Promoter Mr Mehta gave is monologue and then left the concal without bothering what other participants are asking and what the response is being given by CFO.

It gives a poor image of the management.

1 Like

Bharat Shah from ASK gave it back during the call, that when Mr Mehta sought answers or suggestions, we expected him to be there over the call. it really showed him in bad light and Mr Bharat Shah asked how can you expect investors to understand all the three verticals if the information shared is shallow.

5 Likes

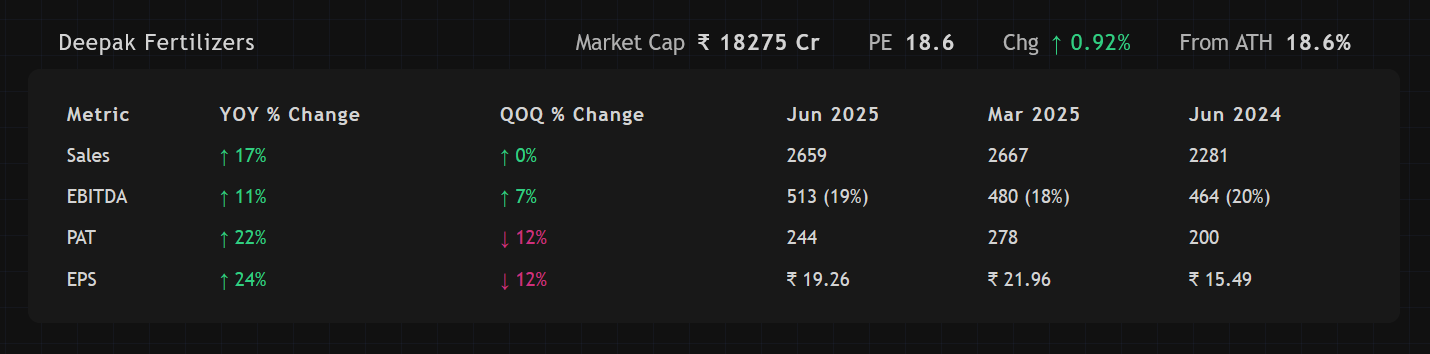

Q1 FY26

Performance

Concall Notes

- The company invested ₹377 crores in CAPEX during the quarter. Despite that the Net debt was reduced by over ₹225 crores, from ₹3,305 crores to ₹3,078 crores.

- Net Debt / EBITDA ratio improved to 1.5x from 1.72x in March '25.

- Fertilizer segment profit grew 125% YoY.

- Chemical segment profit declined 9% YoY due to pricing softness in IPA and ammonia.

-

Now, as many of you may know, ammonia contributes or constitutes almost 75% to 80% of our key chemical variable cost of production, 75% to 80%. Now ammonia has seen a volatility in the pricing right from, say, 10% to 200% over the last five Q1 quarters, if I might take it that way. And yet, our contribution margin in the downstream of our market determined key products, that is technical ammonium nitrogen acids has hovered around 40% plus, and our consolidated EBITDA margins have hovered around 18% to 20% over the last five Q1 quarters. Now what it tells very clearly in terms of these actual facts that the business model, the businesses have a very strong resilience and robustness, which is evident from some of these financial figures.

- The government has increased the export quota for TAN to 50,000 metric tonnes per year, allotted to Deepak as it is the sole exporter.

- The domestic TAN market is growing at 6-7% CAGR, while imports stand at 4 lakh tonnes, providing room for new domestic capacity.

- The company received a favorable ITAT order, deleting a tax demand of ₹581 crores and an expected penalty withdrawal of ₹479 crores.

- Early monsoon in Q1 FY26 impacted mining activities, leading to a 15% YoY decline in LDAN volume.

- The Gopalpur TAN project has 90% of total plant and machinery ordered. The Dahej acid project has 63% of total plant and machinery ordered. Both the projects are commissioning in Q4 FY '26.

- Total CAPEX spent so far on the new projects is roughly around ₹1,700 crores.

- Expansion projects at Gopalpur (TAN) and Dahej (Nitric Acid) are foundational to future growth and strength.

- The company acquired an additional 20% stake in its Australian subsidiary, Platinum Blasting Services, for ₹77 crores, increasing its holding to 85%. With the goal to accelerate growth and gain knowledge in advanced mining practices. The entity’s revenue was ~₹600 crores last year.

- The three core growth strategies are:

- Grow in areas of expertise (40 years of experience).

- Backward integration as a risk mitigator.

- Getting closer to the end consumer with tech-superior services.

- The company is pursuing a ‘total cost of operations’ model in the TAN business, which has been proven at a proof-of-concept stage and is now being scaled up.

- The journey from commodity to specialty continues, with almost 25% of the top line now emerging from this shift.

- The specialty shift has yielded price premiums of 15% to 40% over old commodity pricing.

-

Our plant OPE, OPE is operational efficiencies, have now improved from 78-odd percent to almost 86%, and some plants over 93% over the last five years of hard work. And as per global benchmarks, this sits in what they would call it as a very efficient operations category. So the manufacturing setup and facilities are also on a very strong wicket.

- Ammonia prices are expected to rise in H2 due to seasonal demand and plant restarts in Europe. China’s curbs have shifted supply sources for specialty fertilizers to Europe/Israel, increasing costs which have been passed on.

Risks & Concerns

- Ammonia price volatility remains a key variable, constituting 75-80% of key chemical variable costs. But management has successfully demonstrated the resilience of the business model.

- Pricing pressure in IPA and nitric acid is foreseen due to seasonal and inventory-led dynamics.

- Early monsoon impacted mining activities and LDAN offtake.

- Threat from Coal India’s proposed TAN plant.

-

So, today somebody might be thinking I will start from coal and produce ammonium nitrate. But that’s not the only thing. At some stage, people may realize that India has a deficit of many other chemicals, which can be produced through coal gasification process, which India is currently importing all those chemicals. So why you do that? So now all this is work in motion. I am not, of course, in any of those government committees. But I can definitely say this with some comfort and confidence that these things will be looked at by the government over a period of time as to how best to put this Indian coal to which kind of use. No point creating assets and products which we already have enough of, rather focus on producing things which we have deficit of. That’s where government will intervene at some stage is my view.

-

FII & DII Accumulating while Public is selling.

Disclaimer: Invested & Biased

6 Likes

With the coal gasification project a reality in 2030 for commercial production of ammonia nitrate for 6KMT will this have an impact on market dynamics of TAN

Can some chemical expert seniors please throw some light on this

Thank u in advance

Q2FY26

- Revenue 9% YOY, PAT 0% YOY.

- EBITDA Margin 15% vs 18% YOY. Q1 was 19%.

- Crop Nutrition

- 36% EBITDA growth YOY.

- Speciality Products (Croptek) 54% YOY growth.

- Speciality products now account for 28% of segment’s revenue vs 22% last year.

- Bulk fertilizers sales were down 31% YOY due to shortage in raw material.

- Outlook: Good season anticipated due to above normal monsoons.

- Mining Chemicals (TAN)

- TAN sales volume grew 29% YOY with full capacity utilization.

- LDAN volume was down 3% due to the monsoon.

- The B2C segment grew 33% YOY. Now contributes 14% of total revenue.

- Outlook: Strong post monsoon recovery is expected.

- Industrial Chemicals

- EBITDA declined 21% YOY due to margin pressure.

- Nitric Acid:

- Steady Volumes at 70 KT. Prices are expected to remain stable.

- Isopropyl Alcohol:

- Volumes flat at 17 KT.

- Margin severely impacted due to global oversupply, a steep drop in acetone prices and increase in US imports (due to tariffs).

- Outlook: Early signs of price stabilization are visible.

- Ammonia

- Challenging quarter due to global price volatility and operational constraints.

- FOB Middle East Ammonia prices dropped to an average of $300/MT.

- Margins were further impacted due to higher natural gas consumption and lower incentive income due to GST rate cuts.

- Outlook:

- Prices have already rebounded to above $400/MT.

- Planned shutdown in Q4 is expected to enhance capacity by ~10%.

- The LNG gas contract with Equinor will start in the middle of next year which will bring significant cost savings.

- Capex

- Gopalpur (TAN) 87% complete. Commissioning Q4FY26.

- Dahej (Nitric Acid) 70% complete. Commissioning Q4FY26.

- 3 years ramp-up for both to reach normal capacity utilization.

- Asset turns 0.5 - 0.6 for both plants. ROCE 20%+.

- Peak debt of ~4500 Cr by end of FY26.

- Completed acquisition of Australian subsidiary PBS.

- The acquisition was made at a valuation of 6.7x EBITDA and enterprise value of 537 Cr.

- Value added products contribute 22% of H1 revenue.

Disclaimer: Invested & Biased.

1 Like

Looking to the past track record , the 2 CAPEX are likely to get extended and will be commissioned in Q2 of next FY and its benefit will start coming from Q4 of next 2027 or Q1 of FY 2028. The stock is expected to consolidate for next 12-15 months and probably then we can see some improvement in earnings.

Margin trend for the last 11 years is as under :

13% 8% 9% 11% 6% 4% 7% 21% 14% 16% 17% 20% 18%

Margin seems to be reverting to mean and in case it reverts to the mean, Company has huge debt in its balance sheet. Company had been in past subject to downgrade in rating during 2019.

Company is into cyclical and commodity business and it will be interesting to see the cycle this time

Disclosure : Invested from lower levels of 450.

The company is trading at a Forward PE of 10-12 and Ammonia price is increasing.

Even overall Commodities prices are increasing.

Why will they keep this company at such low PE until all this happen till 2027?

1 Like

True. Ammonia price is now above 470 and close to 500…In concall also someone asked “what is driving the ammonia prices now? And do you think they are sustainable?” to which management answered that “Ammonia prices, in fact if somebody is looking 10-year average, it remained $450 higher up. So $300 was abnormality, I call it, that’s not the normal somebody should look in. So, it’s getting back to the right scenario, and that’s how it should be.”

2 Likes

The company has acquired 100% stake in an explosives manufacturer. Details not disclosed due to confidentiality.

Exchange Notification

How Deepak Fertilisers is gearing to detonate Solar Industries dominance

A Blasting Solution is an end-to-end service providing the bulk explosives, initiation systems, and engineering expertise required to fragment rock safely and efficiently. In simple terms, it involves engaging a specialist to break rock using controlled explosive energy.

The solution comprises the following key components:

Bulk Explosives

- TAN (Technical Ammonium Nitrate): The primary oxidizer. It is used to make ANFO (TAN + Fuel Oil) or dissolved to create the Emulsion Matrix.

- Emulsion Matrix: A stable mixture of oxidizer solution (TAN + Water), fuel oil, and emulsifiers. The matrix is non-explosive during transport.

- Sensitiser / Gassing Agent: A specialty chemical added to the matrix at the blast site. It creates microscopic gas bubbles that sensitize the emulsion, allowing it to detonate.

- Fuel Phase: Diesel or oil. In ANFO, it is soaked into the TAN. In Emulsions, it is chemically part of the matrix.

The Initiation System

- Detonator (Electric, Non-Electric or Electronic): A device that produces a high-energy shock wave to start the sequence.

- Cast Booster: A high-explosive charge that amplifies the detonator’s energy. It is required to initiate the main bulk explosive, which is often too stable to be set off by a detonator alone.

- Detonating Cord: A flexible cord containing a high-velocity explosive core, used to transmit detonation between charges or holes and to tie the blast pattern together.

A specialized truck (often called a Mobile Manufacturing Unit or MMU) transports these components to the mine site. Depending on the geology and water conditions, these components are mixed on-site to create ANFO (for dry ground), Emulsion (for wet ground) or a hybrid blend known as Heavy ANFO to optimize cost and energy.

Solar Industries is the leading player in Blasting Solutions in India. Its blasting solutions segment is operating at an ARR of 6000 - 7000 Cr with an EBITDA margin of 20 - 24%. It’s split between ~52% domestic & ~48% export. Domestic clients are primarily Coal India & other coal miners. It’s difficult for a new player to enter the market because of following reasons:

- Manufacturing and storing explosives requires strict licenses from PESO (Petroleum & Explosives Safety Organization). Obtaining these is a complex, time consuming process that deters new entrants.

- Explosives are dangerous to transport and expensive to handle. Crucially, the final explosive product has a shelf life of zero once mixed, meaning it cannot be transported after sensitization. To solve this, Solar Industries operates 30+ manufacturing plants strategically located near major mines and owns one of the largest fleets of MMU (Mobile Manufacturing Unit) trucks in the world.

While Australia has historically been the hub for its full-service model via Platinum Blasting Services, Deepak Fertilisers has successfully transitioned to an integrated ‘Blast-to-Cast’ service model in India. As of Q2 FY26, blasting solutions accounted for 14% of Mining Chemicals revenue, with a 33% year-on-year volume growth, signaling a definitive shift away from its legacy as a commodity TAN supplier toward becoming a specialized mining partner.

Manufacturing capabilities comparison of Platinum Blasting Services Vs Solar Industries

| Component | Platinum Blasting Services | Solar Industries |

|---|---|---|

| TAN | Sourced (Buys from Deepak) | Sourced (Buys from Deepak + Imports) |

| Emulsion Matrix | In-House | In-House |

| Sensitizer / Gassing Agent | Sourced | In-House |

| Detonator | Sourced | In-House |

| Cast Booster | Sourced | In-House |

| Detonating Cord | Sourced | In-House |

Deepak in India too has similar capabilities with advantage of in-house TAN.

Now the interesting part, check following timeline of events:

- On 5th November 2025, Deepak Fertilizers announced it has acquired the remaining stake to make Platinum Blasting Services a 100% wholly owned subsidiary.

- On 24th December 2025, Deepak Fertilizers announced an 100% acquisition of an explosives manufacturer. (Confidential at the moment & subject to completion of conditions)

- Gopalpur TAN plant with a capacity of 377k MTPA is ~87% complete and is expected to go live by Q4 FY26.

- The government has increased the export quota for TAN to 50,000 metric tonnes per year, allotted to Deepak as it is the sole exporter.

My guess is that this unknown explosive manufacturer will complete the final piece of the puzzle and will bring in capabilities that Deepak Fertilizers & Platinum Blasting Services lack. Current debt stands at 3402 Cr and as per Q2FY26, management guided for peak debt to be ~4500 Cr. Assuming 500 Cr for remaining Capex & H2 CFO of 800 Cr. Total Acquisition budget could be 4500 - 3402 - 500 + 800 - 80 (To acquire remaining PBS stake) - 160 (Interest) i.e ~1160 Cr.

With ~1160 Cr of acquisition budget, my guess would be Regenesis Industries.

Regenesis is a fully integrated manufacturer of the “Initiating Systems” suite, filling all the gaps in Deepak’s current portfolio (TAN + Emulsion).

- Detonators: Manufactures Electric and Electronic Detonators (Brand: Indra E-Det, Indra Excel).

- Cast Boosters: Manufactures Cast Boosters in-house (Brand: Indra Booster / Quality Tested Cast Booster).

- Detonating Cord: Manufactures Detonating Fuse (Brand: Highly Durable Detonating Fuse).

- PESO Licenses: Holds valid licenses for manufacturing and storage of all Class 1, 2, 3, and 6 explosives.

The 25th December announcement mentioned exporting “differentiated products” to Australia.

- Regenesis has a strategic agreement with Vikram Sarabhai Space Centre (VSSC) to manufacture detonators using NHN (Nickel Hydrazine Nitrate) technology. This is a Green Detonator technology (lead-free), which is a highly differentiated and value-added product suitable for strict environmental markets like Australia and Europe.

- This specific IP (Green Detonators) gives Deepak Mining a unique competitive advantage to supply its Australian subsidiary (Platinum Blasting Services) against giants like Solar Industries & Orica.

Regenesis is a mid-sized private entity (FY24 revenue of 703 Crore). Likely operates at 6-8% EBITDA margins (approx 42-46 Cr EBITDA) because it has to buy its raw material (TAN) from the market, likely from Deepak Fertilisers or imports. Deepak paid 6.7x EBITDA for Platinum Blasting Services. They can easily acquire Regenesis assuming 7x EBITDA multiple for 294 Cr - 322 Cr. Once Deepak integrates its own TAN supply, margins should expand from 6-8% to 18-20%.

Other candidates:

- SBL Energy: Having raised ~340 Cr in Series B funding in 2024 from marquee investors like Synergy Capital and Mukul Agrawal, they are likely on an IPO track. [Unlikely]

- IDL Explosives: This is a subsidiary of GOCL Corporation (Hinduja Group); it is unlikely the Hindujas would divest a core explosives asset to a competitor like Deepak unless it was a distressed sale, which the 13% CAGR does not suggest. [Unlikely]

- CDET Explosives: They have highest EBITDA Margins of all because they only focus on selling high tech detonators. They lack the complete initiation suite (Cast Boosters, Detonator Cord). On the contrary they fit in the acquisition budget and detonators are of much more value than cast boosters. So could be another potential candidate. [Likely]

- Special Blast: With revenue nearing 900-1000 Cr, they might be too expensive for a 100% buyout within Deepak’s current budget. Also they have limited footprint in Electronic Detonators. [Unlikely]

- Salvo Explosives: Similar to CDET, they specialize in detonators (Non Electric) but lack capabilities for cast boosters. They fit the acquisition budget too so could be another possible candidate. [Likely]

While CDET and Salvo offer attractive entry points into the high-margin detonator market, they are specialized component manufacturers. Regenesis Industries stands out as the most logical target for two critical reasons:

- Portfolio Completeness: It is the only mid-sized private player with an in-house “Initiation Suite” (Detonators, Cast Boosters, and Detonating Cords). This allows Deepak to provide a complete backward integrated blasting solution to Indian & Australian clients.

- The Green Advantage: Regenesis’s ties to NHN (Nickel Hydrazine Nitrate) technology provide a “differentiated product” that is essential for the Australian market’s strict environmental standards, a specific detail highlighted in Deepak’s December 24, 2025, disclosure.

Future Manufacturing capabilities comparison of Deepak Fertilizers (Platinum Blasting Services + Regenesis Industries) Vs Solar Industries

| Component | Deepak Fertilizers | Solar Industries |

|---|---|---|

| TAN | In-House | Sourced (Buys from Deepak + Imports) |

| Emulsion Matrix | In-House | In-House |

| Sensitizer / Gassing Agent | Sourced | In-House |

| Detonator | In-House | In-House |

| Cast Booster | In-House | In-House |

| Detonating Cord | In-House | In-House |

Based on my findings, TAN is 60% - 70% of the cost of providing blasting solutions. And Sensitizer / Gassing Agent which Deepak Fertilizer lacks is only ~2% of the cost. As they have the advantage of in-house TAN manufacturing over Solar Industries, they should be able to out bid Solar Industries or at least compete head on with them while maintaining high margins.

The Gopalpur TAN Plant is strategically located on India’s East Coast, serving as a high-speed maritime gateway to the Asia-Pacific. It reduces transit times to Australia by ~40% compared to traditional Black Sea supply routes. The plant’s location, coupled with a dedicated 4.8 km ammonia pipeline from Gopalpur Port, eliminates the logistics tax of inland transport. This allows Deepak to move TAN seamlessly to its Australian subsidiary (PBS) at a lower landed cost, creating a competitive moat against peers who lack such plant to port integration.

Market size estimate for Blasting Solutions:

- Indian market is estimated at 11,500 Cr - 13,500 Cr. Solar Industries is the market leader with approximately 25-30% market share. The remaining share is split between other organized players (like GOCL, IDL) and a significant unorganized sector.

- Australian market is estimated at 23,000 Cr - 27,000 Cr. It is an oligopoly dominated by two major players Orica and Dyno Nobel, who control over 80% of the market. Solar Industries has entered the Australian market as a challenger brand to compete on cost.

If Deepak Fertilizers is able to capture 25% of the Indian Market and 10% of the Australian Market, they can do an ARR of (2875 Cr - 3375 Cr) + (2300 Cr - 2700 Cr) = 5175 Cr - 6075 Cr.

Valuations:

We can use Solar Industries as reference. Current Market Cap: 115,000 Cr. FY26E revenue estimate from blasting solutions: 6500 Cr, Margin 22%, EBITDA 1430 Cr.

At EBITDA multiple of 20x, the blasting solutions business of Solar Industries is valued at 28,600 Cr.

Deepak Fertilizers current market cap for entire business: 15,697 Cr.

Disclaimer: Invested, biased and possibly daydreaming.

33 Likes

Very meaning ful analysis, however Solar valuation is mainly on account of exposure in defense sector and not Explosives alone.

1 Like

Yes, Solar commands a premium due to defence. That is why I am not using Solar’s entire business as reference which is valued at 56x EBITDA. Instead, I am stripping out the defence segment entirely. Solar’s Blasting Solutions segment should generate ~1,430 Cr in EBITDA in FY26. I am assigning 20x multiple to that to arrive at a valuation of 28,600 Cr. Even at 15x multiple, it’s valued at 21,450 Cr. Whereas Deepak Fertilizers current market cap for entire business is 15,697 Cr.

5 Likes

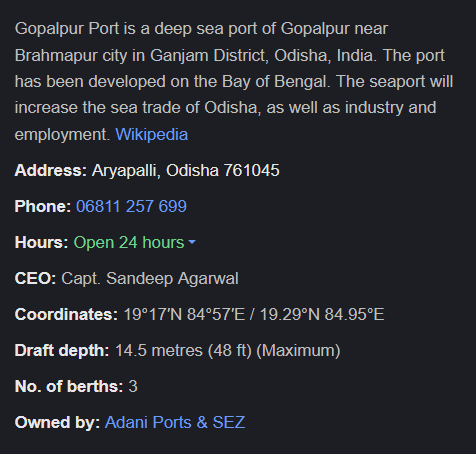

Excellent write-up. Thank you. Just wanted clarity. Gopalpur port appears to be a small one and does not do long-distance shipping to Australia.

1 Like

Historically it was a small port but things changed post Adani Ports acquisition. It is now classified as a deep sea port.

With a deep draft and multipurpose berths, the port efficiently handles the largest bulk carriers of Cape Size vessels with a draft of up to 14.5 m. The port has covered and open storage areas with an enormous capacity of 7.5 lakhs sq. m. Excellent cargo evacuation and receiving infrastructure support the smooth movement of cargo in and out of the port, demonstrating expertise in successfully handling oversized and overweight project cargoes as well. Mechanized import berth for faster turnaround of coal vessels.

Source: https://www.adaniports.com/ports-and-terminals/gopalpur-port

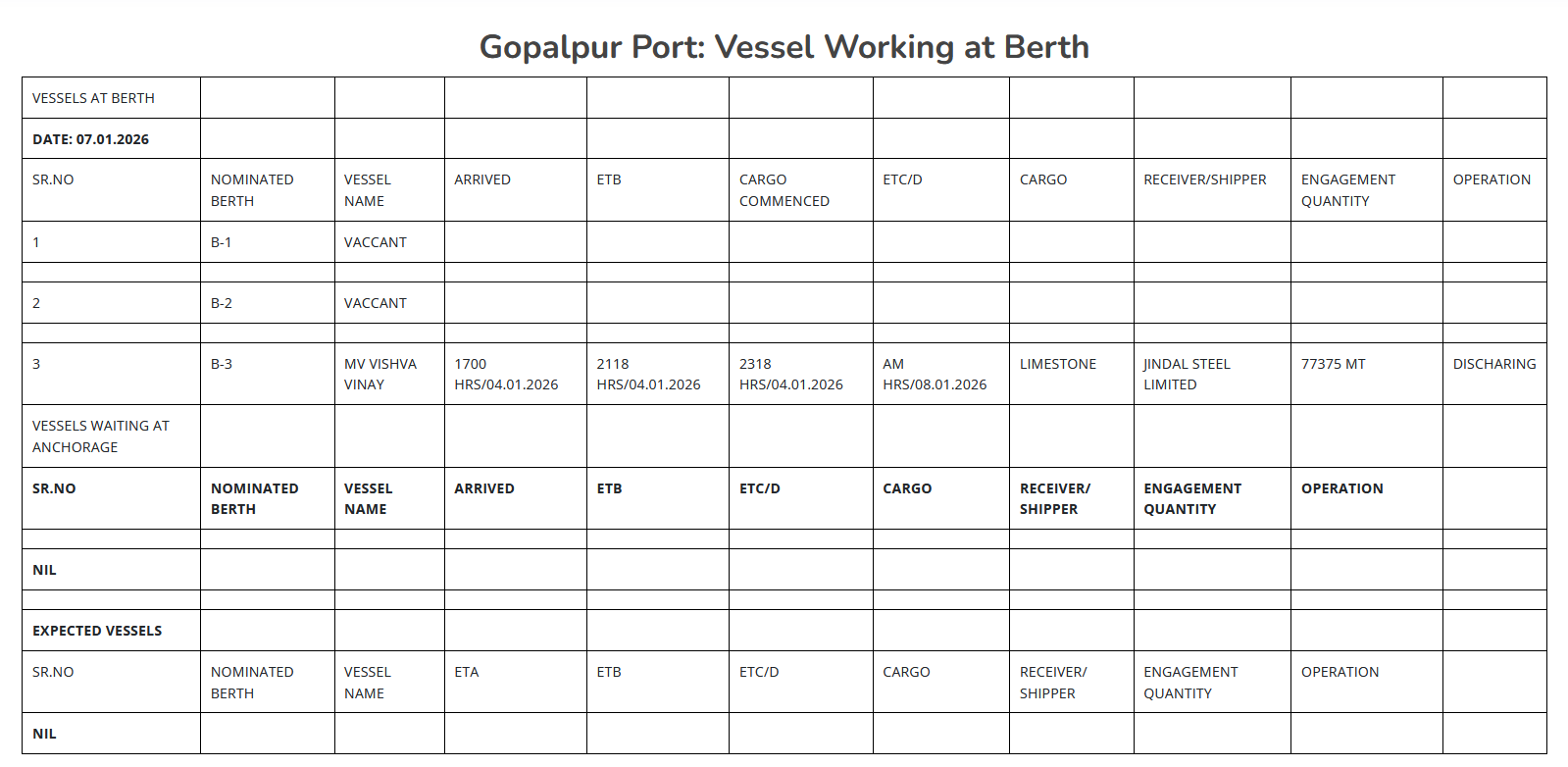

MV Vishva Vinay is a large bulk carrier. Recorded at Gopalpur Port discharging Limestone.

Furthermore, Adani also owns the North Queensland Export Terminal (NQXT) in Australia

APSEZ’s Board approved the acquisition of North Queensland Export Terminal (NQXT), Australia. NQXT is a critical export gateway for producers in resource-rich Queensland, Australia and has current capacity of 50 MTPA. APSEZ also signed a 30-year concession agreement to manage container terminal at Dar es Salaam Port, Tanzania

Deepak Fertilizers management commentary:

8 Likes

Excellent analysis, i read it 2 to 3 times to understand how they are shifting to clear value addition solutions in the Explosives segment, what kind of timeframe you forsee for it play out ? can we assume 3 years for them to reach 6000 Crores revenue in this segment alone

4 Likes

The Power of Ammonia: How the Equinor deal unlocks structural alpha for Deepak Fertilisers

Equinor deal is a 15 year Liquefied Natural Gas (LNG) supply (Volume: 0.65 Million Tonnes Per Annum) agreement between Deepak Fertilisers and Equinor (a Norwegian energy giant) starting May 2026. This gas will primarily serve as feedstock for Deepak’s Ammonia manufacturing plant, allowing them to replace expensive spot market gas with a stable, long-term supply.

Impact:

-

Without a long-term contract, chemical companies are forced to buy Spot LNG, which is typically linked to the JKM (Japan Korea Marker). In the last 1 year, JKM averaged ~$11.80/MMBtu, with landed costs in India often exceeding $13.00/MMBtu after adding shipping and regasification charges.

-

Long-term contracts from Western suppliers (like Equinor’s) are linked to Henry Hub (US Gas Price). The Henry Hub average for the last 1 year was $3.52/MMBtu. Even after adding liquefaction, shipping, and regasification costs, the estimated landed cost for Deepak is ~$9.00 - $9.50/MMBtu. We can use $9.25/MMBtu as average.

-

This creates a structural spread of ~$3.50 - $4.00 per MMBtu between Deepak’s contract price and the market spot price.

-

It takes ~34 MMBtu of natural gas to produce 1 Ton of Ammonia. (Based on standard industry benchmarks, IEA and Indian BEE Norms)

-

Cost Impact: A $3.50/MMBtu saving translates to: $3.50 * 34 = $119 per Ton of Ammonia

In the chemical industry, Gas isn’t just fuel, it’s the raw material. Because Deepak needs a massive 34 units of gas to make just 1 unit of Ammonia, a moderate drop in gas prices gets magnified into a ~$119 drop in production costs. This is the ‘Operating Leverage’ of the Equinor deal.

As a result this contract allows Deepak to produce Ammonia in-house at an estimated variable cost of ~$350 - $355/ton. This is significantly lower than the landed cost of imported Ammonia, which typically trades at ~$450 - $500/ton (CFR India).

-

Logic for Deepak’s cost:

- Gas = $9.25 (Avg. Price) * 34 = $314.5

- Conversion (Estimate cost of electricity to run the compressors, water treatment, and catalysts) = ~$35 - $40 per ton.

- Total Variable Cost for Deepak: $350 - $355

-

Logic for landed cost of imported Ammonia:

-

CFR Far East Asia: $528/ton

-

India typically pays slightly less than Far East Asia (Japan/Korea) because it is closer to the Middle East suppliers. If Far East is $528, India CFR is likely ~$450 - $500.

-

-

Savings for Deepak: Indian CFR of ($450-500) - Deepak’s Cost of ($350-355) = $100 - $145. This aligns with our ~$119 cost savings for Deepak per ton of Ammonia.

The Equinor 0.65 MTPA volume contract secures the majority of Deepak’s gas requirement. This prevents plant shutdowns caused by gas shortages or spot price spikes (where production becomes unviable). Running the ammonia plant at 100% utilization (vs. industry standard 80%) allows Deepak to spread fixed costs over maximum tonnage, further lowering the unit cost and freeing up cash flow that was previously tied up in working capital for spot purchases.

The true power of the Equinor deal is not just that it makes Ammonia cheaper, but that Ammonia is the “Mother Chemical” for nearly every product Deepak sells.

We can compute how much benefit it will have on major products of Deepak.

Nitric Acid

The transformation of Ammonia (NH3) into Nitric Acid (HNO3) occurs via the Ostwald Process. The overall net reaction is: NH3 + 2(O2) → HNO3 + H2O

Molecular weights:

- Ammonia (NH3): 14+(3*1) = 17 g/mol

- Nitric Acid (HNO3): 1+14+(3*16) = 63 g/mol

In a perfect lab with 100% yield, to make 63 tons of Nitric Acid, we theoretically need 17 tons of Ammonia i.e 17/63 = 0.2698 Tons of Ammonia

However Real chemical plants are not 100% efficient. In the Ostwald process, efficiency losses occur due to side reactions & absorption losses. Standard modern plants operate at ~94% - 96% Efficiency. So 0.2698 * 1.06 = 0.2859

Therefore, we require 0.286 Tons of Ammonia to make 1 Ton of Nitric Acid.

Cost Savings: 0.286 (Intensity) * $119 (Ammonia Savings) = $34.03 savings per Ton of Nitric Acid

Since Nitric Acid is typically $350-$450/ton, a $34.03 cost reduction drives a 7.5% to 9.7% structural EBITDA margin expansion.

TAN

To make 1 Ton of Ammonium Nitrate, we need two ingredients:

- Ammonia (NH3)

- Nitric Acid (HNO3)

The chemical reaction is: HNO3 (Nitric Acid) + NH3(Ammonia) → NH4NO3 (TAN)

Molecular Weights:

- Ammonia (NH3): 14+(3*1) = 17

- Nitric Acid (HNO3): 1+14+(3*16) = 63

- TAN (NH4NO3): 14+4+14+48 = 80

To make 80 units of TAN, we need 17 units of Ammonia (Ammonia per Ton TAN = 17/80 = 0.2125 Tons) and 63 units of Nitric Acid (Nitric Acid per Ton TAN = 63/80 = 0.7875 Tons)

But Nitric Acid itself is made from Ammonia and we previously computed we require 0.29 Tons of Ammonia to make 1 Ton of Nitric Acid.

Total ammonia required = 0.2125 (From Ammonia) + 0.228375 (From Nitric Acid 0.7875 * 0.29) = 0.441 Tons of Ammonia.

Therefore, we require 0.441 Tons of Ammonia to make 1 Ton of TAN.

Cost Savings: 0.441 (Intensity) * $119 (Ammonia Savings) = $52.48 savings per Ton of TAN

TAN typically trades in the Indian spot market at ~$650-$750/ton. As per my estimates, Deepak’s blended realization is ~$500-550/ton (lower due to bulk contracts), a $52/ton cost reduction drives a 9.5% to 10.5% structural EBITDA margin expansion.

Fertilizers (NPK)

For Deepak Fertilisers, the flagship bulk fertilizer is Mahadhan NP 24:24:0 (Nitro Phosphate).

Since Deepak produces this via the Nitrophosphate Route (attacking phosphate rock with Nitric Acid), we can derive the Ammonia intensity based on the Total Nitrogen content.

In Mahadhan 24:24:0, 1st Number (24) is % of Nitrogen, 2nd Number (24) is % of Phosphorus, 3rd Number (0) is % of Potassium.

It means 24% of the fertilizer’s total weight is pure Nitrogen. 1 Ton of Fertilizer * 24% = 0.24 Tons of Nitrogen

In the Nitrophosphate route, all Nitrogen in the final product whether added directly as Ammonia or indirectly via Nitric Acid originates from Ammonia feedstock. Therefore, we can calculate the total Ammonia requirement directly from the Nitrogen percentage.

Molecular weights:

- Nitrogen (N) = 14

- Ammonia (NH3) = 17

To get 1 unit of Nitrogen, we need 17/14 = 1.214 units of Ammonia.

Therefore, 0.24 Tons of Nitrogen * 1.214 (Ammonia Factor) = 0.291 Tons of Ammonia

Fertilizer granulation and rock phosphate acidulation are complex processes with some nitrogen losses (volatilization). Adding a standard 3 to 5% loss buffer: 0.291 * 1.05 = 0.306 Tons

Therefore, we require 0.306 Tons of Ammonia to make 1 Ton of NP 24:24:0 Fertilizer.

Cost Savings: 0.306 (Intensity) * $119 (Ammonia Savings) = $36.41 savings per Ton of Fertilizer

Fertilizer margins are volume driven. On a volume of ~1 Million Tons, a $36.41/ton saving adds roughly $36.41 Million (INR 328 Crores) directly to the bottom line, purely from the gas arbitrage.

Disclaimer: Invested & Extremely Biased. I believe in the operating leverage but the market can be irrational longer than I can remain solvent.

@bajji_s I am working on the model. Will share it once ready.

29 Likes

Disclaimer: Invested & Extremely Biased. Since management guards segment level EBITDA margins like nuclear launch codes, this is an exercise in reverse engineering, not clairvoyance. I might be directionally right or I might be hallucinating. Please consume with a generous bucket of salt.

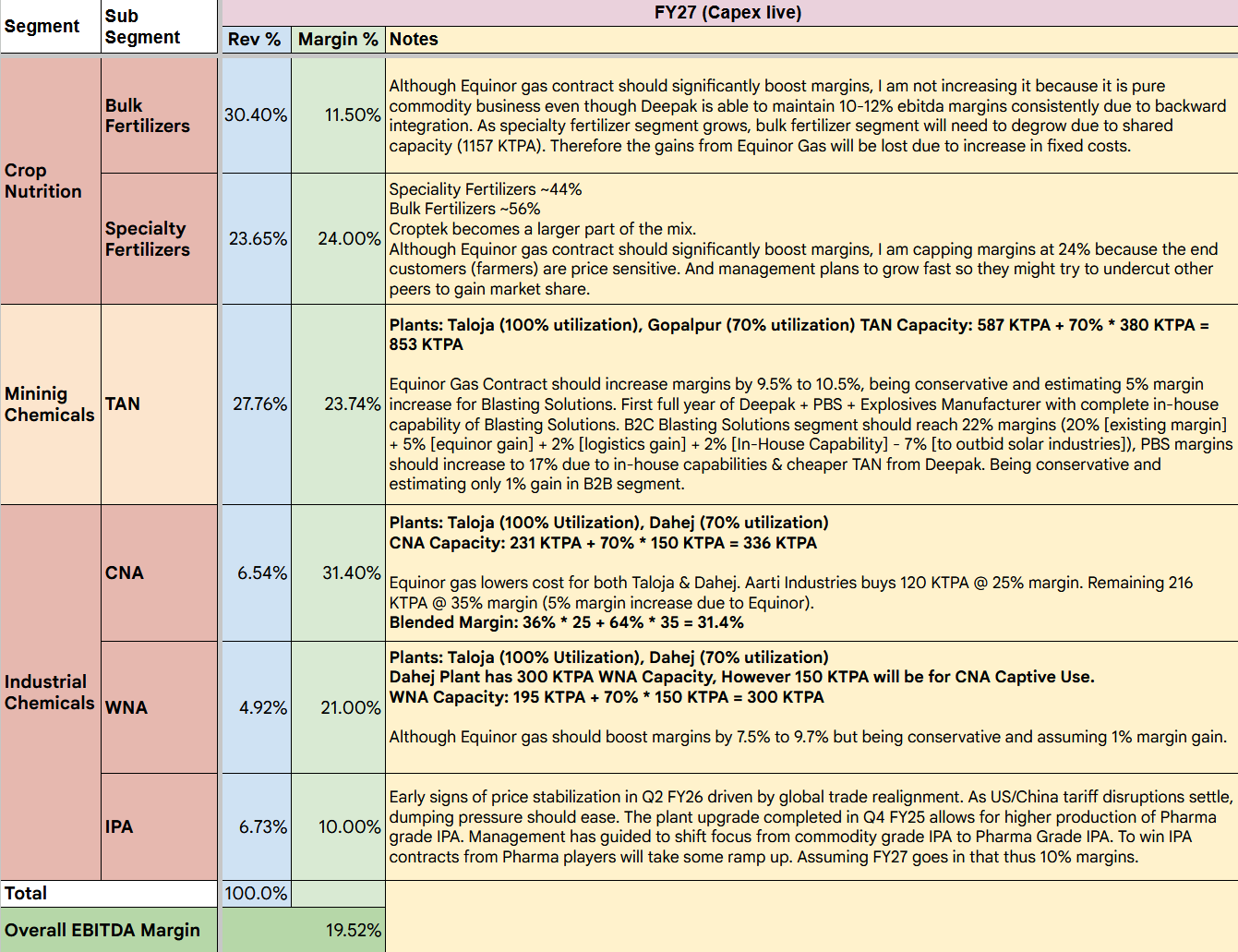

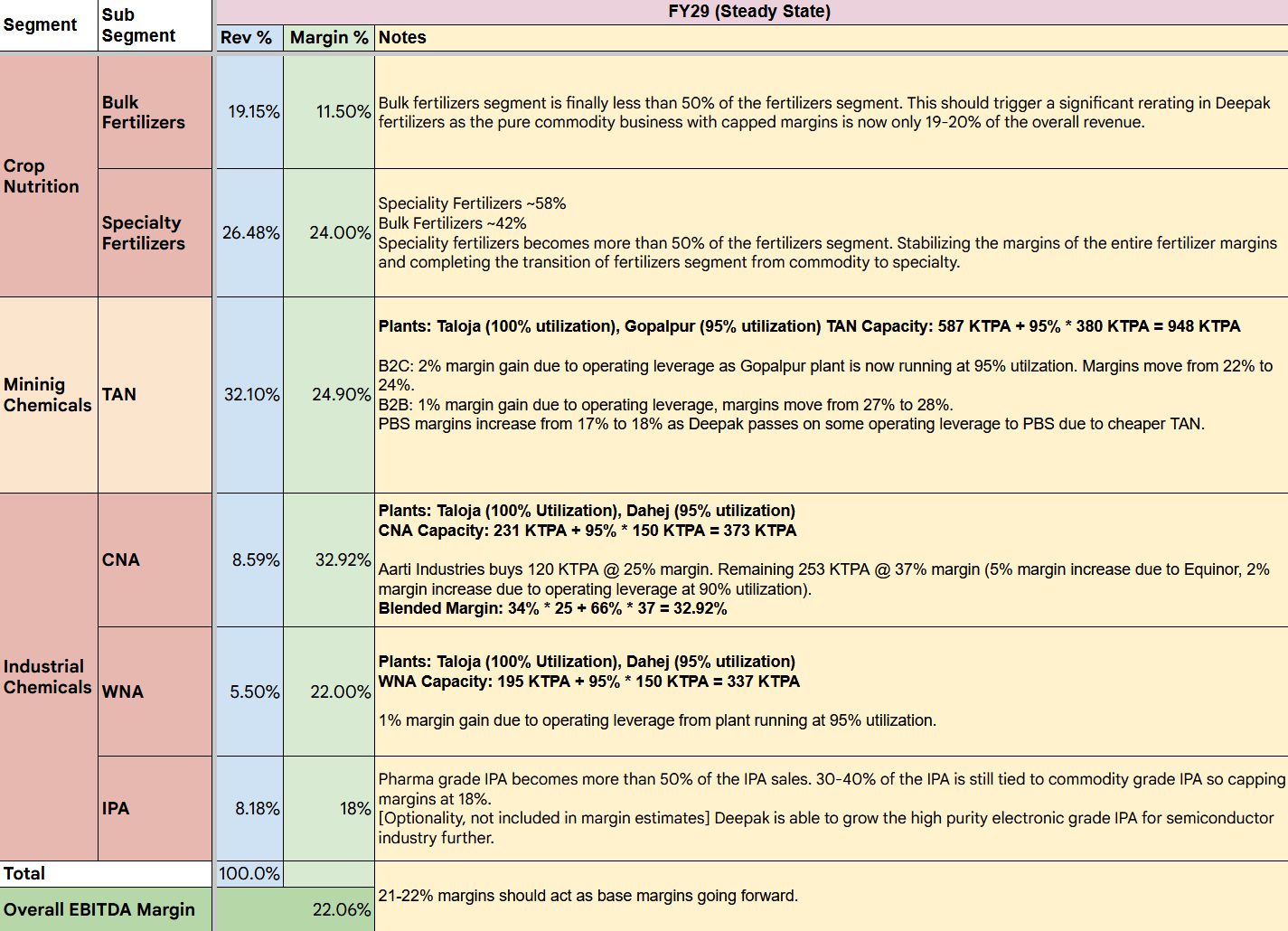

Deepak fertilizers transition from commodity to specialty:

FY26

FY27

FY28

FY29

The above numbers do not include the unknown explosives manufacturer that they have bought. My estimate is by FY29, it should contribute 100-200 Cr of EBITDA. I have also excluded the ‘other’ segment which includes traded chemicals & fertilizers and real estate business.

Overall revenue from FY26 to FY29 will grow at a CAGR of ~13% and EBITDA will grow at a CAGR of 21%.

Excluding bulk fertilizers segment, revenue from FY26 to FY29 will grow at a CAGR of ~23% and EBITDA will grow at a CAGR of 28%.

Current Market Cap: 15,150 Cr

FY29 EBITDA based on my calculations comes to 3385 Cr. At 15x multiple, we get 50,775 market cap. At 20x multiple, we get 67,700 Market Cap.

12 Likes

These numbers are based on avg Ammonia price of 500$ over next 3 years?

Ammonia price volatility doesn’t matter to the model. I can infact argue that the rising Ammonia price is good for Deepak.

- They have 510 KTPA ammonia plant at Taloja which meets 100% of the captive Ammonia requirements of Taloja (TAN, CNA, WNA, Fertilizers). Equinor gas contract will further boost margins as explained earlier.

- In the Indian market, the price of TAN and Nitric Acid typically tracks the cost of imported ammonia. If price of Ammonia rises, Deepak’s margin will increase further because peers will have to buy costly Ammonia from market whereas Deepak will continue producing Ammonia in-house at cheaper rates. Their cost remains flat while market realizations go up.

- Approximately 65% of the new 150 KTPA CNA capacity in Dahej is tied under the Aarti Industries contract. The contract is formula based, meaning any volatility in raw materials like ammonia or gas is passed through.

- For remaining Dahej CNA capacity & WNA capacity, they can transport Ammonia from Taloja to Dahej as they are ~350-400 km apart, making internal road tanker transfers cheaper compared to importing spot ammonia. They can also do Ammonia swaps i.e selling Ammonia to a producer in Taloja and buy Ammonia from the same producer in Dahej to save on transport cost.

- For Gopalpur TAN they will have to buy Ammonia from market but the shift to B2C Blasting solutions is the key here as blasting solution contracts are long term contracts with pass through cost for Ammonia. For B2B TAN, they gain ebitda margins as they won’t need to pay costly freight of transporting TAN from West to East. That should take care of any rise in Ammonia price volatility.

3 Likes

@r8b8 Can you give your viewpoint on expected listing, in the forthcoming years, of the demerged entities and how it can benefit the existing shareholders?

My understanding is that the existing shareholders would not get anything as they will only be the owners of the holding company stock.

Expected Listing Timeline

Listings of demerged entities (MAL and DMSL) are not immediate but anticipated in forthcoming years (2026-2027+) once stabilized, per chairman’s remarks on “unwinding each business into separate corporate entities” and historical “opportune time” guidance. Expansions like Gopalpur TAN (H2 FY26) and Dahej Nitric Acid must ramp up first for valuation appeal. No direct share issuance to DFPCL shareholders; benefits flow via holding company value