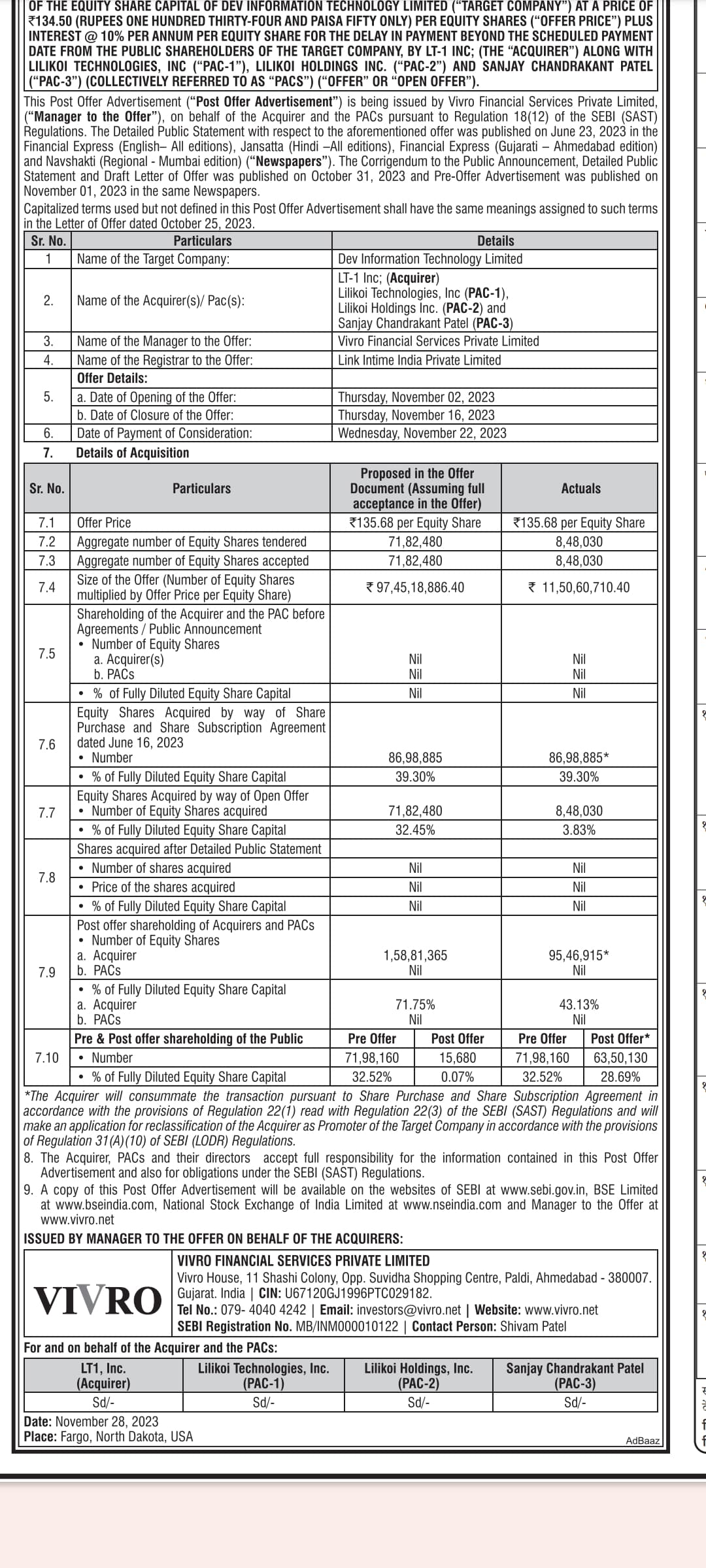

The Open offer & Preferential issue details:

The existing promoters decided to 31.22% of their stake to Lilikoi Holdings, a USA-based IOT company & issue new preferential shares at INR134.5 per share aggregating to 20% of the share capital.

After this transaction, the new promoters will have a 51% stake while the existing will continue to hold around 17% stake (as per the emerging voting capital).

This transaction then triggered a compulsory Open offer at a price of INR134.5 to acquire a 25.8% stake from the remaining shareholders.

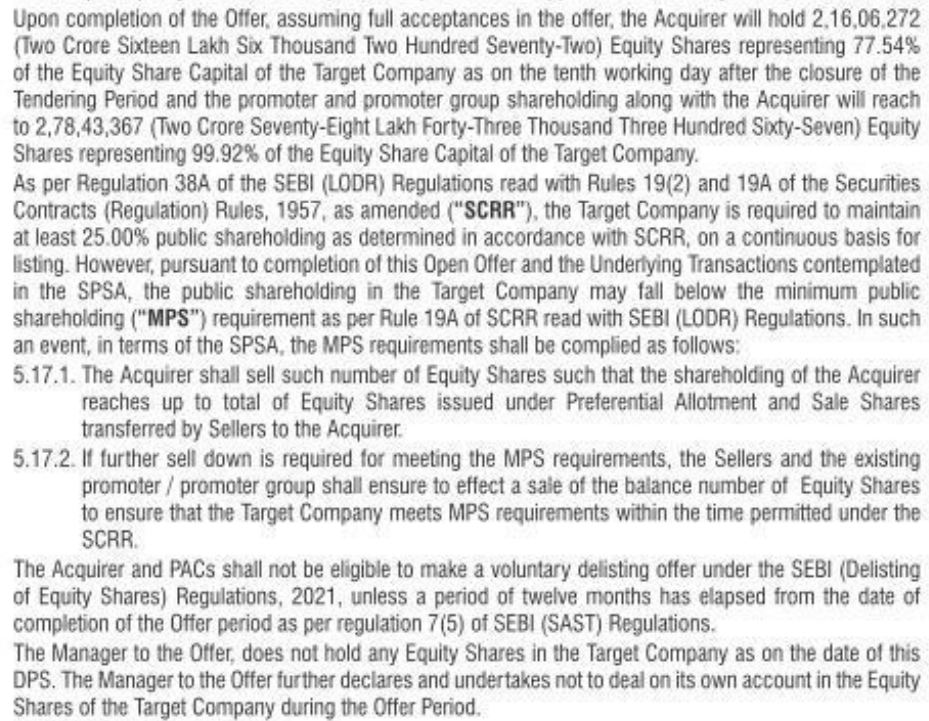

Post the completion of the offer, the total promoter holding will stand at 99.78% (much above the maximum limit of 75%) & so the promoters will be required to sell some of their holdings to reduce the number to 75%, i.e. basically the new promoters 25% shares acquired through open offer will be required to be resold in the market most probably.

Timeline of the offer-

Why is this a special situation?: Well, firstly change in Management can be a big trigger as we have often seen in the past, however, not all management changes translate into returns, & therefore we need to understand the fundamentals as well.

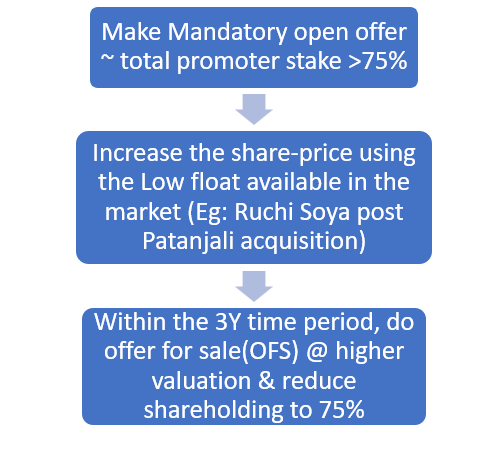

THE SPECULATION PLAY:

The acquirer owing to the laws of the country is required to make a ‘mandatory’ open offer even after acquiring a 51% stake in the company. Further post the open offer, because the existing promoters want to retain some of their shareholdings ( as they will continue to manage the business), the new acquirers will be required to ultimately sell the shares which they acquired in the Open offer to maintain the maximum promoter shareholding requirements.

However, this means that the company can possibly use a window of 3 years to reduce its stake, & owing to the negligible float available in the market, it can increase the price of its shares (which can obviously be in parallel to its improved operational performance) & then use this low float to get a higher valuation for its shares that are recently acquired.

Note: this is completely speculative in nature, however, we have seen recent instances like the case of Ruchi Soya where the promoter (i.e. Patanjali) pulled off a similar trick & everyone knows about Adani’s crazy valuations which were partly helped by its very low float in the market.

Now, although one might not invest in this company solely based on this factor, I believe this ‘incentives play’ will be the key contributor to its stock price growth (if it even happens).

Now this was about the speculation aspect, let’s understand the fundamentals of the company-

Brief History:

Dev IT, an Ahmedabad-based IT company, was incorporated by Pranav Pandya & Jaimin Shah ( An ex-Oracle Partner based on our scuttlebutt) in 1997.

Geographical Presence:

Key products & services include:

A) Services:

B) Products: Talligence & Bytesigner

C) Coworking solutions - ‘DevX’ where the company has around 32% stake (based on the Q4 numbers, however as per Q3 investor presentation, it had 44% stake)

POSITIVE TRIGGERS

- Geographical expansion- With Lilikoi’s presence in the USA market, it will ensure DEV IT’s services reaches a broader customer base.

-

Decent growth in the existing biz - The recent FY saw the company turning profitability after several years of losses, & with the company’s Talligence product & DevX scaling up, the profitability should improve going forward.

3)Change in management can bring a substantial boost to the company’s IoT plans-

Lilikoi Holdings, a USA-based IOT company through its step-down subsidiary LT1 is acquiring the company at a valuation of 300 Crs! Which is the second largest IT-based acquisition for a Gujarat-based company.

The acquirer is a major player of IOT based products, therefore his capital, expertise & connections will help in scaling up this division in different geographies & transform the company into a leading IOT player (potentially)

A brief look at the company’s website:

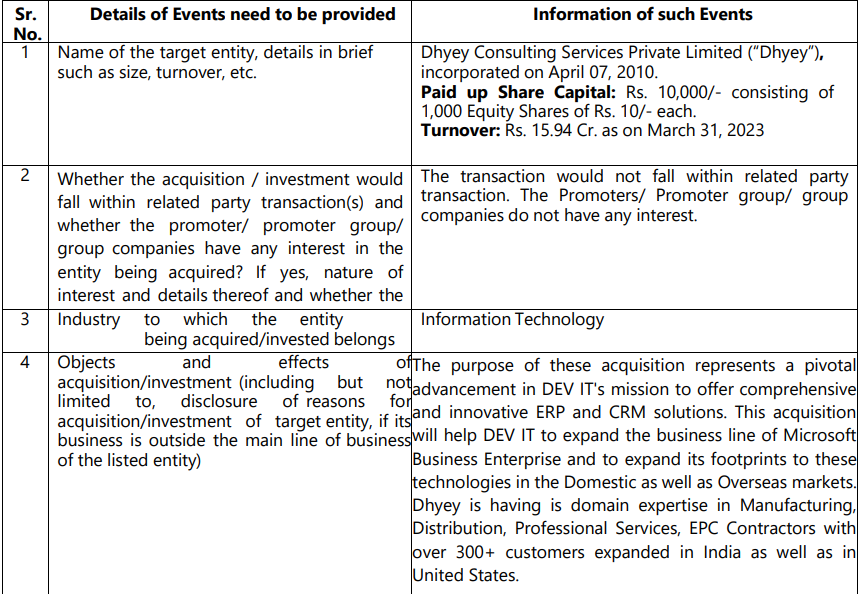

4)Capital infusion to accelerate growth: The company was not only cash strapped due to capital infused in the development of its new products like Talligence & Bytesigner, but also due to offshoring attempts by opening offices in Canada which are yet to yield the desired results. The company even tried to foray into Blockchain technology, but it was not possible to scale those products without capital.

Thus, the capital infusion of 77 Crs through preferential allotment will ensure that the new promoters can expand the service offerings by Acquiring new products & even companies which will again trace back the company to its growth journey.

-

A hidden gem in the form of DevX- The company through its associate company ‘DevX ‘has developed an ecosystem where it not only provides startups a workspace leasing space but also ensures that they can create allied services in the form of training & mentoring startups & business consulting. While Globally the returns made by the office leasing industry have been sub-par, the company’s edge lies in providing the additional services & eco-system which can not only help in retaining the startups to continue leasing the space, but most importantly the start-ups taking the lease can be a fertile ground for the company to choose from for acquisition purposes in future.

-

The transformation from a pureplay software developer to an AI/IOT-based player might lead to valuation rerating when profitability comes in the future-

- Lack of any major financial risk- owing to the substantial funding rounds coupled with lower capex requirements, the company has very low debt in its balance sheet which is a positive.

Now let’s see the Negatives & key risks:

- High single client concentration risk: Revenue from the top customer contributed 32% of the total sales in FY22.

- Very low profitability: The normalized EPS from operations stood at appx. 1.5 Rs Vs the reported 4 Rs owing to the impact of other income in the form of the sale of a stake in Dev Accelerator.

- Sale of shares in Dev Accelerator at a very early stage- The company in November sold off roughly 12% of the company’s stake & reduced the stake to 31.22%.

- Very low Scale - The company not only does generic software development & maintenance services but the majority of its revenues are also derived from Govt. projects like GIFT city etc, which might not be a steady stream for revenues.

- Reducing margin profile - While the company has made efforts in increasing the contribution from its products portfolio like Talligence etc, this has led to a reduced margins profile owing to the razor-thin margins in the products business.

- Inability to identify any competitive advantage which can possibly justify its 300 Crs valuations!

- New fundraising despite doing a preferential issue a few years back & an IPO in 2017 is a major red flag- The new funds raised will be used predominantly for acquisition purposes which is also a very risky strategy.

- Stretched working capital cycle & lower margins leading to poor returns on capital:

The company’s ROCE has been very low due to poor capital allocation (although ROE looks high, it is solely due to the low net-worth effect, & ROE is positive purely on a standalone basis). Plus, the company has also done several write-offs of its investments in the recent past highlighting the poor capital allocation.

-

Potential inability to attract talent: The company pays extremely low salaries to its employees with the average salary being only Rs.15,000 for its 950 employees. Further, the promoters themselves only have an average salary of 30 lakhs each.

This not only translates to inflated Profits (as the employee expenses are very low) but also leads to a lack of quality talent in the team owing to poor salaries.

- Revenues from Govt (which formed around 70% of total revenues at a certain point) is a major risk

About the Management team:

- Promoters & their roles:

- Pranav Pandya (Chairman) - Operations & building clients & relationships

- Jaimin Shah (MD)- support the company’s growth, manage critical finance function and adhere to regulatory and compliance requirements.

- Vishal Vasu- CTO, R&D at DevLabs, leading the Information Technology function for DEV IT

provides technical direction across the company in areas of managed services, architecture designs, software technology, and cybersecurity thus supporting project development that fuels business growth.

- Prerak Shah- came back to India after 14 years in 2009, & currently spearheading its PMO, processes, and community-oriented activities.

Concluding Views: The company’s recent profitability has been hit partly due to emphasis on product development which does take higher initial expenses (& then offer non-linear revenues if scaled up). But it is very difficult to bet on this company currently purely based on the past track record, however, given the potential speculative play as well as the new promoter’s competence in IOT & the company’s strong cash positioning post the preferential issue, it can be an interesting stock to keep a track off especially if one wants to learn more about how to open offers pan out live …like I do ![]()

Note: Not attaching any financials or my valuation framework which generally reflects the past financials…as although it does look expensive currently, the bet is more on the low float & transition to an IOT company owing to the reverse merger with Lilikoi. And projecting these triggers is not possible at the moment as per my view.