You are right about the headwind in pharma in general. But, don’t you think some of the pharma scrips are unreasonably low priced despite having a decent earnings outlook for the next couple of years (for example, Auro and Lupin). Does this mean market is correcting their PE ratio? Would you still call it a contrarian bet if one chooses?

@hitesh2710 Thank you Hitesh for taking a look at my Portfolio. I am really thankful to all the VP seniors who are helping newbies like me.

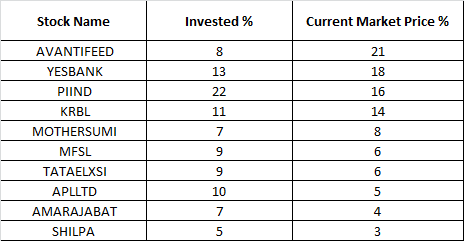

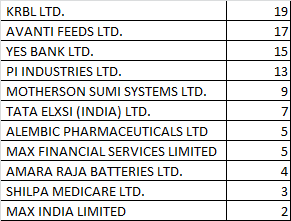

I usually look at the invested % and hence the allocation to pharma looks more. Here is how the portfolio looks with the current market price.

I have been actively building cash for a year and buying DEBT funds. I usually deploy it once or twice a year. Probably I will deploy it sometime when I find an opportunity.

This is how my investing strategy has evolved so far. I would kindly request the board members to help me refine it.

Identify companies with good track record. (i.e,) 3 Year Sales growth, Profit growth, ROE, ROCE, FCF etc

Good Management. (Promoter Holding, Equity Dilution, Wealth Creation, R&D Expenditure, Any fraud history etc)

P/E - This is the single metric i use to find the valuation. I will see anything less than 15 PE as reasonable price and will not invest grater than 25 PE. I know this is a big drawback but I am living with it. I will surely miss companies that revive (due to high PE) but I am OK with that.

I will also look at NIFTY PE. I usually will be 40:60 on equity/debt if the NIFTY PE is around 20 to 25. I will increase equity allocation when NIFTY PE falls below 20 PE. Again this another drawback, for the last 10 month I could not invest much into equities. I know looking at stock specific stories is the right way but I am not yet matured to do it that way.

I am inclined towards companies that produce products that are easier to recognize. i.e, KRBL, Eicher, etc.

I would again kindly request the seniors to help me refine it. It has been a wonderful journey with value picker so far. I have started documented my portfolio since beginning in this thread. Thanks again for all your mentoring.

Sold 15% of my total stock holdings today. Since I am not really good at valuation, i have sold 15% of all the stocks I own. If some one has a better strategy, kindly enlighten me.

I don’t think having 15% cash and remaining 85% in equity would give adequate protection if bear market indeed comes. My thinking on this matter is as follow:

I tend to classify long term equity investors based on their life circumstances.

Young, starting out, not much of the liabilities & investing for real long term wealth creation - This class of investors should stay invested in high quality, growth companies and not bother about valuations. If bear market comes, they should consider that as blessing and load up further on the stocks.

Middle aged or old, may be uncertain about job stability, capital protection is important but at the same time does not want to stay out of wealth creating opportunity in stock market - This class of investors should follow approach of balanced fund, means cash level of 35% to 40% and balance in high quality growth stocks. Ideally high cash levels should be result of selling under-performers. Portfolio tend to be concentrated and as long as growth profile of stock portfolio remains intact, overall portfolio achieves reasonable balance of growth & capital protection. This is also in line with what Ben Graham advised in his book Intelligent Investor - maintain minimum 25% & maximum 75% equity exposure depending on comfort level with valuations.

Investors with trucks full of money, not dependent on job or capital gains for living expenses & for financial responsibilities, may have other assets which provides adequate cash flow or may be, dividends from stock portfolio are much more than adequate to cover their expenses - This class of investors also should not bother about valuations or bear market and should remain fully invested in equity.

So, I guess it would be better to tailor equity exposure based on risk profile. For sake of disclosure, I am class-2 type of investor and maintaining high level of cash, about 40%, as of now.

Thank you very much for taking time to reply and provide your valuable suggestion. I completely agree with you.

This thread is more like a log to my journey. I am still learning in the market and i would categorize myself as a defensive investor as in the book Intelligent Investor. I always go by the 40:60 equity debt portfolio. I take NIFTY PE as reference. I was around 41:59 before trimming my positions today. After trimming it is around 35% equity and 65% Debt(FD + Debt funds). The debt is storing money and whenever i find valuation to be reasonable (read as pe less than 20 or any stock specific story with mouth watering valuation) I will build my position.

I mean i am sitting really on cash and I would fall under no.1 in your category. I am 28 and want to build long term wealth. But, I lack the experience and skill to remain fully invested in this market.

I am holding century ply from 2015 and thinking of dumping everything very soon.

My reasons.

1.) Havent seen much of an outbreak since 2015 and its always been a slow performer.

2.) Current real estate market isn’t look very bright and i’m really thinking that they will have a muted year .

3.) environmental laws are also getting stricter.

4.) This looks like an industry wide issue because i looked at greenply as well and even they are almost having same kind of financials QoQ.

@shampavman Around 2015-16 management did say that the growth will be muted. if you look at 2015 the net profit more than doubled compared to 2014. Price followed the earnings and the market priced the stock accordingly. So the base was really high and double digit growth from here is difficult and it may take some more time. Nevertheless, it is a good company and yes it has environmental laws to its advantage.

I learned this lesson hard way after investing in Alebmic pharma. I invested after a block buster extraordinary year. PE looked amazingly cheap. It did came up with good results, but compared to the block buster earnings it had it was not enthusiastic which reflected in price as well.

Looking for avenues of growth is an important aspect that I missed. Hope it helps.

Sold 25% of my portfolio today. Sold 50% in Avanti and 25% in Yes & KRBL. This is how the portfolio looks now. Equity part has gone to the lower limits around 25% and the debt is around 75%. I will wait till i find reasonable valuations in any of the existing companies that I hold or any new interesting ideas that come up.

Pulled out 15% of money from equity today. Equal cut across all scripts. NIFTY PE around 28 which is equal to the peak of 2008. But market may stay here for longer time than expected owing to liquidity factors. Waiting with good amount of Cash for now.

Another 10% cut across all the companies in the portfolio. As they say “There is no top for the bull market and no bottom for the Bears”. Almost all the decent companies look overstretched in Valuation. Garware wall ropes looks interesting. I will take a position if there is any decent correction.

Hi @Dhinakaran, Can you help me out with the following queries

In your earlier post you had mentioned that you have invested in debt funds, any funds with a good track record, at this point in time with market at record high moving towards debt makes sense to me.

When a stock is bought let say at 10 and reaches 18, how do you make up your mind to sell say 10% or 15% of your holding. Is it with the believe that the price of 18 would come back closer to 10, I struggle to sell some stocks that have gone up say 40-50% from my buying price and what stops me is - ‘What if the price doesnt come close to my buying price’

Seasoned members can also help me with the answers alongside with Dhina.

Debt funds are quite easier to choose. I will go with Gilt funds mostly to avoid the risk of debt default. Also there wont be much difference among the top houses. It is a good idea to choose direct funds. Also, if you choose to invest in non gilt funds make sure they are well diversified and make sure to check the fundamentals of the individual companies in the debt fund portfolio.

Selling is quit difficult even for the esteemed members. For e.g, Avanti gave me 5X returns. And then I sold it to make sure it did not cross 20% of the total portfolio. I usually go with NIFTY PE to find if the market is overbought or not. Also I don’t completely exit from any of the company company owing to higher valuation. Whenever the NIFTY PE crosses 25+ i do sell part of my portfolio and it will be a cut across all the scripts. I know this is not the best method but it works for me.

@Alphin All these companies have been analyzed so much in Valuepickr and other forums. My holding period is around 3 to 5 years and I prefer mid caps. My aim is to do a CAGR of 20% annually. I have a debt portfolio where I rejig between based on the valuation. Currently debt is around 70% and equity is around 30%.

If you feel something needs to be answered, please let me know. I will give a try. Thanks for taking time to review my portfolio.