This company seems to be trading in multiple commodities and owns a couple of windmills as well. However, these parts of the business seem completely inconsequential from the perspective of valuation.

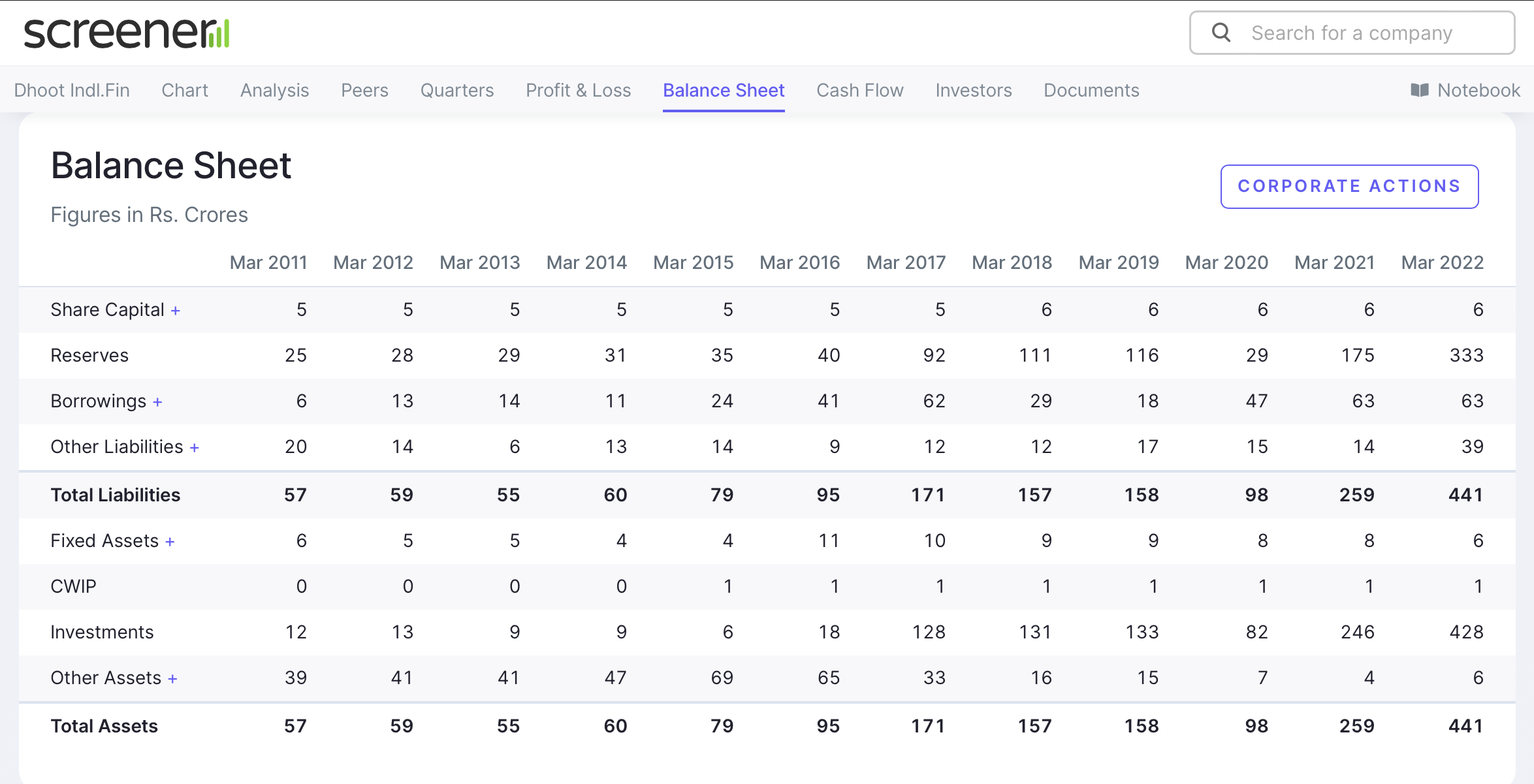

The main value lies in balance sheet i.e. Investment at 428 Cr. The investments are mainly quoted equity shares in various public limited companies. Illustrative list from screener: Register - Screener

The rest of the balance sheet is at around 13 Cr. They have non-equity liabilities of around 100 Cr.

With a very liquid book of around INR 300 Cr, and a market cap of INR 50 Cr - this looks like a very good buy.

Red flags:

- No buyback, increase in shareholding, or dividend from the promoter. Why would they not do any of these? rather, Rohit Rajgopal Dhoot only takes a salary of INR 24L. If I can’t see how the promoter gains value from the company, I get suspicious that they may gain from a source I don’t like.

- Rohit Rajgopal is a director is many companies. While this is not a bad thing per se, but married with point number 1, I get more suspicious. Link: Rohit Rajgopal Dhoot - Director information and companies associated with | Zauba Corp

- They seem to be running a portfolio on borrowed money. Market drawdowns could lead to margin calls.

Final thoughts: The discount is too alluring to ignore. Never trade on margin, but there is a significant discount. Even if they market falls 50%, they are above market cap.

1 Like

There are many Holding company stocks in the market trading at 80-60% discount to market value of respectable companies stocks like Maharashtra Scooters (Bajaj Auto, Bajaj Finance/Finserv), Kama Holdings (SRF), Tata Investment Corporation (Many Tata companies) etc.

If you’re looking to play holding discount atleast these names would provide necessary Corporate governance and Shareholder friendly outcome which isn’t the case in this company (Dhoot).

Though you might want to read more about these holding companies threads to find why they trade so cheap.

Would Dhoot be considered a holding company? I have been tracking holding companies, and feel I understand the logic for the discount to a certain extent. I may not agree with it, but bhav bhagwan che.

As opposed to holding companies, Dhoot is not a promoter at its investees apart from Oudh Sugar (I may have missed a couple more). It is a public market investor like many of us. The fact that they book profit and get out of companies and trade actively gives their portfolio liquidity. On the other hand, a holding company would have most of its portfolio illiquid and act as promoter.

1 Like

I agree with the logic but as I can see the company has paid 0 dividends in the last 10 years nor any buyback nor any communication with shareholders beyond mandatory annual report which is also bland, no outlook or guidance.

Comparing this to Berkshire Hathaway if you allow, it also functions the same, invests money into stocks and sometimes acquires business but it pays the investors back through buybacks and gives out Annual reports which are quite detailed in nature so that shareholder are informed.

We can be a shareholder in this company and enjoy company’s gains however would we ever see the light of the money in our hands is a question.

If they start to perform buybacks/dividends then it could be considered. Please reach to IR if they can provide some info on that.

2 Likes

Completely agree on the red flags. I assume that the market is right, so just want to figure out what I am not seeing. Although the red flags exist, I have yet not seem obscene erosion of value through RPTs or loans.

I tried calling the company, no response. Will try again on Monday.

1 Like

New Red Flag: They have shifted auditors from Bohra & Co. to Pulindra Patel & Co.