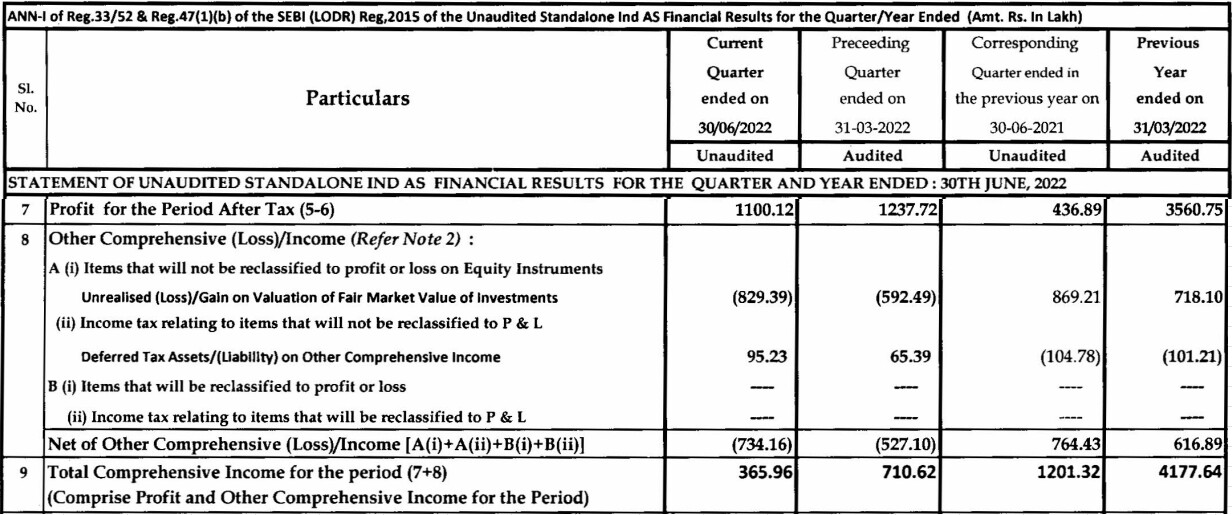

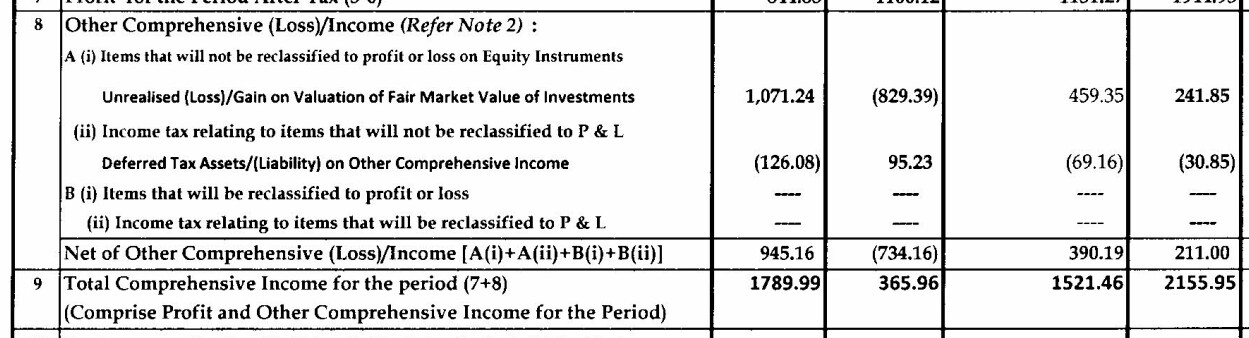

As against 8.29 Cr notional loss on MF booked in Q1’22, we can expect a MTM gain of ~ 11 Cr in Q2 going by 30th Sep valuation of MF assuming all units held as of Mar’22 are still intact.

MTM gains since Sep are on the rise with additional ~ 3 cr and a closing valuation of 93 cr (against 87 cr carried in Mar’22).

The company should have a policy to cap the upper limit they carry in MF (@ CMP) in relation with free reserves (ideally 50%) beyond which should be liquidated and held in FD/Govt Bonds or at best distributed as special dividend, if they cannot be productively deployed in the business.

A principal reason this stock is not getting the traction it needed despite spectacular track record is the lackluster use of cash in the business.

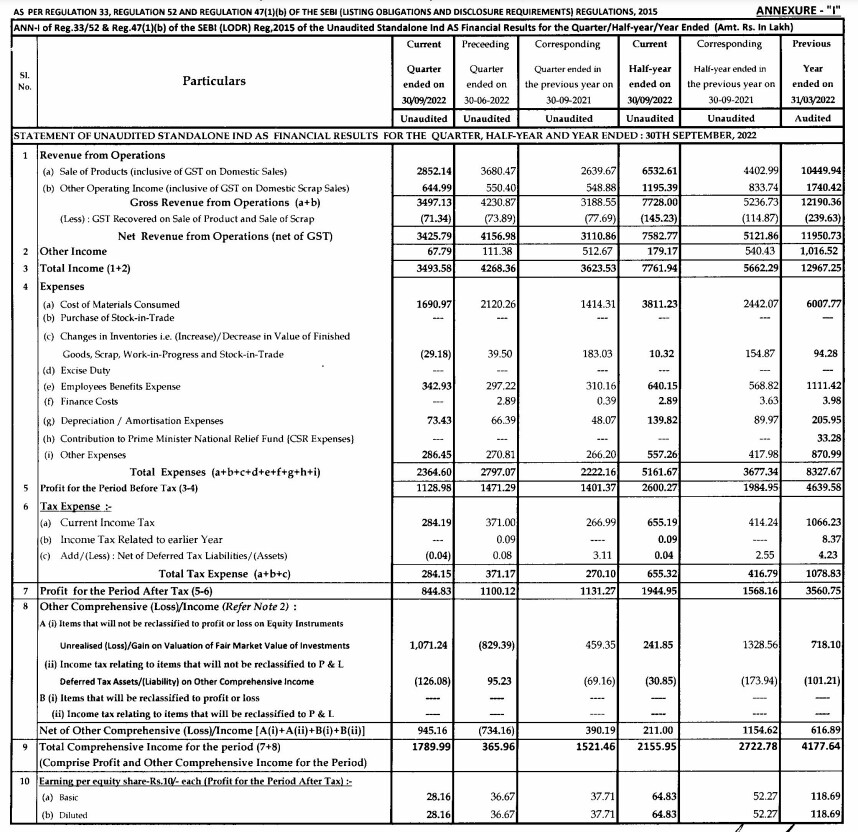

Results:

Sales are down from the quarter, though YoY is up. There seems to be no seasonality to this product and Mgmt is not sharing it’s views on the future.

Equity investments have done well.

Insights welcome.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/1b809599-f3bd-450b-a20e-9d284f53cbab.pdf

| DHP INDIA LTD | |||

|---|---|---|---|

| YOY | Sep-20 | Sep-21 | Sep-22 |

| Sales | 17.12 | 31.11 | 34.26 |

| Operating Profit | 0.66 | 9.36 | 11.34 |

| Net profit | 6.63 | 11.31 | 8.45 |

| OPM | 9% | 30% | 33% |

| Margin after Tax | 91% | 36% | 25% |

| YOY | Sep-21 | Sep-22 |

|---|---|---|

| Sales | 82% | 10% |

| Operating Profit | 1318% | 21% |

| Net profit | 71% | -25% |

| OPM | 234% | 10% |

| QonQ | Jun-22 | Sep-22 | QoQ |

|---|---|---|---|

| Sales | 41.57 | 34.26 | -18% |

| Operating Profit | 14.30 | 11.34 | -21% |

| Net profit | 11.00 | 8.45 | -23% |

| OPM | 34% | 33% | -4% |

| Margin after Tax | 26% | 25% | -7% |

However QoQ has been neutral but I am still happy to see OPM around 30s, I think more important for me in this business will be to keep close watch on OPM if they are able to maintain it. If it sustains business will thrive itself.

Disc: Invested and biased

With 30% operating margins and 106Cr out of 160 Cr free reserves sitting in liquid investments, I have not come across companies under 500 cr market cap matching its strength.

Today’s 17% drop with 22K shares however is a shakeup test to drive away weaker hands holding the stock.

It may not be of surprise if this flush-out continues all the way to 750-800 and leaving the onus on Q3 results for a meaningful reversal.

Without any guidance coming from management or investor friendly actions, price will be left in the hands of market that has no tolerance for slack in performance or patience for a turnaround.