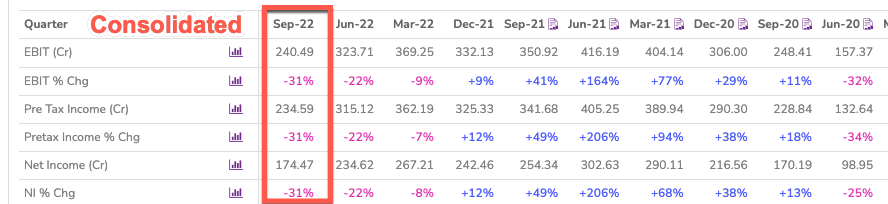

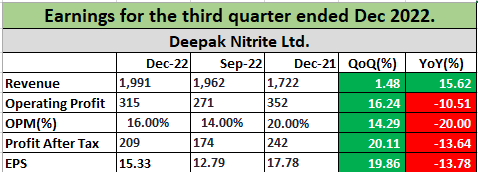

Standalone Numbers are very good !!!.

3 Likes

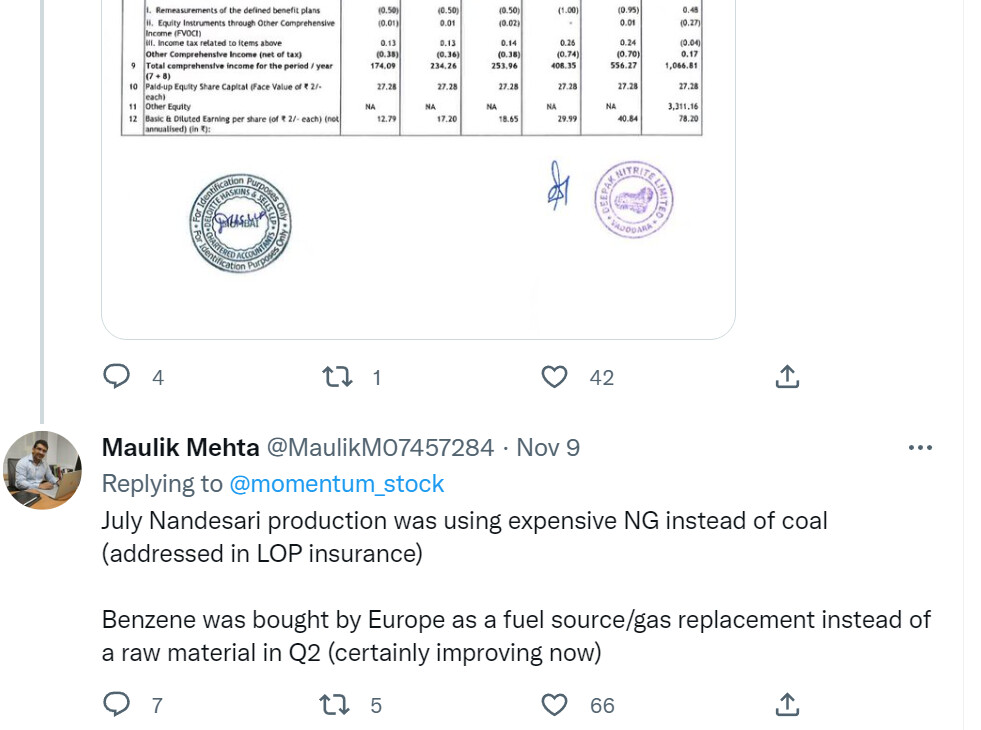

What is the insurance, he is talking about?

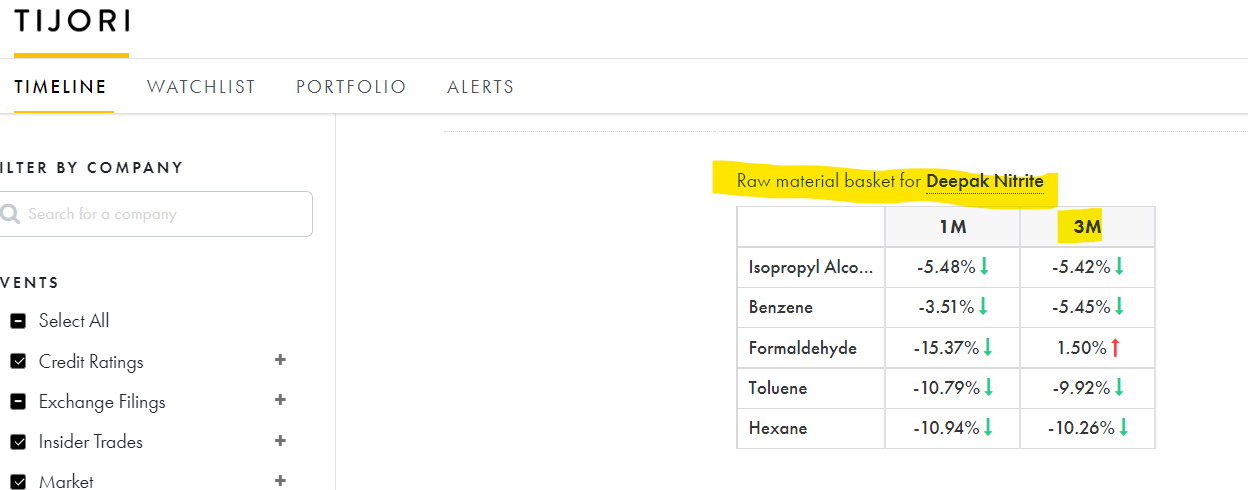

They used natural gas for production in nandesari plant in previous qtr. So loss due to that…

3 Likes

Q2FY23 Notes

a)Nandesari operation has been initiated from July month in Phase manner and from October onwards it is working at full pace. Even at Nandesari we’re getting Natural Gas which is dearer than other sources. Hence, leading to high Power & Fuel cost.

b)Demand looks stable this quarter. However, we saw significant impact on Raw Material and especially Utilities (Power). This quarter we saw decrease in price of Phenol in the initial half of quarter and significant rise in RM price (Benzene)

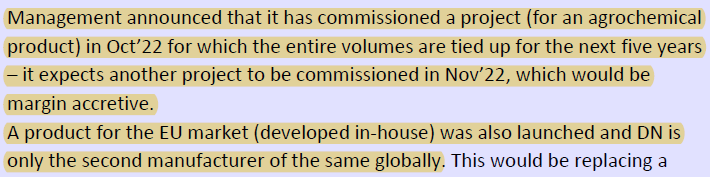

c)In November month we expect one project to commission this is for Margin accretive product for Deepak Chem and other CAPEX also progressing well and on time.

d)Deepak to invest 51% stake in new entity established in Oman due to cheaper and cleaner crude available in the country. Also, the products going to be manufactured are existing ones with good deeper client relationships.

e)Deepak Nitrite Standalone business: Ambition is for next 3-4 years top line to atleast double from what we are currently but on the bottom line growth will be more faster due to all the backward integration and debottleknecking we’re doing.

f)Our R&D team is ~103 employees of which 20-25 are PHds.

g)Deepak Phenolics saw 10% volume growth this quarter but realizations were low due to subdued demand this quarter whereas Deepak Nitrite saw no volume growth due to Nandesari plant but if it’s a normal quarter it would be 10% volume growth

h)There has been a product which has been stopped in Europe but we have started manufacturing and alongwith us there is only one player and we see strong demand on this product with our European customers going forward.

i)Externalities in this quarter: Moderation of Textile segment demand, Nandesari plant operations, Usage of Natural gas instead of coal for utility. 4 Cr is the delta due to usage of Natural gas instead of coal for a month.

j)Current environment: Demand is bullish, RM cost has normalized compared to Q1 but still high. Benzene, Tolurene and Xylene prices are way far away from crude prices and they are significantly high. Crude prices have been stabilized but its Petrochemical derivative prices are significantly high which is the RM for Deepak

k)Currently prices of Phenol are going slowly compared to prices of Petrochemicals like Benzene, Xylene and others.

l)Phenolics is dependent on domestic growth and you can say its bet on India’s GDP. India Phenolics is used in laminates, Agrochem, Pharma. India demand is not that fast as we anticipated but faster than other developed nations. Deepak Phenolics has capacity utilization is 100+

m)Phenol: Europe not a Net exporter due to high energy prices its not the supply which is impacted its also the demand because there is no consumption as well.

n)Outlook for remainder FY23: Deepak Orderbook is full and we expect some reduction in price in freight cost and moderation in energy price. Q3 and Q4 to be comparatively better than Q2.

o)CAPEX Plans

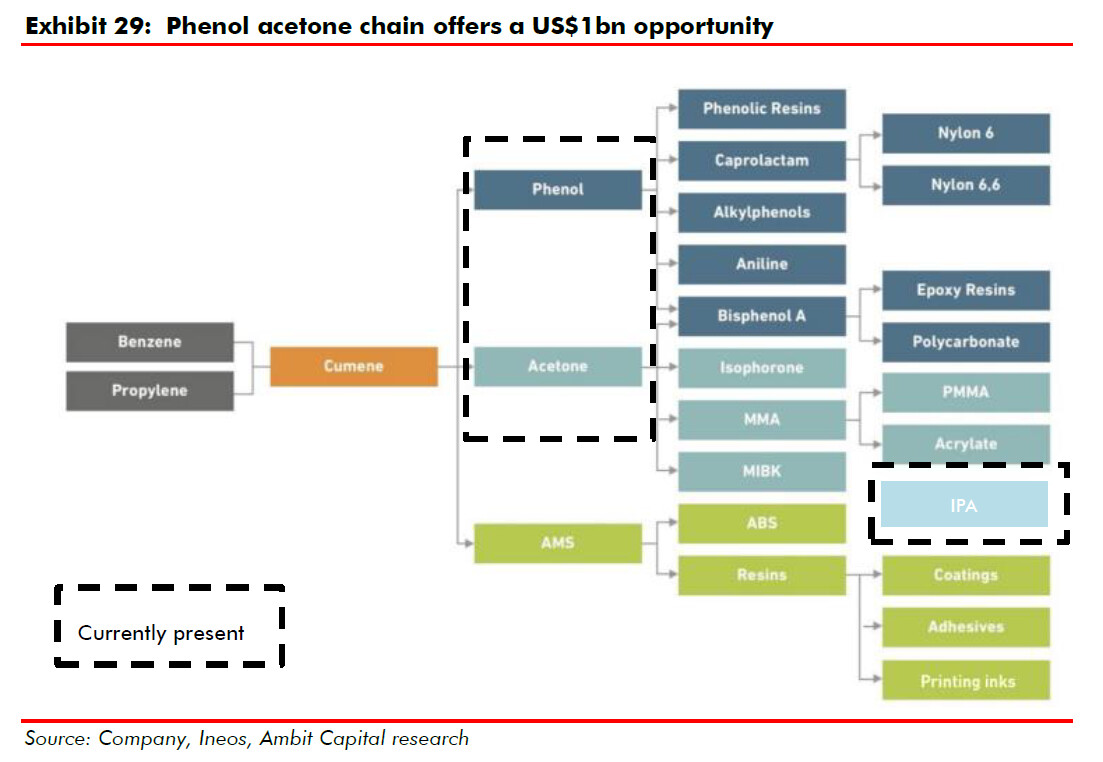

i)Deepak Chem: INR 1500 Crore investment where we are going into various derivatives of Phenol and Acetone and will go live in phase wise manner entirely by FY25.

ii) Working on developing basic engineering package for Pharma division which will be in the EBITDA range of 22-24% and this will be roughly generate revenue of roughly 500-600 Cr.

iii) Sultanate of Oman entity where we have 51% stake. The rationale behind this investment is to get cleaner and cheaper source of energy. We’re going to cater to our existing products like Sodium Nitrite per se which has energy not as Utility but as RM as well and this will target market like US where Oman has FTA and where we have deeper understanding of our customers/markets.

24 Likes

5 Likes

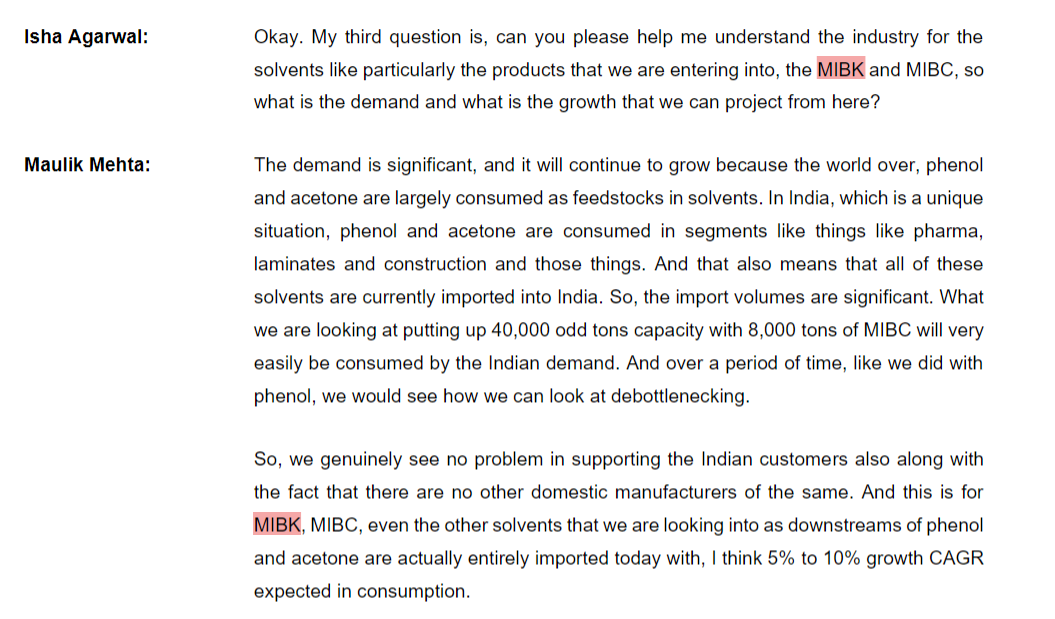

if possible please share the name of product.

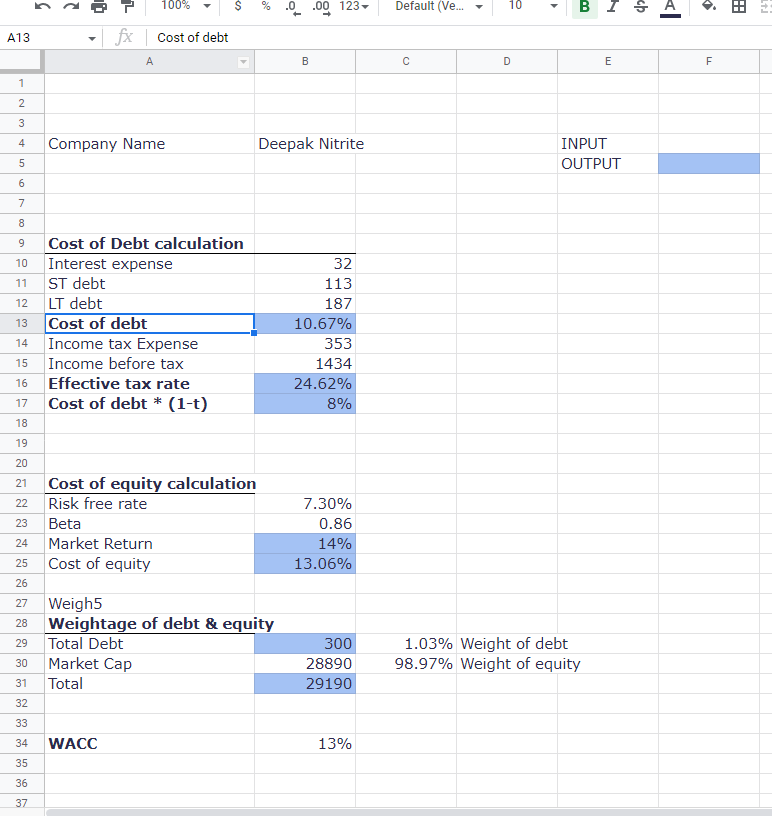

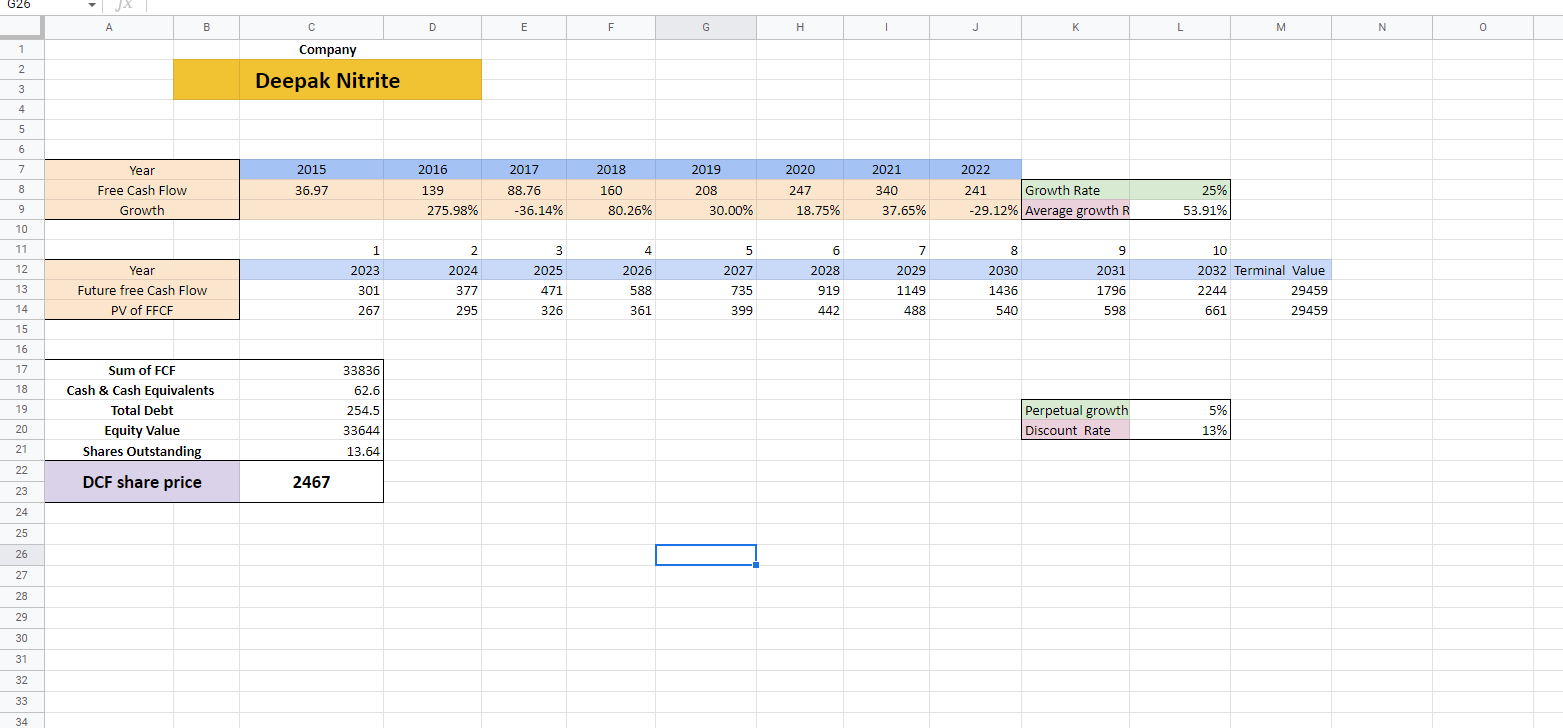

Did some Calculated DCF on Deepak. Market has priced Deepak Nitrite fairly. However, Upcoming Capex of 1500 crore can be big game changer if management executes with same track record.

8 Likes

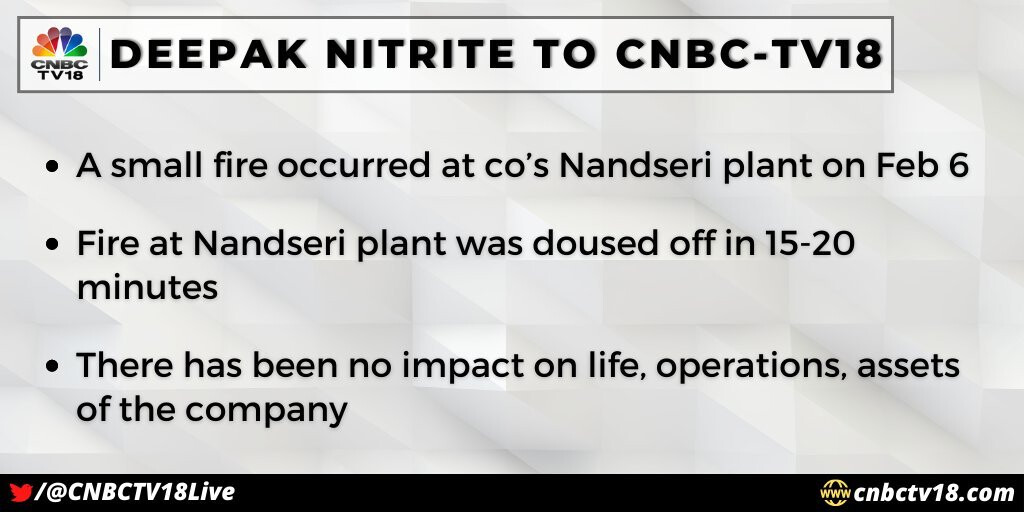

Insurance claim on loss due fire in their plant

1 Like

11 Likes

Noob question: If price of raw materials go down, is it not good for the company?

9 Likes

Inventory loss, if company have high inventory at higher price.

4 Likes

Thanks for the information. Lets see when they announce the capex

3 Likes

Second fire in last 6 months… ![]()

2 Likes

Hi can someone better help me understand the Clean Tech investment and subsidiary? It is 100% subsidiary and my understanding is that a majority of future capex is being done through it? Is there any particular reason for this?

1 Like

if RM price goes down then company cannot reduce the finished good price bcz they bought RM at higher cost. so they will be sitting at a lost if they sell at low cost. and if competitor bought RM at lower cost then they can sell finished good at lower cost also, so first company will lose business.

Hey, two questions

- Are we assuming that the company bought huge quantity of raw material at high cost or is there some way to verify that?

- Since raw material cost has reduced, the company can further buy RM at lower price and sell products with increased margin. Won’t this overcome the affect from point mentioned above?