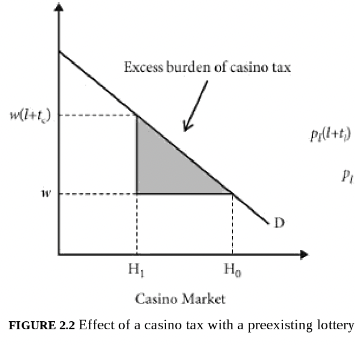

Macau please

38%

Largest casino gambling jurisdiction.

Credits : The Oxford Handbook of the Economics of Gambling

I think investors have still not completely understood the magnitude of this decision. It isnt the tax rate of 28% that matters, but rather the fact that it is going to be levied on the full face value of the chips rather than on the casino’s revenue. So if you go to Deltin Royale and wanted to buy chips worth Rs 1000, you would now have to pay Rs 1280. This used to not be the case earlier. Earlier, you would get Rs 1000 in chips for Rs 1000 and the casino would pay 28% tax on the amount you lost.

In my opinion, this is a complete killer. Though we have to wait and see the impact, I think the casino under this rule becomes effectively a worthless operation. I was trying to find any examples of geographies where tax is levied this way at a rate higher than 5% and still has a thriving casino industry and couldnt find a single one. See example of Kenya where a similar tax was introduced at a comparable rate and completely destroyed the industry.

In my view equity of the company ex of the cash on the books now only has option value. It will be valuable again if the govt decides to rollback this tax, else the equity value is probably 0 for both the casino and online gaming operation. This is unless the company finds some creative loophole to get around this tax.

7 Likes

Risk highlighted by you are spot on… one of the risk GST increase to 28% is happening now.

1 Like

I always thought Government would not take such a step otherwise the local economy will be hit heavily. They did it anyway.

This is severely going to affect the economy in Goa. I think Delta Corp was one of the largest tax payers in Goa. They have been made to pay license fees to the Goa govt even during lockdown caused by Covid.

Hand twisting it seems - read GamesKraft case with GST Dept.

Looks like GST Dept has some kind of issue with all this.

Offline casino business already pays 28% (75% revenue FY23)

Online business will have a +10% tax from 18% GST.

Negative effects on DeltaCorp(https://twitter.com/hashtag/DeltaCorp?src=hashtag_click)

- loss of some revenue

- loss of investment/FDI

- loss of mkt share to illegal gaming

So -25% mcap overreaction?

2 Likes

illegal gaming is an over reaction specifically for Delta corp.

Organised to unorganised is really not something historically folks have banked on.

Market is not overreacting. According to news channels, earlier 28% gst was not on the total face value i.e on the value of chips purchased. This makes delta business unviable as of now, but I am sure Delta will somehow mitigate this, may give players extra credit/incentive after purchasing chips, or some sort of taxation loophole which will surely hurt some profitablity. According to Najara ceo, this move just killed online gaming industry completely. In future, there is possibility that govt may change the rule also.

I have sold my holdings as of now. Will observe.

1 Like

I initiated a position in Delta Corp ~6-7 months ago and it constitutes 1% of my pf. Usually each stock pick is 3-5% of my portfolio and I build this position over time basis my conviction.

I have 1% in Delta due to the uncertainties the business faces on different fronts, mainly taxation and political issues, thus the lower conviction. However, on the flip side I like the direction the company is going in and the fact that it allows me to own a company that is very different from what I usually own (steady compounders in the consumer space).

After yesterdays GST announcement and the subsequent drop, here are my 2 cents.

Known business risks:

- Taxation. Will forever be a concern with this business, I won’t be surprised to see other taxes added over time.

- Political issues the business faces (esp. during elections). Will always remain a factor.

- Geographical concentration, may ease up over time, especially as the Indian economy grows

Near term risks:

- Possible slowdown in business, hit on margins and profitability due to the tax change

- Delayed IPO of the gaming business

- Pressure on stock price till things settle down

Un-factored risk:

- Retrospective taxation demand. If this ever happens it will kill the business and everything good, bad and ugly will cease to matter

Upcoming positive triggers:

- Land parcel owned by the company is being developed into residential properties. Will be ready in Q2 FY24, will be monetised over FY24/25 (source: Delta Corp's Jaydev Mody On Firm's Business Outlook, Expansion Plans & More | Inside Out | CNBC-TV18 - YouTube)

- Doubling capacity/new gaming positions with the new vessel by end of FY24. Full impact to be realised in FY25 (source: concall)

- In 3-5 years they are building entertainment city in Mopa (next to the new airport in Goa) on 100 acres of land. Another 1500 gaming positions will get added (source: Delta Corp's Jaydev Mody On Firm's Business Outlook, Expansion Plans & More | Inside Out | CNBC-TV18 - YouTube / concall)

- ~550 crores cash on books (10% of market cap) (source: concall)

- Dark horse: IPO of the gaming business will see light of the day sometime. I think this business over time can be as big as the offline business

- Joker in the pack: Awaited Daman verdict

I think 1-3 are things that should play out with a higher degree of certainty.

- #1 will add more cash on books

- #2-3 will increase gaming positions 4-5 times over ~5-6 years, which means profits should rocket over the next 5-7 years.

#5 is now uncertain, though over time things will get clear about that too. The online business being as big as the offline business is my feeling, may not happen.

#6 is the joker in the pack, if it works out it will immediately double their gaming positions. However, after the tax thing yesterday, I feel they will lose the case (courts don’t rule favourably when sin products are involved is my take).

Other positive factors:

- Growing per capita income means the business will only grow over time, demand at their casinos is already high

- Addictive nature of gambling. People that drink and smoke, will drink and smoke. People that gamble, will gamble

- Mopa airport will bring more people to Goa, that is good for the business

- Heavily regulated business mean high barriers to entry

- Leader in the casino space

- The GST ruling has cleared the tax overhang on the stock

I have had all these thoughts swirling in my head since yesterday, thought best it is to pen it down and forget about it ![]()

Waiting for the dust to settle to continue SIPing in the stock and further building my position limited to 1% of my pf. Of all my stock investments, this business remains the ‘value pick’ in my pf.

Downside: At the extreme, I lose all my money and 1% value of my pf.

Upside: It could be huge from these and upcoming lows from a 5-yr standpoint.

——

Some interesting quotes from mgmt on the demand (picked from the last con call)

-

Q: Demand from high rollers vs casual rollers:

- We don’t have any such breakup that we maintain or we have anything because, again, if you see the average GGR, that we generate per person is about anywhere between 14,000 to 16,000 or 14,000 to 17,000 ahead. So, and I don’t know whether you have been on earlier calls as well or no, but we are a company which is wanting to be more like a family destination and a retail attracting customers. There are the high-rolling business is not something that we rely upon, and it’s very, very miniscule as far as our larger picture is concerned. So that’s my answer to you.

-

Deltin Royale, when we had introduced, I think we haven’t seen a weak opening at all. We’ve always been lucky or since the demand is so high, because as I said, Goa attracts close to about 10 million people a year, which is one crore people a year in visitations, okay. And the total intake of all the vessels put together today will not be more than, I don’t think more than 20 lakhs a year. So you have 80 lakhs people who are un-serviced even today. So I think the demand is very high. And by virtue of that, you will not see underutilized assets in any case. Having said that, again this is not a business like the steel plant or the cement plant that you operate at 100% capacity or 110% capacity. It’s a very, very subjective business in terms of the quality of people that you get on board. But to answer your question, I think we have been fairly utilized from day one.

-

We have never factored in Daman Casino ever in our discussion. We believe that that is, for our investors who believe in us, that is an option value. What I can only tell you is that we genuinely believe based on the international demographics, which are very easily available. And it’s an internationally accepted fact that a casino with a 10 million population in a four-hour driving distance is a gold mine destination and you have examples in Las Vegas itself, Foxwoods in Connecticut and whether you even look at Macau for that matter, it is the mainland China which feeds into Macau. And therefore, if you have a 10 million population in a four-hour driving distance, it’s a gold mine. Daman, I will only give you the statistics and you can then imagine whether it can be as big as Goa or bigger than Goa. Daman has a 50 million population in a four-hour driving distance, which is five times the population that makes it a gold mine, standard casino destination, anywhere else in the world

16 Likes

So earlier, it was 28% on GRR (Gross Gaming Revenue) but now it will be 28% on face value (the amount that the customer uses to buy gaming chips to play). That is the fundamental difference and can have a huge negative impact. Is that correct or is my understanding wrong?

Which also means that the moment you bet, you have already lost 28% of your capital. Correct?

1 Like

This will help. Govt wants retrospective taxation also.

2 Likes

Retrospective taxation will destroy the company. And it isn’t a Vodafone like scenario where the government will be flexible. That is still an essential service. Casinos aren’t.

Any retrospective taxation action if it materializes makes me a seller.

3 Likes

Retrospective taxation will kill the industry. Govt. is hell bent on milking all possible sources of revenues. Pahle free me baato chunav jitne ke liye, phir industries ki kamar tod do.

i just read Annual report.

85% income of company comes from offline gaming business. online gaming earning comes nearby 15%. so how about thinking in this way that if stock correct 30 to 40% than it can be good buy. looks valulation is good and for business part, major income comes from offline gaming platform.

1 Like

Point taken. How I am thinking is that if I spend Rs 100 and I have already lost Rs 28, then what are the chances of me making any money at all. On the 72 if I make anything, again I am taxed at my marginal rate (say 30%). So the odds now of making money are squarely in favor of the government and much much less for a player. ![]()

3 Likes

Currently, the casino and online gaming industry is paying 28% tax on GGR (gross gaming revenue) which is basically their commission or rake. In the latest GST council meeting they announced that this would be changed to 28% on face value (amount of chips purchased). So effectively, you would have to pay Rs. 128 to get chips worth Rs. 100. This would be a drastic negative for the company and the entire industry. Casinos online and offline would become very unattractive and delta corp would not be worth a fraction of what it is today. Now many companies including fantasy players like dream11 have appealed to the government to re-think this decision as it would lead to lakhs of job losses. To this appeal, the Minister of State for Electronics and Information Technology Rajeev Chandrashekhar has said a couple of days back that the whole regulatory framework for the gaming industry in India is very nascent and keeping in mind the industry’s plea, his ministry will request the GST Council to re-consider it’s decision. If the GST Council does re-consider, then the current stock price of Rs. 190 is a very attractive entry point in my view, but if they do not change their stance then the future of the company as a viable business is in doubt and I would be a seller at any price. Would be very keen to hear what the company has to say on 25th in it’s analyst call.

8 Likes

Last update on Daman case:

“Due to paucity of time, stand over to 27/07/2023”