DHFL’s Asset-Liability Mismatch is positive upto 3 years Even at 11%, I’d say DHFL can keep going upto a year or so (While taking strain on their B/S, sure). Of course, this is assuming that interest rates don’t go haywire. If interest rates do climb to crazy levels, then DHFL posting losses would be the least of our worries. The entire credit environment could go for a toss, affecting all BFSI firms left, right and center.

Once again, the way I see it is that the business is extremely undervalued. Ignoring DHFL’s core business for a second, here is how their liquid cash and investments round up:

That is a total of Rs. 7745 Cr. in Non-Operating Assets and Cash. That in itself is Rs. 247 per Share. Even striking off a few points from that for liquidity, we’d reach the current price of Rs. 220. Also consider the fact that I’m ignoring their investments in JVs and Associates (Like DHFL Pramerica, Aadhar HF and so on).

Essentially, the market is pricing the stock as if DHFL’s Housing Finance business is going to wind up tomorrow. In my opinion, you only have to take a call on if this sounds plausible or not. Here, you should also consider the fact that DHFL has been in this business for 35 years, facing several short term and long term credit cycles. They know what they’re doing.

I am sure that market knows more about quality of book for HFC lenders than retail investors are privy to.

A few HFCs have fallen prey to unscrupulous builders, who introduce ‘dummy borrowers’ (for a fat commission) as prospective customers. The builder gets bulk low interest funds (at retail rates) from the lender. The builder then tries to find a genuine buyer to sell down the apartment at matching or higher prices. Only if he succeeds, does he repay the HFC

ET article is staying this as fact and not a quote attributed to a person.

In a liquid market what you say must hold true. But with Net current assets of -10000 crore and a trust deficit in the market where it is a question mark as to whether institutions/retail investors will actually subscribe to CP’s of the company and where their bonds are already quoting at 11% (in which liquidity has already seemed to dry up), how does DHFL cover this asset liability mismatch? Further, they already seem to be leveraged to the hilt (gearing > 10). Btw, even a company like gruh has an A/L mismatch but people are lining up to subscribe. Their (DHFL) CL is 27k crores which basically means that if they stop disbursing they have a quarters worth of cash and investments. If they stop disbursing which someone on this thread mentioned earlier, their balance sheet keeps shrinking and costs keep going up. I dont think the market is pricing for DHFL to wind up. 15% ROE at P/b of 1 would be fair value. I might be completely off but Im guessing it wont be easy to maintain that in the coming time for DHFL.

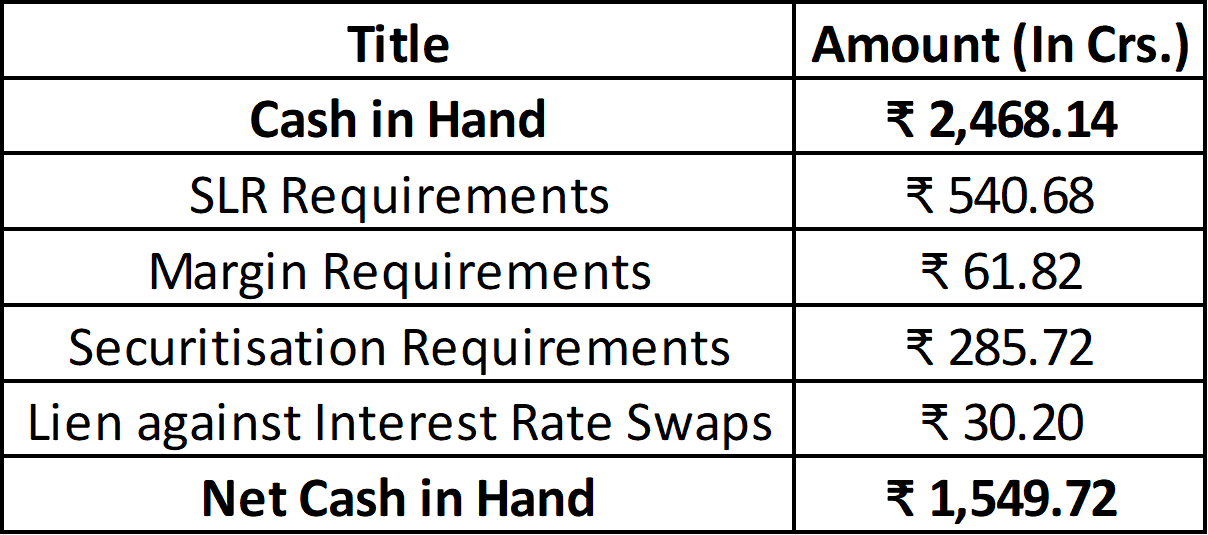

DHFL has a Short Term Borrowings and Loans of ₹27,188 Cr. It has Current Assets worth ₹18,138 Cr. It also has Short Term Lendings of ₹9,503 Cr. That’s a very tiny deficit in the Short Term.

As I said, DHFL is ALM positive upto 3 years. What you’re saying is possible if something like a Bank Run happens where nobody is interested in buying anything issued by DHFL. Whether that situation actually will happen, is anybody’s guess. You can’t reason with the markets especially amidst a panic.

That’s why the BFSI business is tricky. It’s a business that’s highly linked to the economy. So both the positive and negative sentiments on the economy have a magnified impact on the sector.

I just looked at the current assets vs liabilities figures which matches exactly with what you are saying giving us A/L mismatch of -9000 (current liability - current asset). When I had seen the B/S I could not find the 9503 short term loans and advances. May I humbly ask you to point me towards it? Isnt short term lendings part of current assets?

Mindless panic on Dewan and other NBFCs continues. Panicky TV anchors and journalists who have just discovered a new word- asset liability mismatch and the IT herd/part time investors on this forum who have suddenly morphed into financial market experts seem to be key contributors.

As an ex- financial markets banker, allow me to point out a few basics:

• First , ask yourself , how an obscure govt controlled infra lending company has suddenly become a proxy for the NBFC space? Most Infra companies have already defaulted on their bank debts, this one was stupid enough to fund highly uncertain infra related payments through the short term CP market and ended up in default. Is this even surprising? The issue here lies on their asset side not on their liabilities. Instead of the CP market they might as well have borrowed from a bank, through public deposits or from their uncle, it would not have mattered. They faced the equivalent of HFCs not receiving timely mortgage payments.

• Credit markets are inherently extremely panicky and even more so in the case of India- a country with a shallow and underdeveloped credit market. They also have very short memories. Argentina a country in dire straits today and one that has defaulted throughout history was able to raise a 100 year bond last year, Russia a pariah in 1998 after defaulting on both its FX and Ruble bonds was welcomed again to the capital markets within a year. Portuguese bonds spiked to 15% in late 2011 at the peak of the Euro crisis before rallying to 5% within 2 years and so on. Buy value, sell hysteria always works in the bond markets.

• There is no comparison between NBFCs like Dewan and Lehman. Lehman crisis happened because the assets the company was holding was mostly MBS which were almost worthless, more over they had plenty of CDO squared and cubed assets whose contents were unknown. Unless someone comes out and says that the assets on the books of bajaj finance, gruh, dewan etc are worthless there will be no credit cut off just temporary panic.

• The NBFC model of borrowing from capital markets and banks and lending onward is a viable one as long as the lending is prudent. The NBFC managers may have been overly confident of rolling over their CPs at good rates and hence some like PNB Housing may have gone overboard with high CP usage, but this is a minor problem that can be fixed, the overall sector will become more stable as the funding sources get aligned. This is what happened in the REIT market in Singapore post 2009 crises.

• Finally, please stop posting all the flawed ALM analysis. This is not how Financial institutions operate at all. The LCR or liquidity coverage ratio is the key metric calculated daily by CFOs. I don’t have time to explain here how that works. Suffice to say, stop worrying about it.

My doubt may be too naive, because I don’t know much about how NBFCs work. Is CP the only way of funding? Isn’t there a chance of getting funded by raising from ECB (like PNB housing did) or masala bonds or more from the banks? Given that they have been in this business for 35-40 years, have got some reputation and hence won’t they may be able to replace one form of funding with other, may be at a slightly higher cost.?

Well is it worth investing right now is all together a different question.

But I think the things to look out are

How much will this short term mismatch dent their profits?

Will this result in reducing the new loans extended and hence much the growth will suffer ?

Along with that how much net interest margins might reduce. (depending how well they can pass on or not the increased borrowing costs)

Also when the interest rates increase,will that result in higher NPAs? And how clean are their NPAs as of today?

disc: picked only a few shares for tracking purposes

This has nothing to do, even with short term investors. Someone made a huge, bad trade and there’s a dispute on whether he was authorised to do it. That’s SEBI’s territory and has literally nothing to do with DHFL’s business.

Any idea if the loan book of DHFL are cooked in any way, that is whether they have not maintained LTV properly, given subprime loans, facing cashlow issues? Price action is leading towards a negative surprise.

DHFL has an impression of collecting outstandings from the builder community by hook or crook. Not that builder community is any clean bunch of folks. No excel sheet or research report will ever tell you these things. Neither I have proof but you can talk to small time builders in Mumbai for the same. Not bad for the shareholders as such but fund mgmt community doesn’t think highly of these practices.

There are different ways to handle large NPAs (corporate or real estate) in lending institutions. e.g. Piramal can take over projects while Edelweiss will hand it over to their ARC division to take care. Both of these promoters have applied long term thinking in organizing their lending biz. Not many organisations have internal capabilities or second layer of risk mitigation to handle NPAs while DHFL has its own way.

absolutely concur with Sumit.

While the 'quality" of loans may be questionable, therr is no question weather they will be returned or not… this is because - first, the masses to whom they lend are normally middle class to lower middle class who would loose their sleep at night if they default on a repayment, forget about willful default.

second, they still have a house as mortgage.

again, the masses whom dhfl lends cant afford to let go their houses.

plus, dhfl has its own ‘hook or crook’ method…

We don’t know at what price RJ has purchased the shares.

RJ’s recent inclusion JP Associate was down by around 50% from his purchase price.

Axis Mutual Fund, IDFC Mutual Fund and JM Mutual Fund were seen trimming their stakes in the company in September.

Brokerage Emkay Global in a recent note suggested that 12 per cent of DHFL liabilities (nearly 17 per cent of market borrowings) were maturing in three months against 9 per cent of its total assets (nearly 3 per cent advances).

Big investors like RJ or BM are nimble and fast on their feet …they get in and get out very fast… since reporting happens on quarterly basis, rest of the world comes to know very late. He may have been out of it by this time and we will find that out only in January… This could be trading bet for him if he got it very cheap… so I don’t give much importance to these news . Everybody knew about BM’s position in PNB Housing but nobody knew when he got out

I notice that a lot of senior boarders as well as astute investors on this forum (as well as outside - RJ being one of them) are taking this drop as an opportunity to add DHFL to their portfolio.

If we keep this temporary cash flow mismatch/liquidity freeze in debt market aside, it would be helpful to understand the conviction behind the decision to add.

My understanding/thinking was that, before this fiasco DHFL was comfortably and consistently growing at 15% ROE. As Munger says, long term ROE = long term growth rate of the company. Taking that into account and the fact that opportunity cost of equity is approx 15%, shouldnt fair value of the company be 1 P/B? DHFL currently trades at very close to that which means that the company will continue to have to generate 15% ROE to justify investment. Some members have mentioned that (only speculation and hearsay on the street - might be inaccurate information) DHFL has cut down on further lending and that yields for them have gone up (its arguable that how long this situation will last). If that is true their book is shrinking (fixed costs spread over lower volume) and at the same time their input costs are going up. Shouldnt that make it a lot harder for them to generate that same 15% ROE that they were generating a few months back, now? If that is the case, shouldnt it have to correct more for it to become attractive?

What is it that I am missing in my argument? It would be nice to have views @dineshssairam and @ricky76 apart from other senior and experienced boarders with strong conviction.

I have already expressed my conviction in my blog and even in this thread. DHFL’s inherent cheapness is what makes it most attractive. I initially wanted to buy into the NBFC space with a diverse set of bets, but DHFL was the only undervalued bet in my eyes at the time. Even now, after the fiasco, I wouldn’t mind diversifying into something like IBHF or Shalibadra, but once again, I feel that DHFL offers the most value. Indeed, I have increased my stake in DHFL a few weeks back and even looking to increase a little bit more.

I am certainly cognitive of the threat the market mentality can cause to a BFSI firm. We all know what happened during the ICICI bank run “just” because of rumors. DHFL’s promoters also have a bad reputation (For being allegedly involved in shady stuff, the likes of which may never be proved). But their handling of the crisis and attending to shareholder/debt holder queries was impressive. They also followed up with some great moves like buying back their own papers at a discount and Securitizing some of their loans. So unless there are skeletons in the closet or black swans around the corner, I am comfortable.

However, as a rule of thumb, I would never let any BFSI stock (Read: Highly levered stock) be more than 10-15% of my portfolio. So within that limit, I wouldn’t mind loading up on DHFL or any other BFSI stock.

I believe Mr. Munger was alluding to the SSGR. His statement applies only to mature companies earning almost stable levels of RoE. In the short term, as a company is growing towards maturity, it can very well grow its profits above the SSGR by utilizing several tactics: Increase Margins, Increase Operational Efficiency (Fixed Asset Turns), Increase Working Capital, Increase Leverage etc To be honest, in a developing country like India, it is difficult call any firm ‘mature’. Perhaps about 10% of India Corporates are mature. Most of them have a long run way ahead of them. We as investors should feel very lucky to be investing at a time when India’s Demographic Dividend is being paid out.

Even assuming that the statement is universally true for all types of firms, at all times (It’s not), the stock price will grow at the same pace as the RoE given that it fairly priced. If it was under-priced or over-priced when an investor first bought it, the statement may not hold true. That is to say, you can buy a High RoE company at an elevated price and end up making less in terms of returns than from buying a Lower RoE company at a discounted price. That’s essentially what investing is all about anyway-- buying stocks for way less than what they’re worth.

Again, what’s discussed above answers this question too. In fact, if you can, go back and look at how much DHFL’s RoE was from 20 years back and what’s been their profit growth rate from then to today. You can actually do it for any BFSI firm to arrive at the same conclusion.

Dr. Vijay Malik wrote a nice piece on the SSGR if you wish to read it:

In the above article,answering to a question the doctor mentions "SSGR is primarily useful for manufacturing companies and would not be very useful for sectors like financial institutions like Banks/NBFCs/HFCs. Further, to complicate the matters, the information shared in the annual report of financial institutions is not sufficient to assess their financial position, therefore, I do not attempt to tweak/adjust the SSGR to suit FIs.

I would suggest you to proceed with you adjustments to SSGR formula with Net Long Term Loans and other such parameters and see the outputs to determine whether it is able to differentiate between good & poor performers in HFCs and other FIs."

Have you done any analysis on DHFL based on a tweaked SSGR Dinesh?