Fair results coupled with strong CFO (3x+ of H1 PAT). I guess it’s last trench of trading inventory getting cleared up after winding up trading business. This is much needed cash which will go in expansion plans.

1 Like

Deepak Fertliser is the largest producer of ammonia in India.

The latest technology in the news is that-- Hydrogen fuel cell from ammonia. This will change the dynamics of the ammonia producers.

5 Likes

Company did a virtual analyst meet yesterday & gave a very comprehensive overview of all business segments.Well worth the time for interested people.

8 Likes

Listening to investor meet, we have a rich exposition of each vertical. I’d like to share my notes, and add on to what @phreakv6, @vishalprasad and @mrkakade have written about higher up in the thread, as more pieces of this story are fitting together.

Highlighting some of the questions asked above as a precursor to this post, please keep these in mind as I believe we have a definite answer for each of them.

-

What’s special about their chemicals/fertilizer?

-

Aside from cost savings, is there a strong logic to manufacturing ammonia?

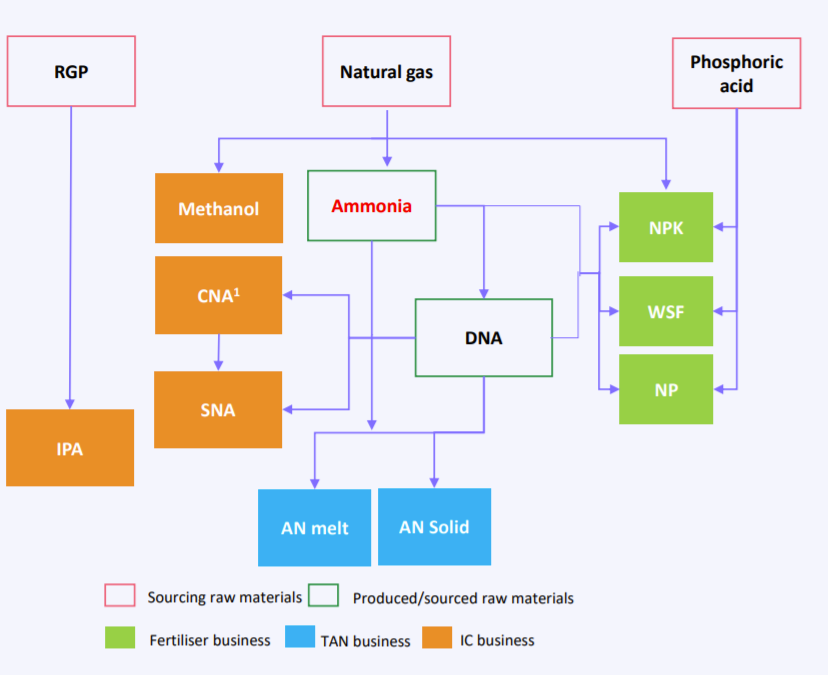

Value Chain

Management argues that their product offerings place them in a unique position relative to competitors.

- Domestic companies that produce ammonia are into fertilizers, not industrial chemicals.

- Domestic companies that produce TAN only produce it as a byproduct, or consume in house to make fertilizers.

- No producer of TAN produces their own ammonia at present/no plans for Capex at present.

This flow chart shows us that ammonia is central to their value chain, used in all three of their verticals. Dilute Nitric Acid is an intermediate compound, and TAN is produced downstream. Therefore, the ammonia capex will be utilised in house across all 3 verticals.

The Ammonium Nitrate Vertical:

They produce three forms of TAN. The first is an Ammonium Nitrate(AN) melt, the second is high density solids, and low density AN. Ultimately, all forms are used in making explosives for the mining industry.

Market landscape

Higher up in the thread, we realised this isn’t an import substitution play in ammonia, as DFPCL will use all the ammonia produced. However, what’s clear now is that this is a TAN import substitution play.

India is a net importer of TAN, with imports ranging from 200,000-300,000 TPA.

Current demand for TAN in India is 1,000,000 TPA, and is expected to be 1,200,000 TPA by the time DFPCL’s capex comes onstream. On capacity basis, DFPCL will produce 65% of India’s FY25E demand.

DFPCL says that cement industries that use limestone, and steel/power industries that use coal require TAN. While we may move away from coal power, as long as there’s spending on infrastructure, they see visbility for the next decade. Indeed, Ultratech is one of their clients.

- This outlook is corroborated by Solar Industries’ annual report, I will refer to both in future posts as the pair offer useful perspective of the industry.

Management’s take on entry barriers:

-

All 3 competitors they have in TAN right now are PSUs. These are companies like RCFL, and for these companies, Ammonium Nitrate melt is a byproduct that is sold, not a main vertical. They only have the capability to produce AN melt, and not of any other form.

-

Since AN is used in explosives, and after events like the Beirut explosion, government regulations on storing, handling, transporting ammonium nitrate are incredibly strict. Setting up a plant for a new entrant has high capital requirements, and no new player will be profitable in TAN unless they make their own ammonia.

On downstream opportunities and competitive advantages:

-

Clients blast the mines prior to excavation. This creates a huge amount of ash and rubble which needs to be cleared. Management’s claim is that DFPCL’s version of TAN/explosive that helps the customers in three ways:

- DFPCL’s TAN leads to better rock fragmentation, allowing for easier excavation.

- Ash/rocks need to be removed. If these broken rocks are large, clients need multiple expensive trips with the removal vehicle. DFPCL’s TAN leads to smaller, even rocks, allowing for a better fill factor for excavators, and fewer trips.

- Ultimately, these rocks are taken to crushers, which again are hindered by large rocks. If fragmentation is good, customers save money/generate higher margins with DFPCL’s products.

-

Secondly, they offer AI modelling of these blasts, providing a solution for their clients to choose exactly the right form/grade/quantity of TAN for their exact needs.

-

Explosive manufacturing - ANFO, Ammonium Nitrate Fuel Oil is a grade of explosive used worldwide, is a downstream product of TAN. Rather than supplying TAN and waiting for someone to create explosives, DFPCL is working on a number of products that utilize TAN to produce explosives.

Interestingly, management has given an explanation of how the three kinds of AN: HDAN solids, LDAN solids and AN melt work:

-

DFPCL currently has 4 production lines where these three forms are produced. The unique benefit DFPCL enjoys, is that they are completely fungible, and there is no fixed mix between the 3 produced. Depending on the end use of customers, they change the product mix to cater to market demand. If one quarter HDAN is in high demand, they can take advantage of this flexibility.

-

Different customers have different needs. AN melt comes with handling costs, needing heated tankers for moving, and is inconvenient for customers to store due to its explosive nature. In contrast, HDAN/LDAN solids are easier to transport, and LDAN forms the highest margins for DFPCL, catering to the limestone/infrastructure industry. PSU mining companies buy HDAN.

-

Solar Industries is an example that prefers AN melt. Whenever a client buys HDAN/LDAN solids, they first need to melt the solids before forming an explosive out of it. Therefore, some clients prefer the melt as they save on melting costs.

Finally, a key point to consider is that the new TAN plant will require DFPCL to import ammonia. Produced ammonia will be consumed in house on the west coast. Management says the economics of pipe linkages mean that it’s easier to import fresh ammonia on the east coast.

Economics of ammonia

The savings DFPCL makes with in house ammonia have been covered higher up on this thread. and will range from 600-2000 Cr. depending on the assumptions made. Here’s a lot more information about the way they’re going to get natural gas, and why the simple savings calculations we’ve all done based on natural gas spot prices are naive:

-

DFPCL will look for 10 year contracts on natural gas. These will be based on a basket of different underlying benchmarks, such as HenryHub. Crucially, HenryHub doesn’t index natural gas to crude prices.

-

People are usually concerned about natural gas prices looking at international prices. However, these are spot prices, some linked to crude, and long term contracts based on Brent/HenryHub do not have this kind of volatility. When spot prices move up 100%, long term contracts based on HenryHub only move 20% or so. It’s important not to extrapolate spot prices.

-

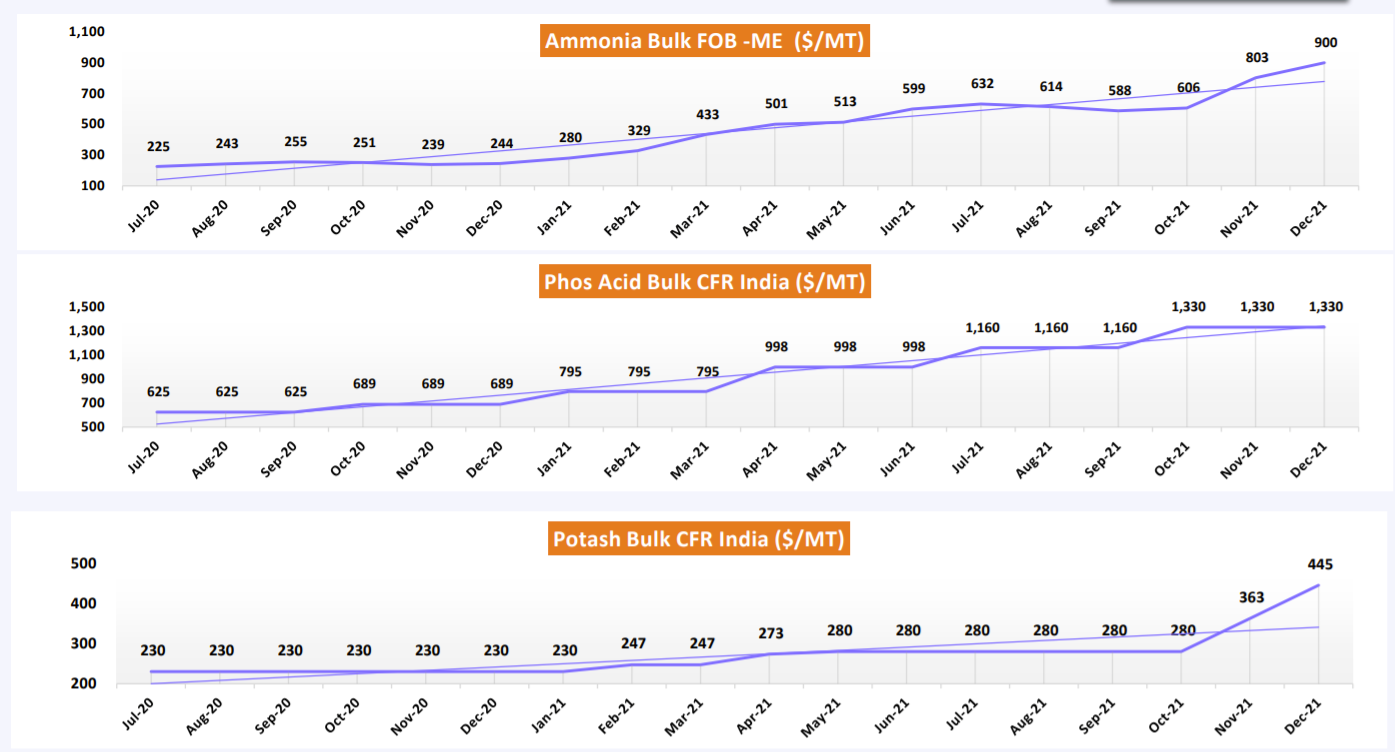

DFPCL’s most conservative savings models are built on ammonia prices being in the 10-15 year range of $400 per ton. Experts are predicting the cost of ammonia to reach $600-750 or more in the next two years. This has also played a role in the buy or make decision.

-

In discussion with 3-4 suppliers for this 10 year gas contract. Full supply is needed from March 2023.

-

Will recover 75% of the capex costs through GST subsidies over 10-15 years.

-

Margins not just of TAN, but nitric acid and fertilizer will improve from in house ammonia production.

Fertilizer Vertical

This is the vertical that requires more attention from investors.

Disasters between FY15-FY20:

- DFPCL’s fertilizer division went through enormous headwinds between 2015-2020. They used to receive subsidized natural gas from the central government, but this was then terminated on the grounds that the company was producing non-urea products. As a consequence, they had to halt production for a year, while this was fought in court. They ultimately won the judgement, but lost market share entirely, and had to restart using imported natural gas the following year. This was tied up in the courts until 2021.

A review from FY17’s annual report:

On top of this, they had to combat elevated prices in phosphoric acid, and a drought in Maharashtra.

All in all, here’s what their margins looked like from FY15-20:

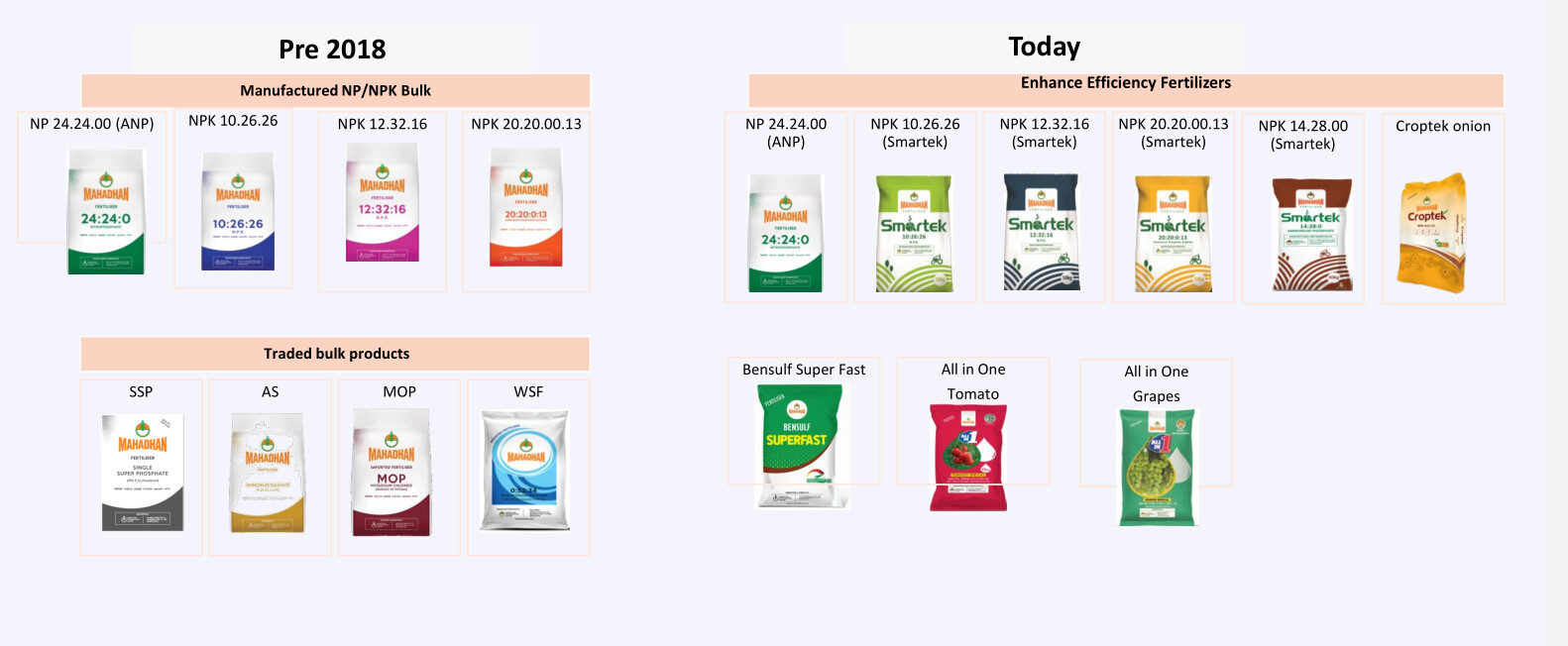

Following this, they chose to not compete in the bulk fertilizer space, but to invest in the Nitrogen Phosphorus Potassium (NPK) range. (The numbers on their fertilizer correspond to different mixes of these three. Eg: 12-32.16)

All in all it took 6 years for the turnaround opportunity written about in the titular post to play out:

As mentioned higher in the thread, they’ve done two things in the last three years.

- New speciality product offering

- Specific management hiring

Speciality Fertilizers

-

Introduction of Smartek and crop specific fertilizers. Were able to scale Smartek sales from 13kT in FY18 to 438kT in 2021.

- Smartek is based off technology from their partners in Australia. DFPCL has a ten year exclusive license to this technology. Contains a humic acid coating, which has multiple benefits for soil. Coromandel offers humic acid fertilizers, but not with the same nutrition profile.

-

Management’s claims are that they differentiate by nutrition use efficiency. “With Croptek, we’ve taken a complex route to forming a balanced nutrition fertilizer. Competitors have tried to add 1-2 micro nutrients, but no one else has been able to come up with the complete nutrition product with 8 nutrients. This is our unique offering”.

All of this happened on the back of key management changes. The person heading the fertilizer vertical is a Mr. Girdhar:

Upon closer inspection, there has been a significant amount of senior management hiring, Mr. Sailesh Mehta’s two children are both working at the TAN/Crop Nutrition division. The new head of the TAN division also has decades of experience with AN:

IPA and Nitric Acid Verticals

IPA

While IPA demand was higher due to covid, hand sanitizers only accounted for 10% of IPA demand, according to a report from IIFL. The balance was utilized by the pharma sector, which makes up some 75% of IPA demand in the country.

The investor meet revealed something interesting:

There are two routes to producing IPA: from propylene, and from acetone. DFPCL produces IPA via propylene, and Deepak Nitrite produces IPA via acetone. While IPA produced by acetone is cheaper (thus offering an advantage to Deepak Nitrite), DFPCL’s management explains that propylene based IPA is pharma grade due to a superior impurity profile, but propylene plants are expensive to make. Any future expansion on the IPA front will most likely be acetone based.

Nitric Acid

In my view, Nitric acid is the least interesting vertical at present. Nitric acid is mostly used in house, and DFPCL started a plant recently to cater to external demand. (80% is used in house, 20% is sold externally). The competitors in this segment are the same PSUs that produce TAN.

Since ammonia goes into nitric acid, external sales should benefit from the same margin expansion factors as TAN. What strikes me is that demand for nitric acid is driven by speciality chemicals - nitro aromatics, and demand for nitric acid is expected to outpace domestic production in 2026. Therefore, I would not be surprised if the next capex cycle includes more nitric acid production.

Until then, this is the least interesting vertical to me as they don’t have any plans at present to move downstream.

Summary from my notes:

-

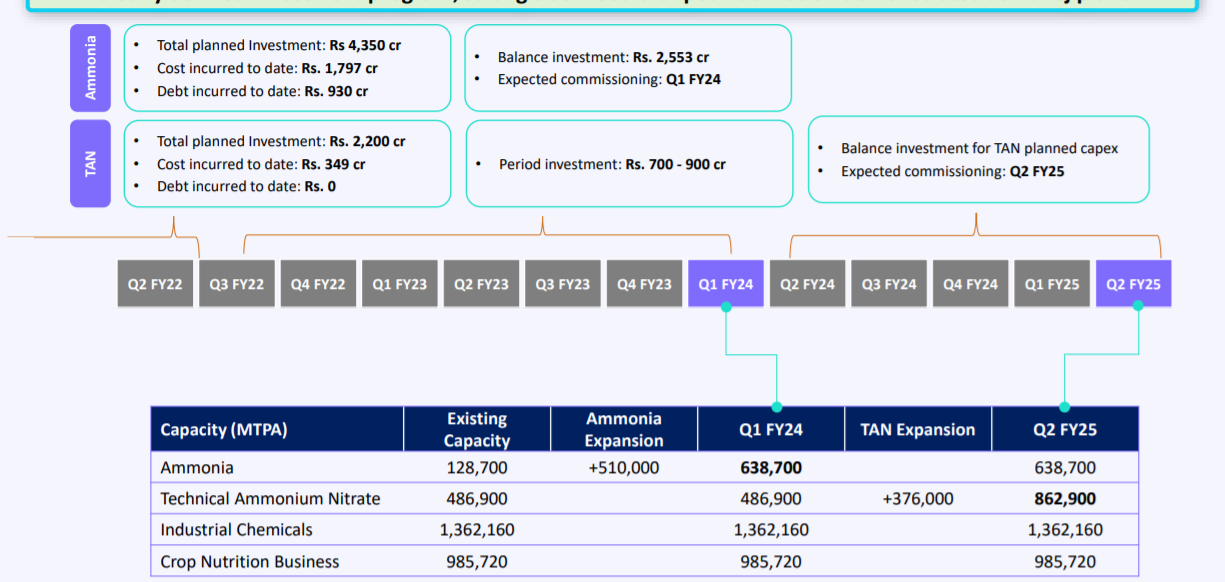

TAN expansion looks to be the most clear cut opportunity with entry barriers, downstream capabilities, and inefficient competitors. They’ve made a case for how their products are differentiated ie. speciality. However, margins need to be blended in our model as 3 out of 4 existing lines will use in house ammonia, and 1 line + new capex will still require ammonia.

-

Fertilizers have had a chequered past, they decided to take on capex after capex between FY15-20 despite the problems with natural gas supply. One has to ask if they’ve learnt their lessons from the 2014 fiasco in the new natural gas contracts. On the other hand, they did win the court case against the government, meaning this imposition was arbitrary from the government…

- Their claim of speciality fertilizer is based on yield rates and a complete nutritional profile, offering a clear differentiation to bulk fertilizers, and having more nutrients per grain than competitors.

-

This deserves attention, whether discounting phosphoric acid backward integration is the right move, given the shortages and problems in the past.

-

Their management hiring has been impressive in the last 3 years, and have lead to numerous changes behind the scenes. Out of all of them, Mr. Tarun Sinha, who runs the TAN division comes across very well in the interviews.

-

What I don’t understand fully is the interplay between fertilizer subsidies, and their strategy for margin expansion given farmers with limited purchasing power are the end user. Once I understand this, I will write a follow up.

Disclosure: Invested, have accumulated between November and December.

31 Likes

Nitric acid price rises due to increase demand from fertiliser. in Asia it was increasing till September. How we can track the price of nitric acid

If you read this article it is clear that during December 2020 the prices of Nitric acid in India was around $ 125 per MT.

The same is now at $ 423 per MT.

So clearly there is a huge increase.

In the interest of having accurate data points in this thread, and not posting random claims from twitter, could you please prove this claim about Deepak Fertilizer’s capacity expansion in Nitric acid?

As far as I’m aware from annual reports and investor presentations, there is no planned capex in nitric acid. They recently commissioned the plant at Dahej, and increase in volumes is from higher capacity utilization.

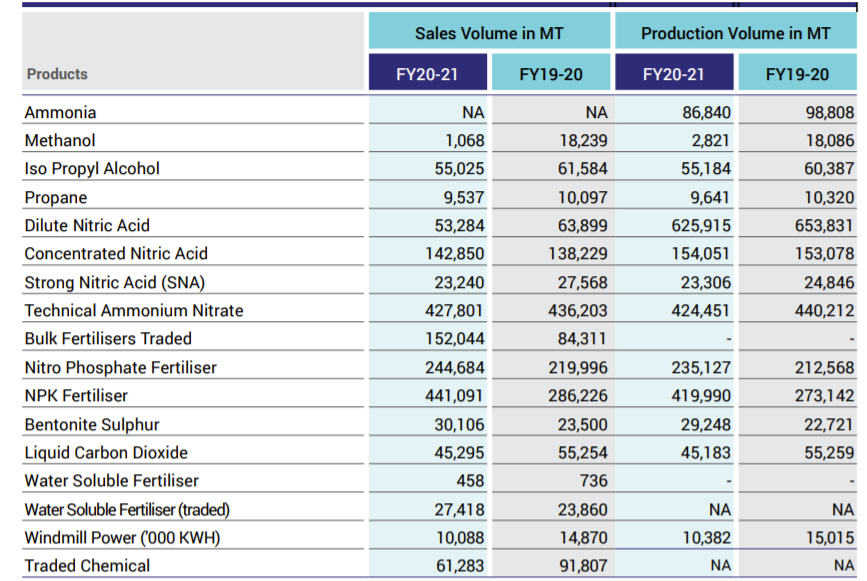

As you can see, a majority of DNA is consumed in house, and CNA volumes are similar to FY20.

Secondly, all communication hints at this quarter doing well because of TAN, not because of nitric acid.

-

Within the chemicals segment, TAN contributes 60% to the profits, Nitric acid contributes 20% to the profits (FY21).

-

Volumes in Q3FY22 were 6% higher in nitric acid, but TAN volumes were 24% higher (YoY).

-

The investor presentation says that the quarter has been a record quarter on TAN, and no comments on nitric acid.

10 Likes

Yes. TAN and Ammonia.

Can somone help understand Deepak’s sustainable advantage? Looks like the results are driven by raw material prices vs. value addition and they are present in fairly old-economy sectors? Some rerating could happen but don’t see this beyond that. Please correct me if I’m wrong ![]()

1 Like

Please read the thread, the discussion in the last 6 months has revolved around precisely these points.

3 Likes

I have found some more information about the competitive landscape.

Comments

-

RCF is investing in brownfield AN melt (not solid HDAN/LDAN) expansion. National Fertilizer has two lines of AN melt production, each is 119,000 tonnes. Currently only one line is in use. I’ve taken the full capacity here.

-

Chambal Fertilizer has decided to use excess ammonia in production of TAN. No details yet on product mix (AN melt or solids). This has been announced in Jan 2022, environment clearance has not been obtained yet.

-

Deepak Fertilizer will still enjoy the lion’s share of demand. The time between their capex coming online (Q2FY25) and Chambal Fertilizer’s capex coming online and achieving full utilization (2025+) should be the highest for their margins. As of now, none of the others are in TAN solids, TAN is still considered a byproduct for them.

-

This gives us more details to track, especially if Deepak’s/Chambal’s capex runs late. All data assumes 100% capacity utilization by all players. In reality, production is much lower. 700-800k tonnes were produced annually in between FY18-FY21.

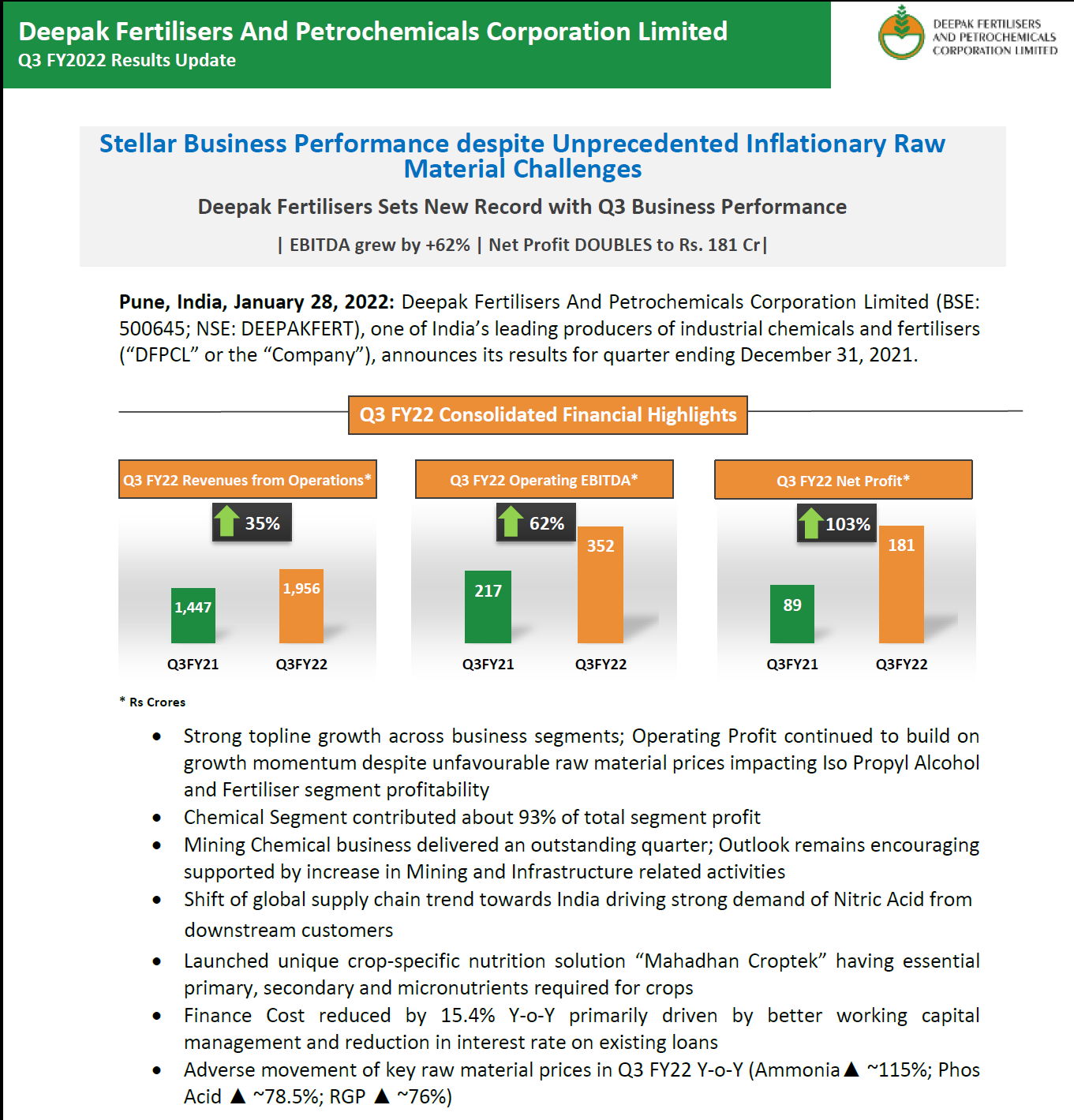

On the matter of Q3FY22’s results, I expect this to be the peak quarter for the chemical segment before the ammonia production comes onstream, and FY23 should see single digit topline growth in this segment. This is because of TAN running at 110% capacity utilisation. Further sales will come from inventory (if at all), and sale of lower margin products. Bottom line will change depending on margins (of TAN and Nitric acid), and whether fertilizers can recover to 10%+, and the effects any subsidies may have.

Inviting comments if anyone thinks this is conservative ![]() will write an update after the concall.

will write an update after the concall.

5 Likes

Chambal is also planning to launch a very big plant for TAN and dilute Nitric Acid. It will be completed in 3 years.

1 Like

Q3FY22 Concall Highlights

- Was a tough quarter, every single RM was elevated:

-

Company takes advantage of flexible manufacturing lines to optimise margins. HDAN volumes grew 32% YoY, LDAN grew 9% YoY. (No mention of AN melt)

-

Crop nutrition revenue grew 19.1%. Fertilizer profitability impacted by key RM price increases.

-

Nitric acid/IPA operated at 86-88% utilization.

-

NP/NPK plant was at 47% utilization due to low availability of RM, lots of headroom for growth.

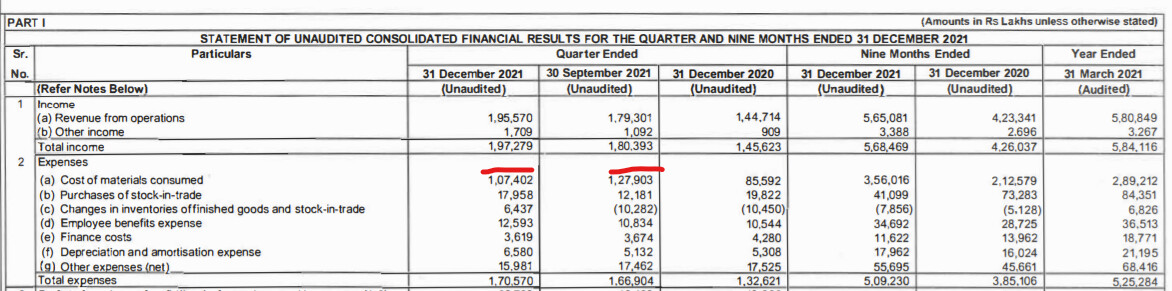

Q) If RM prices are higher, why is the cost of RM in the financial statements lower QoQ. (Great question)

A) Costs are elevated, but we bought a lower volume of RM overall (NPK plant’s utilisation), and the lower volumes lead to the costs optically looking lower.

Q) TAN realisations are some 80% higher, how sustainable is this trend?

A) Volumes overall went up due to demand, this lead to higher realisations. Secondly, while RM costs went up, we saw increases in finished good prices.

- International import prices of fertilizer grade ammonium nitrate went up.

- AN melt spot prices also went up as ammonia prices went up.

On sustainability of these margins: we’re moving downstream as explained in the investor meet. We’ve commenced our journey from product to solutions. Per tonne of TAN, we hope to garner better margins through this strategy, even as ammonia and TAN go through their cycles.

Q) How does one compare the propylene based IPA you make to the acetone based IPA Deepak Nitrite makes?

A) Both of these production paths have their own supply and demand cycles. For Deepak Nitrite, it’ll be based on acetone/phenol production, for us it’ll depend on the supply and demand of propylene. The delta between the two depends on these cycles, and there will be some periods where they have a better margin, some periods where we’ll have better margins. We’re working on specific target markets / captive use for products where margins will be higher. We are considering acetone based capex, but no announcements right now.

Q) Net/Gross Debt to date?

A) Reduced debt by 240 Cr. compared to March 2021. 2200 Cr. of gross debt, net debt is 1570 Cr. Will report balance sheet next quarter.

Q) What is the outlook for fertilizer margins going forward? Do we expect margins to stay stressed going forward? What kind of TAN margins going forward, when would it return to normalcy?

A) Million dollar question is when we expect RM prices/gas prices in EU to normalise. Movement in this would affect finished good products. Initiatives (like Croptek) taken in the last quarter will hopefully improve our margins in the medium term. We’re moving more and more into differentiated and value added products.

Q) Thoughts on Chambal’s TAN project, are we looking at a scenario of oversupply in 2025?

A) We have no understanding of the timeframe for this project, we are on track to bridge the demand as per our timetable. We don’t see a situation where the country will completely stop importing TAN. Even if this happens, we continue to export TAN to neighbouring countries, and new capacity is also coastal. We have the ability to export even in the instance of oversupply.

Q) Solar Industries guided volume growth of 15% in FY23. Do you see this on the ground?

A) Rehash of infrastructure uptick → demand.

- Within a financial year, TAN demand usually peaks in Q3 and Q4. Q2 has subdued demand.

- Without exceptional circumstances, capacity utilisation of >100% will be the norm.

All words are paraphrased, please check figures against official releases. Overall, the investor meet from two weeks ago was more useful for business insights than this quarter’s concall. A large number of responses were understandably rehashed. Highly recommend that to interested investors.

D: invested, biased.

18 Likes

Thank you for this thread, very insightful and built more of my conviction.

1 Like

Hi Guys,

A small doubt as an investor in Deepak Fertilisers, I wonder how any rise in interest rates would affect the balance sheet and the CAPEX?

When companies like Deepak go for such large Capex the interest rate on borrowing is fixed not floating. Therefore from a borrowing perspective deepak stands to benefit from rising interest rates.

2 Likes

Continuing the discussion from Deepak Fertilizers and Petrochemicals:

3 Likes

Coal India will complete the 3 year project in double the time with huge cost escalations. By the time coal will again be on the decline. Right now for Deepak gas prices will be the major worry.

Disc: Not invested,

Regards,

Raj

1 Like

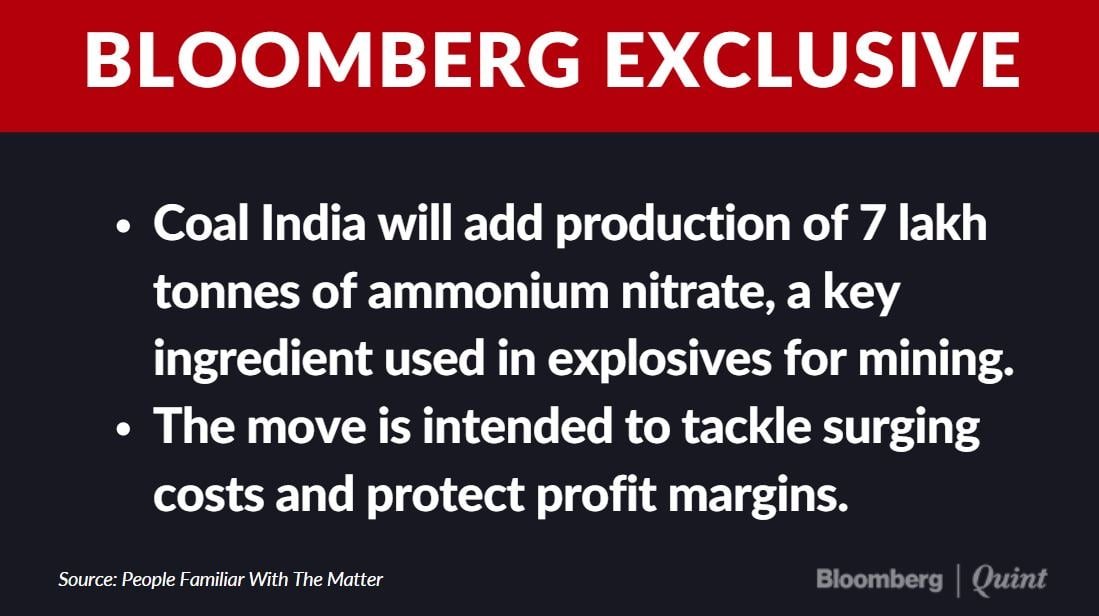

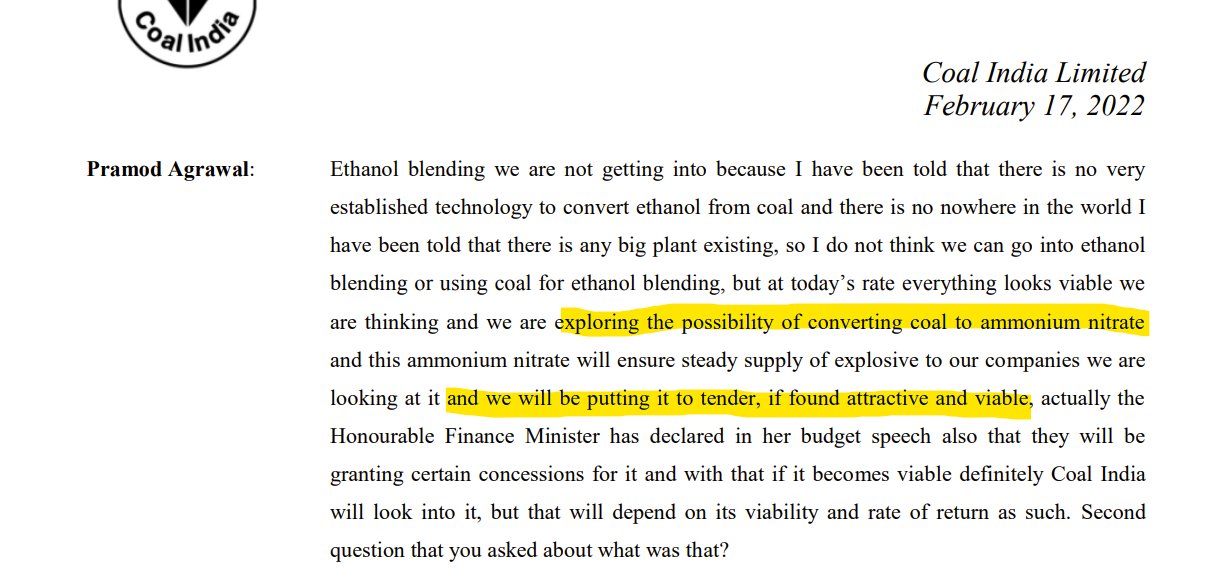

On the Bloomberg news, while they’ve made it look like this is breaking news, Coal India discussed this possibility in Q3’s concall:

This is likely. There are multiple steps and hoops that Coal India needs to jump through before this plant comes on stream. If a tender is floated in the next 6 months, it could take anywhere between 1-2 years for the tender to be awarded after various evaluation rounds. Then there’s the aspect of environment clearance, and the actual build time. I don’t think this will be a reality in the next four-five years atleast.

I’ve been tracking the various capex announcements from competitors, and when they’re expected to come onstream on this post:

While the gas/ammonia prices are high enough for the capex to be warranted, this comment from the investor meet stands out:

D: invested, no transactions in the last two months.

5 Likes

Spot prices are at crazy levels…in India even the government mandate prices are going to be multi fold to $7 / $11 from April/October 2022 from $1.79 few months back. Private parties are going to sell at mush higher rates. You can judge the quantum of rise yourself. Government revises prices every 6 months.

Fertilizers/Sanitaryware makers will be hit badly as they are major gas consumers.

Regards,

Raj

1 Like