Any reasons to choose century ply over Greenply - valuations and other business parameters of Greenply seems to be better off

@varvp14 Varun, Could you please list the business parameters that you are talking about ?

I was referring to parameters like long term consistent growth and wealth creation, stable ROE, consistent reduction in debt, state of the art facilities and being market leader, their products are way better - this I can vouch for as I am an Architect and we generally ask clients to go for greenply and greenlam products. The expansion plans are well thought off and are not adhoc - earlier issue was debt which has come down. May be I am missing something - that’s why I was asking you

1 Like

@varvp14 Varun, I started investing into equities entirely from borrowed conviction. At a point I was holding 50+ stocks. Then I came to know of value picker and I was able to reduce to 15+. Century ply was recommended by Sharekhan I think. I didn’t even know that they are into ply board when I bought this. But in the due course I did a basic analysis on my portfolio and I did compare them with peers. I compared Century ply with Greenply in screener. Compounded sales/Profit, ROE was better and consistent in century ply as per screener.

Apart from that, I was very much impressed by their website and their brand building activity. I sometime back traveled to a remote village deep inside TN, where I could see sharon ply woods ad. Apart from that I do see ads being displayed in and around Chennai. So I preferred to stick to century ply.

Century ply could benefit when economy picks up and schemes like housing for all being concentrated on rural areas.

I could be completly wrong and I would love to hear from seasoned investor like you

Dear Dhina

I may be bit offshoot to your approach, portfolio concentration (number of stocks within a portfolio) unfortunately isn’t a straight forward answer for any one. I can share what I am doing all these days:

First all your purchase should be within your circle of competence, how do I know circle of competence…need bit of exercise if you havent done it. I was just trying to explain in another thread.

A portfolio concentration to me depends on six factors for my risk appetite:

- Competitive Advantage of a Company

- Quality of Management

- Risk Management (financial, operational, compliance and strategy)

- Future catalysts for business

- Margin of safety (I use mostly EPV, Asset reproduction, Franchise, base case, EPS growth…some relative valuations like PBV, PSR, PE just to see the price behavior against fundamental growth)

- Special situation (spin off, distressed asset, hidden asset and so on)

My first band of stock is restricted to 5 stocks constitutes 70% of portfolio. They excel on all criteria to my assessment on above six.

However concentrated portfolio requires a lot of documentation, analytics,…I m sure you are doing them.

Happy investing ![]()

1 Like

To be honest I haven’t really compared both of them on every parameter. Just by the quality of the product and being market leader with good financials was enough for me. However let me get back to you on this after proper study.

i also think that green ply is better long term horse. purely bcos their expansion into MDF. coming from a furniture manufacturing line, i think MDF is the way forward and greenply is right betting on this.

Disc. NOT INVESTED but on my radar

some negatives.

Net profit seems to be consistently low

sundir valai holding creating a bias

high branding and consistent marketing required. (awareness vis a vis like Pidilite/Astral

need to create lower level distribution network

PE 15 seems high for manufacturing

GST will not make any difference rather need tax breaks

1 Like

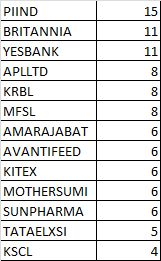

This is my current portfolio. It has not changed much. Came out of century ply, Paushak, Eicher and bought more PI Ind, KRBL and Avanti few months back.

1 Like

Hi Dhina,

Any reasons for coming out of Century Ply? If I understand in the long run the GST bill could provide a huge benefit to the organized players. And Century and Green Ply should be the major beneficiaries of it and with around 60% of it being unorganized, the potential appears huge. I am still trying to understand in depth the GST bill and how this impacts the various sectors.

Hi Samir, I have very limited experience and my views could be completely wrong. Due to sluggish real estate sector, it would be difficult for CENTURY PLY to achieve double digit growth in the near term. Also the stock moved up due to the passage of GST. It will take at least 1-2 years to see the GST impact. Kindly let me know your thoughts.

This may provide some info for folks tracking Century.

http://www.thehindubusinessline.com/companies/century-plyboards-to-focus-on-expanding-india-operations-await-gst-rollout/article9032485.ece

I am not invested. But tracking for an opportunity to enter some of the organized sectors if at all there arises an opportunity. The recent run doesn’t provide any valuation comfort.

2 Likes

I have sold 10% of shares of all the the companies that I hold.NIFTY PE has hit 24+ toady and the idea is to be ready with the cash when the market presents with any new opportunities in the near term.

1 Like

From where u calculated Nifty PE…Is it standalone or consolidated?

I used NSE website to get the PE.

Was listening to one of senior fund managers from motilal oswal . As per him current NIFTY PE was 18 though I m not sure he meant forward or backward.24 seems too high. I think capital mind keeps on updating nifty pi

Hello All,

I have done my first ever analysis of a company. Below is myanalysis on KRBL. Seniors kindly review and help me on the areas where I can improve. Also kindly let me know if I have missed anything important. I have purposefully excluded the basic numbers like 3 year sales growth, profit growth, ROE etc since it is readily available in screener. Appreciate your help.

KRBL

About the Company:

The company is in the business of selling rice in domestic as wells as in foreign markets. The company is also in the power business. KRBL is known for its flagship brand “India Gate”.

Management:

The company is managed by good people and the management walks the talk. For e.g., In 2011 the company said that it will Ramp up its contact farming programme to cover over 2,50,000 acres by the end of FY12. Also it guided double digit growth in export business in the next year. Both of this was executed as planned. In 2012 the company said that it will expand its installed capacity by 4-5 MW every year for the next three to four years. It did expand in the power business and the revenue from power business is growing at 30% CAGR though it contributes only 3% to the total revenue. In 2013 the company said it is planning to launch brown rice variety and it did launch India Gate brown rice as planned. The company is expecting the volume growth to be at CAGR of 12%.

Rice Business:

The company is mainly involved in selling of Basmati rice. Though rice is a commodity, the company says that India gate is enjoying a premium of 20% over its competitors owing to the superior quality. The company sells non-basmati, normal rice as well but India gate contributes to the most of its revenue stream. The company is also diving in to new markets and launches new varieties. The company has tie ups with research institutes to develop new & better variants of seeds which requires less water and resistant to disease. In 2011, R&D expense was 220 lacs and in 2016 it has increased to 369 lacs. Management also bought back its shares during 2013&2014 and the current promoter holding stands at a healthy rate 0f 58%. The debt to equity is also being reduced. The company also reduced the inventory days due to better inventory management.

Power Business:

The company is also involved in selling green power. It started when the company used its rice bran to generate green power. The company sold its excess power and now the power business it is contributing to its cash flow. The power business now includes Solar, Biomass and Wind power. The revenue from power business has grown at 30% CAGR and it contributes around 3% of the total revenue.

Moating points:

Basmati rice can be grown only in certain parts of India and Pakistan.

Company’s flag ship brand India gate is widely recognized as one of the best brand in India as well as in foreign markets.

Risks:

- Middle East is one of the major importers and any political turmoil will significantly affect the earnings.

- Iran accounted for nearly 38% of India’s Basmati Rice exports in FY 2013-14. Any ban in Iran will impact the earnings considerably.

- The company is heavily dependent of Monsoon, Price of paddy, crop diseases.

- Import ban on genetically modified varieties.

- Risk from big companies like HUL, ITC though the company says it has close relation with the farmers along with contract farming.

- High working capital

- Government intervention in fixing price (though basmati price would not get affected).

Investment Thesis:

Basmati currently accounts for only 1% of the total global consumption of rice. With increasing disposable income in India and new malls, going forward the company should be able to achieve 12 – 15% growth. The company also has few tailwinds such as Good monsoon prediction, more spending on agriculture by the Indian Government, increasing population in India, rising middle class, moving towards branded products. With this the company can provide stable returns over long term with moderate growth of 12%.

1 Like

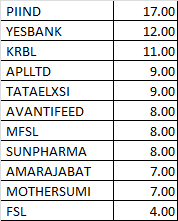

This is how the latest portfolio looks like. No major change in the portfolio. Sold Kaveri seeds and entered into FSL. Equity Vs Debt stands at 45:55. Views on portfolio is welcome.

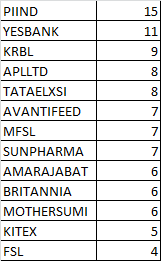

This is how the latest portfolio looks like. Came out of Kitex. Other than that no major changes. Suggestions welcome.

I find that you have 17% allocation to pharma including sun pharma and alembic. While allocation may be low I think pharma might have seen its best times at least in the short to medium term.

Reasons being cut throat competition in US markets which tend to erode prices early on in the launch of a molecule (unless the molecule is very niche and has very few competitors). Domestic scene is also riddled with issues of generic prescriptions etc.

A contrarian might consider these to be good indications to go long citing that when everything looks gloomy its time to buy. But I personally think it might be a long time before pharma makes a comeback.

5 Likes