Summary as on 27 February 2025

Company:

- One of the largest cable TV and has largest Subscriber Base amongst all cable players in India. Presence in 13 states .

- On 17 October 2018, Reliance Industries announced that it had acquired a 66% stake in DEN for ₹2,290 crore (US$260 million) . (You can buy now 100% of the company for lesser price than this)

- Reliance acquired an additional 12.05% stake in DEN in March 2019 taking its total stake in the company to 78.62% .

- Provides broadband connections as well .

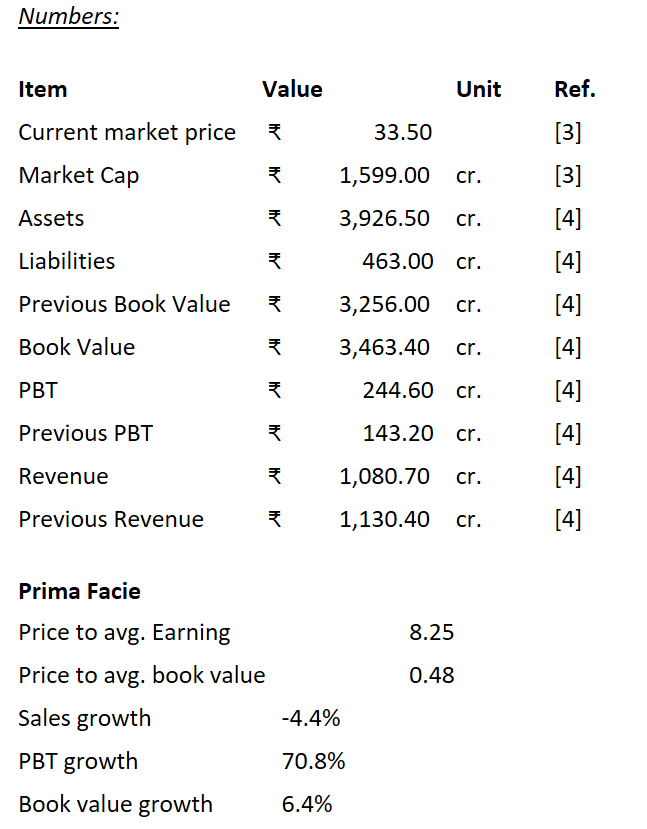

Figure 1: A Prima Facie Look.

A deeper look

Clearly we have a very undervalued company here. When the local SBI FD gives you a pre-tax yield of 7% or PE of 14.28 (1/7%) and Nifty trading at a PE of 20 . We are getting a relative discount of 42.22% and 58.75% compared to FD and Nifty respectively. It is true that the company is in a dying industry and the average consumer is consuming content via YouTube, social media and what not, clearly indicating the decline in sales growth. So giving it a no growth PE of 14 is much more ideal. However, how is the assets increasing and the book value increasing when sales are declining? A closer look at the balance sheet is required then as seen in Annual report Pg. 114 . Please note that the values in Annual report are in Rs. Millions and I am using Rs. Crores. 1 crore = 10 million.

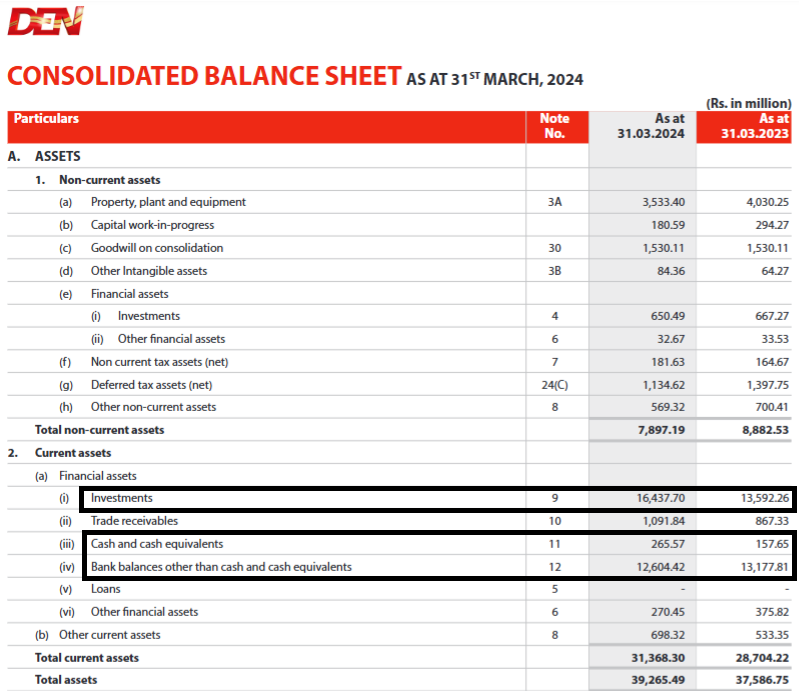

Figure 2: Assets in the Balance sheet.

Something that should hit you in the head. The company has ₹ 1,643.7 cr in Investments and ₹ 1,260.4 cr in cold hard cash. In the Note 11 and 12 in Pg. 140 gives the complete picture of the cash and cash equivalents aspect.

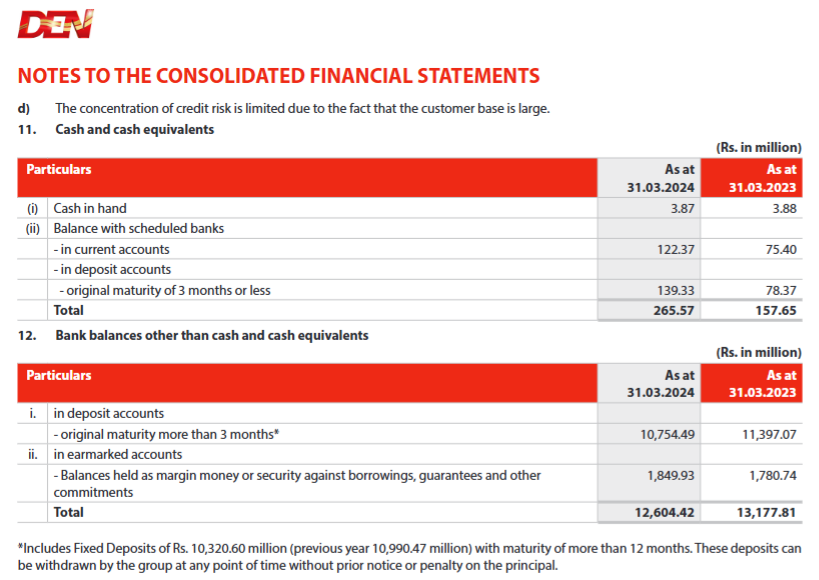

Figure 3: Cash in Balance Sheet.

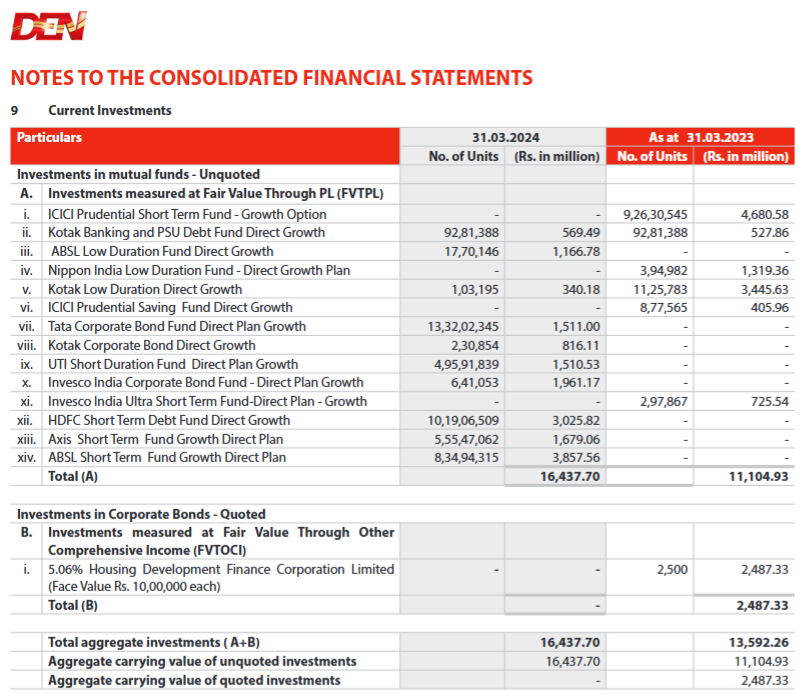

Now what about the “Investments”? This can be seen in Note 9 in Page 138.

Figure 4: Investments in Balance Sheet.

All of the investments are in short term debt mutual funds which is as good as cash but since we are a stickler for accuracy. Assuming they are holding these funds even now which I don’t think is a good assumption given the difference in holdings from previous year, I don’t know why given every time you transact you have to pay a capital gains tax and every time you buy you have to pay STT. (Lol, I just realized these are liquid and short term funds, I could just multiply the value to 1.07X to get a good assumption of the present value and cash can be multiplied with 1.03X which you will get if you put in Savings Bank, however, I have taken cash and bank balance as given in Balance sheet. So prospective return should be higher.)

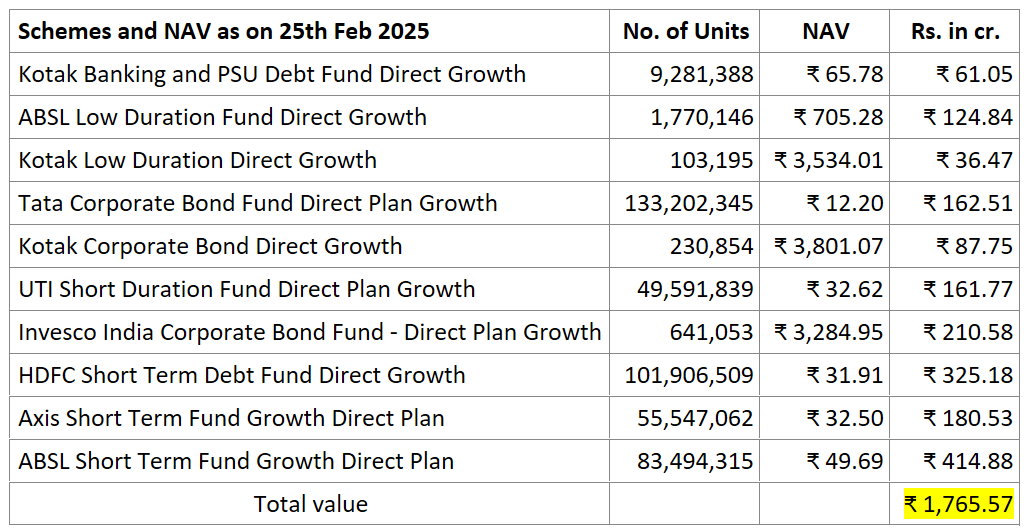

Figure 5: Present Value of the funds.

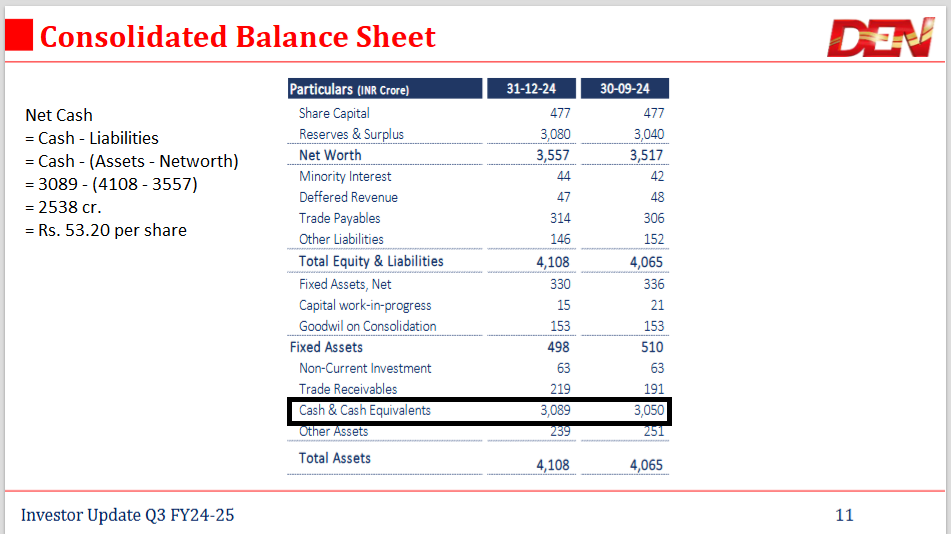

Giving this a 100% credit in cash, we can say that company as a total cash in its 1765 + 1260.4 + 26.55 = ₹ 3,051.95 cr. This value is actually lower than what the company reports which is ₹ 3,089 cr. from their investor presentation for Q3 FY24-25 Page 12 .

Figure 6: Updates from latest PPT.

So the enterprise value of the company is now = Market Cap + Debt - Cash = 1,599 + 463 - 3,051.95 = - ₹ 989.95 cr, yes that is a negative value. A company with zero EBITDA will have zero as enterprise value but Mr. Market is saying it worth less than that. To illustrate the absurdity here. You can buy the company for ₹ 33.3 per share. Pay all the liabilities with the cash and still have cash of ₹ 54.27 per share remaining and have a business that makes earnings per share of about ₹ 2.09 per year. If we give a PE of 5, the business should be valued at = 2.09*5 = ₹ 10.45. So you put in ₹ 33.3 rupees and take out ₹ 54.27 + ₹ 10.45 = ₹ 64.72 per share. A simple approximate 2x your money.

This is a net cash value of the company is = 3,051.95 - 463 = ₹ 2,588.95 cr. The Price is now trading at ₹ 1,599 cr MCAP. A cool 61.9% return to go to net cash value when FD is giving 7% and Nifty gives 12%, beats any asset class essentially risk free. A pure Graham stock I would say, Late Walter Schloss would certainly buy.

A no growth, shrinking company like this should ideally be trading at a EVEBITDA of 5 (super conservative), Taking EBITDA of 100 cr, we see an EV of 500 cr, given the above values for Cash and Debt, we should see an MCAP of = 500 + 3,051.95 - 463 = ₹ 3,088.95 cr. , a return of 93.18%, A screaming buy!

But is it really a bad company? Well, the company as a Net operating assets (NOA) = Assets - Cash = 3,926.50 - 3,051.95 = 874.55 cr. From these assets, the company made a profit of about 122 cr, which means the company has a RNOA of = 122/874.55 = 13.95%, still better than a FD and Index Fund. A company in a dying industry, not a candidate for the core LT portfolio, a good LT swing trade at best.

But if I were the management, I think the best call of action would be returning the capital to shareholders so that they can invest that capital in index funds of 12% return with diversification of 500+ companies than just one company, or deploy capital at greater than 15% return businesses. I do not think Reliance cares about this subsidiary which is barely 0.1% of Reliance MCAP.

What does the chart say?

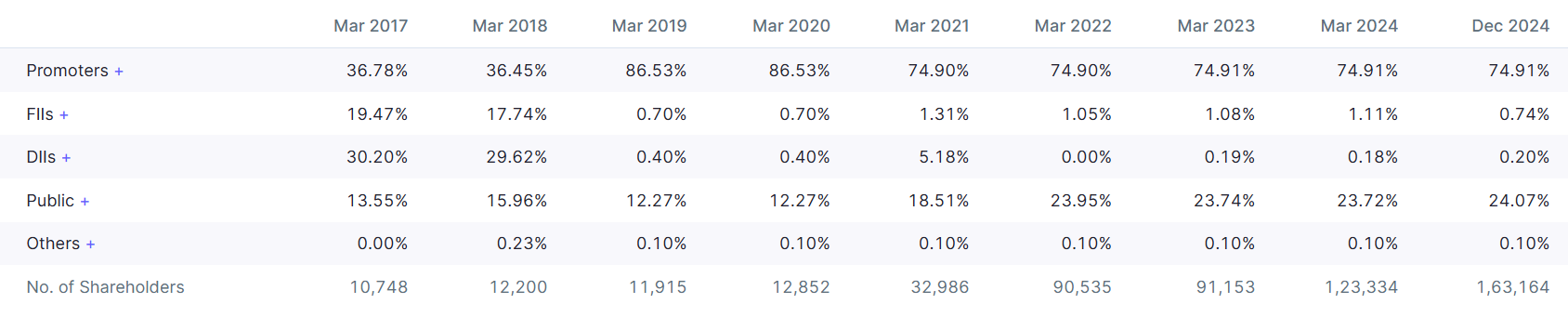

Figure 7: Shareholding Pattern.

Looking at the shareholding pattern, we can see that almost all DIIs and FIIs have sold out on this stock and the only holders are the promotors and public. Seeing as the promotors are already at the 75% mark, them doing insider buying or buy backs is not likely.

Figure 8: All-time stock chart.

I don’t think I am much of a technical analyst. But if you see the all-time chart, the stock hits ₹ 30ish and then shoots up at high volumes. Making it highly likely that the stock will go up soon. The stock has downward moment as it trading below 200 DMA and 50 DMA with little volume. The volume 20 D average is 606k. The free float shares is only = 47.7/4 = 11.925 cr. Which means the average public shareholder is only holding about 200 days. If the stock goes even lower, then the prospective return is only going to increase and becomes a more stronger buy. The stock is currently trading at all time lows!, lowest PB levels, lowest PE levels, surprisingly not the lowest market cap to sales.

The ideal CEO or capital allocator would give this capital back to shareholders so that the shareholder can generate a better return that the Debt funds that the CXO is choosing. I hope we as investors can force the board of directors to act in the best interest of the shareholder and return the capital in any shape or form than reinvest it in a low return asset.

Biggest risk: Board and Management don’t return cash or make no effort to improve ROE. Then you are left holding the bag and value trapped. So position accordingly. Reliance says give royalty fees and take all the money. It is quite risky. It is far better to be in a wonderful company paying a good price rather than a so-so company at a wonderful price. However, I am just curious to see if this cash bargain works out.

Disclosure: Invested and Biased