Great thanks! Do you have any working numbers/valuations for Eureka Forbes and how do you look at it? Not asking for advice or anything, just your opinion. Trying to learn here!

I read ’ You can be a stock market genius’. Now, should I wait for listing of Eureka Forbes, and the selling by FII/DIIs and then buy maybe? Any help is appreciated.

FII/DII do not hold much stake and there is no reason for them to sell it. Selling by FII/DII typically happens when the category(large/mid/small) of company changes. That’s not the case in Eureka Forbes. Valuations will be more clear when Eureka Forbes starts reporting its numbers. Currently, the valuation is around 3x sales. It can go up or down depending on the performance.

From Neil Bahal newsletter

5 Likes

Yes I am aware of his newsletter. That is why after reading I came to this forum.Do you hold the company and will you be buying/selling post listing?

Also, how can I track when the new company would be listed?

1 Like

Also, are there any good sources to read about demergers and spin offs? I am aware of the following resources -

- You can be a stock market genius book (by Joel Greenblatt)

- itsTARH twitter account

- Neil Bahl Newsletter

- Dashboard on special situations by investkaroindia

Sorry if this is a spam and an earlier resource list exists. And if anyone can guide to me it, I shall be thankful.

4 Likes

I will be buying more after Eureka Forbes lists. You can check the Forbes and co announcements to find out when Eureka Forbes will list.

I would suggest you to go through this thread. You will get a good idea of special situations and references that can help

1 Like

As per a recent announcement in the NMDC conference call, the new steel plant demerger should be completed by March/ April, unless an approval is to be sought by creditors in which case it will be in a couple more months.

As I understood,17000crs worth of equity is to be given to the current shareholders of NMDC in the new company. Could anyone shed some more light on any possible value unlocking for NMDC shareholders, assuming a purchase price of Rs. 140-145 (which is the average stock price of the company)? or would it be too early and we should wait for a swap ratio to be determined?

Disc. : Invested

Steel plant: coke oven will start at the end of March or beginning of April, and hot metal in May or June, finished product by June end or July.

I have a doubt here and it would be great if someone could clear this. I am also invested in Sandur Manganese and there they have already setup a coke oven for their integrated steel plant and are already selling coke from it. Can NMDC also do this?

Secondly, there can be massive increase in margins of the steel plant as they will increase production from 2 MT(FY23) to 2.5MT(FY24) and finally 3 MT(FY25). This is just debottlenecking and rampup and thus doesn’t require much capital.

Additionally, the management mentioned that there is land to increas the steel plant from 3 MT to 6 MT. This provides a lot of longevity. for the steel plant.

According to some analysts the Steel plant will be valued at around 20000 crs (very conservative ly). This is just at 1 times book value. Right now steel plants are trading at higher valuations.

1 Like

Is anyone playing the arbitrage on the following cases from other side :-

- GMR - Power & Infra

- Forbes Residual value

I basically want to knw if someone has done detailed valuation of these cases. My ballpark is

(1) GMR - Power & Infra - Thr stake in GEMS which they are planning to sell is worth arnd 3000 crs. The corp net debt will be arnd 2000 crs. So net 1000 crs. here plus the power & road assets with roughly 900 crs. EBITDA shd worst case be arnd 4000 crs.

(2) Forbes - The revalued land assets mentioned in the AR was 600crs. Current mkt cap is roughly arnd 500 crs - rest of the biz free

Love to hear views on these.

Aprt from above, Motherson Sumi spin-off is on the radar as of now. I moved out of GHCL arbitrage & shifted to Ujjivan as potential IRR seemed greater in that case.

Disclosure :- Small position in Forbes(post the demerger) & GMR Power ( due to GMR holding)

5 Likes

I don’t like the management of Forbes and company. I sold all its shares. Yes, it has land bank but market will only rerate it if they can unlock some value out of it. The free float of the stock is very low. So, upside can be huge of they can unlock some more value.

On GMR power, I am not clear about the debt part. I will study it once they publish the new financials. There may be heavy selling in GMR power when it lists because of the heavy FII presence.

3 Likes

Any thoughts on Kamdhenu demerger of paints business?

Disc- no holdings as of now

Any idea on Indiabulls Real Estate? Did something major happen? The stock declined over 14% today. I know they have got the green light for the merger with Embassy. Not aware of any other news.

On the same note, any views on this special situation are invited.

Disc: Not invested. Tracking the entire story

This is because of the below news -

Although this is for Indiabulls Housing Finance but has/had same parent co. and name hence the fall.

1 Like

Ganesh benzoplast demerger: Does any one tracking about it. Liquid Storage division results are looking good. How much time they are going to take for demerger?

1 Like

I had been tracking Ganesh Bezo for couple of years between 2018 and 2020. The company has had a chequered history with a long stint in BIFR (debt restructuring) and I started tracking it as a Turnaround special situation play. The LST division is highly profitable, but the chemical division has always been a drag, even during the phase when the chemical sector in India as a whole has been booming. Also, personally for me, the management does not inspire too much confidence. The second generation of management is in control now, and they are definitely doing much better now, but overall, nothing that excites. The demerger itself had been in the process for 3-4 years now, its been dragged on due to litigation from one of their creditors who had been pursuing the courts for recovery of their, despite the company having gone through the BIFR process successfully. During all of this, one major positive was that Stolt Nielsen Limited (a global major in chemical logistics, one of the largest owners of ISO tank containers in the world) ended up acquiring a significant minority stake in GBL. This happened when GBL acquired 86% stake in an unlisted Stolt Rail logistics (a joint venture between Stolt Nielsen and GBL promoters). So while the overall story has strong promise, its the execution where things tend to fall apart. Encourage you to read the VP thread on GBL for an excellent deep dive.

DISC: No holdings, not an investment advice, please do your own due diligence

5 Likes

One of the special situation I am watching out and invested a small capital is Shalimar Paints. Hella Infra market has acquired around 25% stake in Shalimar paints for 270 crores. The money that will come will mostly be used to reduce debt, working capital and expansion. Today, Mr. Souvik had been appointed on the board of Shalimar Paints who also heads Finance and_ Investor Relations at Infra.Market.

Positives

- Shalimar paints is a very popular and old brand. Most people do know about the brand.

- Infra Market is an online procurement marketplace that offers construction materials and products to build projects. It is backed by the likes of Tiger global.

- This strategic investment should be able to expand the reach of Shalimar paints and will also provide enough capital to expand.

- They are targeting around 1500 crores of revenue(current revenue ~ 300 crs) with 8-10% EBIDTA margin in next 3-4 years. Even if they can achieve 1000 crs of revenue with 8-10% margins, it would be a great turnaround.

Challenges:

- Paint market is becoming very competitive with the entry of Birla and JSW.

- High oil prices

- The company has been making loss for last 5-6 years

Investor presentation - https://www.bseindia.com/xml-data/corpfiling/AttachHis/d8296997-de3c-4798-9921-c29ef84ac051.pdf

Recent concall: Shalimar Paints Earnings Call for Q3FY22 - YouTube

10 Likes

As they have sold so this start to look more over it the new management changes are pretty good in Eureka Forbes.

A good leader is comming a high positive but will advent want to make company private also

4 Likes

Open offer will be triggered once Advent takes control of Eureka Forbes. We have to see the price at which open offer gets triggered. In case they want to take it private, they have to sweeten the price. In case of ABB power(after demerger from ABB India and management change to Hitachi), the open offer price was below the price at which the stock was trading and hence the open offer was not successful. I hope that Eureka Forbes remains listed.

2 Likes

5 Likes

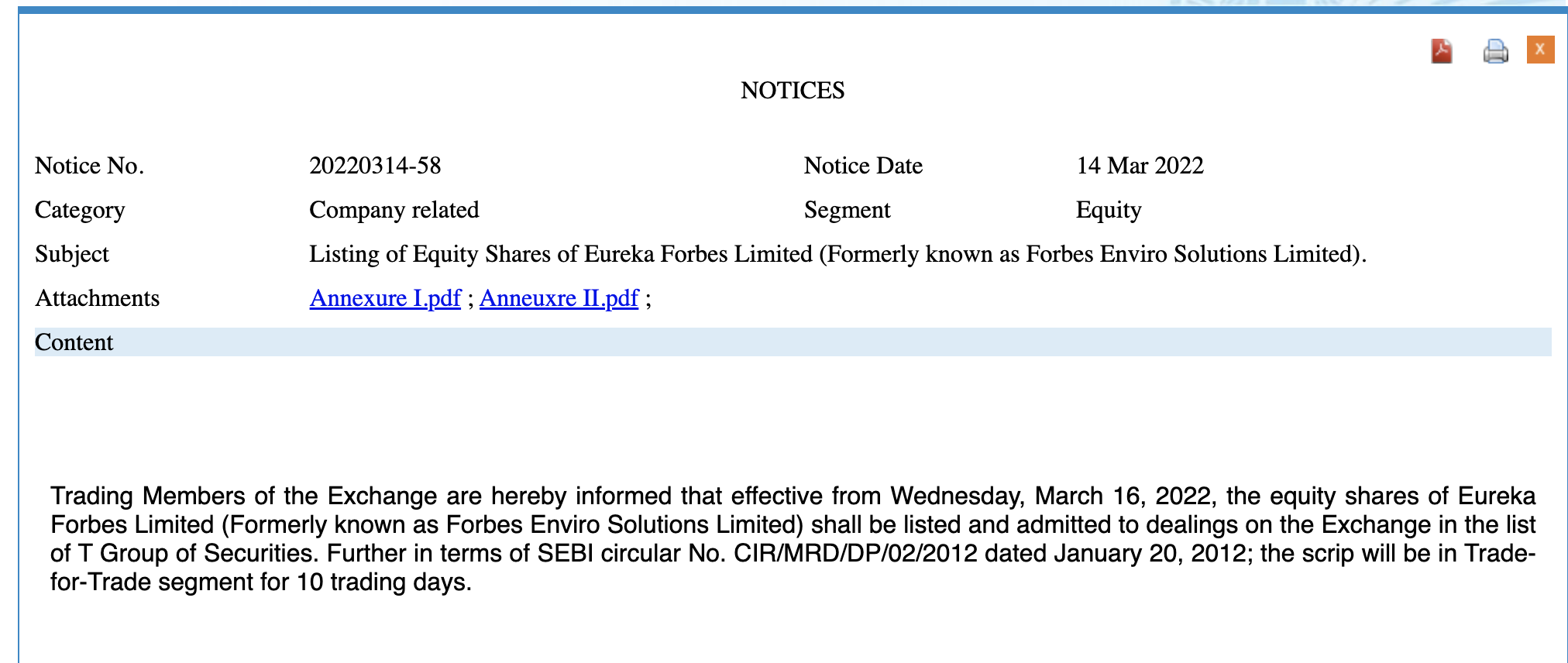

Eureka Forbes listed today at around Rs 495 and it is currently in lower circuit at Rs 470. Open offer price is Rs 210 which will make sure that Eureka Forbes will not go private unless new promoters increase the open offer price.

Overall, the demerger has been rewarding to the shareholders of Forbes and company. Those who hold Forbes and company after the demerger was announced last year would have made around 3-4x. I have closely watched this demerger and will share my learnings soon in a detailed post.

17 Likes