Hi everyone,

The thread has been really insightful, thanks to everyone who contributed.

My viewpoints:

Management

I’m very impressed with the management, they seem to be ‘walking the talk’. Let me take a few instances which made me feel confident about the company:

-

In FY14, the management guided that for FWA, plant will take around 3 years to reach full utilization levels and breakeven and the management went on with the loss-making entity, turned it around completely in FY19 (yes, there was a delay) but to me, it shows that the management is capable of seeing the bigger picture and taking bold decisions.

And as luck would have it, FY20 was driven by PP (Performance Products)

-

In the annual report of 2016, they mentioned that in the long run, the Phenol and Acetone plants would be used for speciality chemicals and they seem to have executed this starting from Q1FY21 (with an opportunistic bet on IPA (Isopropyl Alcohol), which is in huge demand because of its use in sanitizers and also as a solvent in pharma industry)

-

In Dec’16, they said they expect to grow the specialty chem business at 15% CAGR for next 5 years and the results are not bad (12-13% till 2020). I wouldn’t necessarily cut their points for missing this target

I believe the management knows what they’re doing, have skin in the game, capitalizing on every opportunity they get and this decade is going to be a super interesting one

Having studied Vinati Organics before this, I find the management of Deepak Nitrite to be super-hungry (huge debt for expansion in Deepak Nitrite vs no-debt Vinati Organics), this does come with downside risks obviously

One thing which investors are betting on for Deepak Nitrite, except the whole transformation of chemical industry from West to East and the China Effect is the transformation from a commodity chemicals company to specialty chemicals company and a hopeful P/E re-rating

I was quite curious about the sources of future growth for DNL, so decided to dig a bit further:

Phenolics

Example 1: Isopropyl Alcohol (already started)

Raw Material required - Acetone

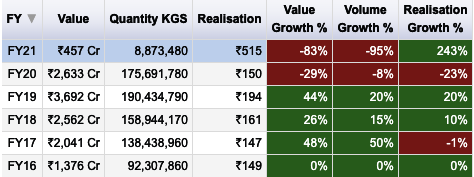

Deepak Nitrite recently setup a 30K MTPA plant and is doubling the capacity by Q3 FY21, so even if we normalize the current super-high price realization of IPA, it should be able to capture a decent % of demand as ‘import substitute’

From Acetone to IPA, what is heartening to see is that the company is moving towards value-added products and is competing in a big market (emphasis on change in realizations in the below table, although the increase in value added will not be equal to the exact difference of realizations, my point is that the company is ‘doing more of what it does’)

→

→

(Acetone Imports to India ) on the left and (Isopropyl Alcohol Imports to India) on the right

(Acetone imports link https://phreakonomics.in/export-import/micro-individual?startDate=2015-08-01&endDate=2020-08-01¤cy=inr&hscode_commodity=1639&type=imports&consolidation=fy)

(IPA imports link https://phreakonomics.in/export-import/micro-individual?startDate=2015-08-01&endDate=2020-08-01¤cy=inr&hscode_commodity=1542&type=imports&consolidation=fy)

A huge opportunity which DNL has with Phenolics, is to go downstream with more value added products

The below 2 examples were mentioned in their annual reports (as well as on their website) as potential products, so I just wanted to know more about them in case they decide to go ahead with this)

Example 2: Bisphenol A

Raw Material Required- Acetone, Phenol

Major Use cases include making polycarbonates (a hard, clear plastic) and epoxy resins

According to 2018 Annual Report, the local demand for BPA was ~80K MTPA and similar figure can also be obtained from the table below:

(BPA imports link https://phreakonomics.in/export-import/micro-individual?startDate=2015-08-01&endDate=2020-08-01¤cy=inr&hscode_commodity=9520&type=imports&consolidation=fy)

The good part seems to be Value-Addition + Big Market

(More about BPA here Bisphenol A market Size and Share | Industry Statistics – 2028)

Example 3: Methyl Isobutyl Ketone (MIBK)

RM- Acetone

Major Use cases are as solvent for manufacturing paints, as chemical intermediates and also used in semiconductor industry

According to Annual Report 2018, the local demand for MIBK was ~28K MTPA and as can also be seen from the data below, this also presents a good opportunity for the company (not as big as BPA or IPA but still)

(MIBK imports link https://phreakonomics.in/export-import/micro-individual?startDate=2015-08-01&endDate=2020-08-01¤cy=inr&hscode_commodity=1641&type=imports&consolidation=fy)

*Another potential product from their website which caught my eye was Polycarbonate, which again has Bisphenol A as its raw material (Now I might be getting carried away when Deepak has not even started with Bisphenol A )

This product also has a huge market size and is imported in vast quantities in India (also it seems like GAIL is interested in the space too https://www.chemanalyst.com/industry-report/india-polycarbonate-market-76)

(Source for all the above data is phreakonomics.in)

FSC

While FSC has pretty good EBIT margins (20-25%) and revenue growth has also been in the range of 12-13% CAGR for the past 5 years.

What I am unable to decipher is how much more revenue/what growth rate can be expected from this segment in the next few years and from where? (Since FSC caters to pharma and agrochem, both of which have tailwinds as of now, is there any visibility in terms of numbers?)

This segment seems a bit opaque to me and I do not understand this fully. If anyone can elaborate more on this, I’d be really thankful

Performance Products

a) DASDA

b) OBA

Vertical Integration:

Toluene → PNT → DASDA → OBA

Trying to understand the market size,

This gives us a rough estimate of DASDA global market~250M USD , out of which Deepak Nitrite has ~12.5% as mentioned. Deepak also has a majority market share in India.

What does the future look like in this segment? Exports? Because the global market seems to be pretty big as per these (north of $800 Million)

Optical Brighteners Market Share, Trend & Analysis Report, 2024.

https://www.globenewswire.com/news-release/2020/01/14/1970031/0/en/The-Global-Optical-Brighteners-Market-size-is-expected-to-reach-1-133-23-million-by-2025-rising-at-a-market-growth-of-6-17-CAGR-during-the-forecast-period.html

What exactly am I missing here?

Looking forward to hearing other’s views