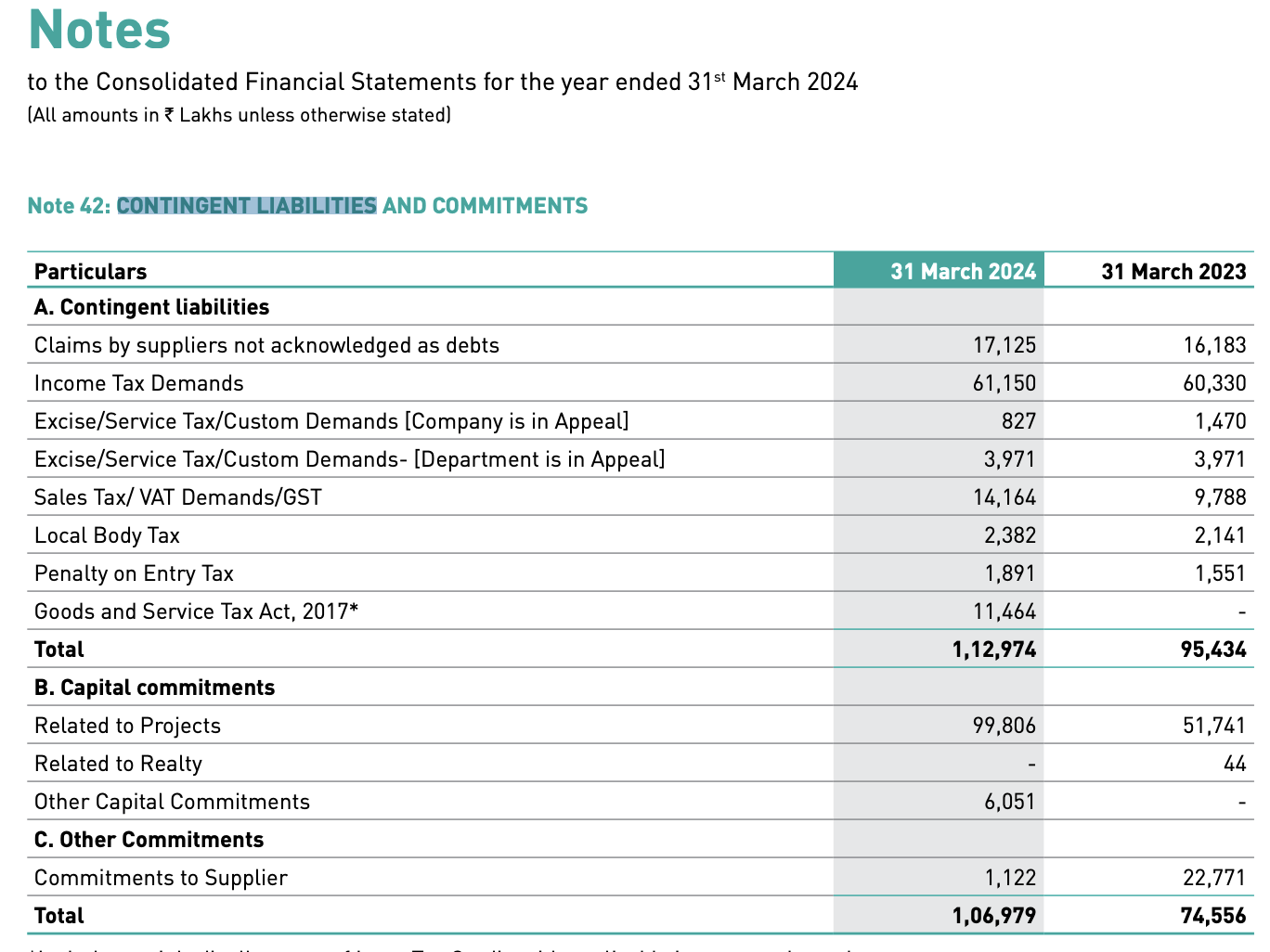

The Contingent liability seems to be on a higher side on a consolidated basis.Your view on this

2 Likes

Mainly IT/GST demands which seemed usual from Fy23 too.

Capital commitments related to projects also seem fine to me. Infact, commitments to supplier seems to have dropped which is good sign.

1 Like

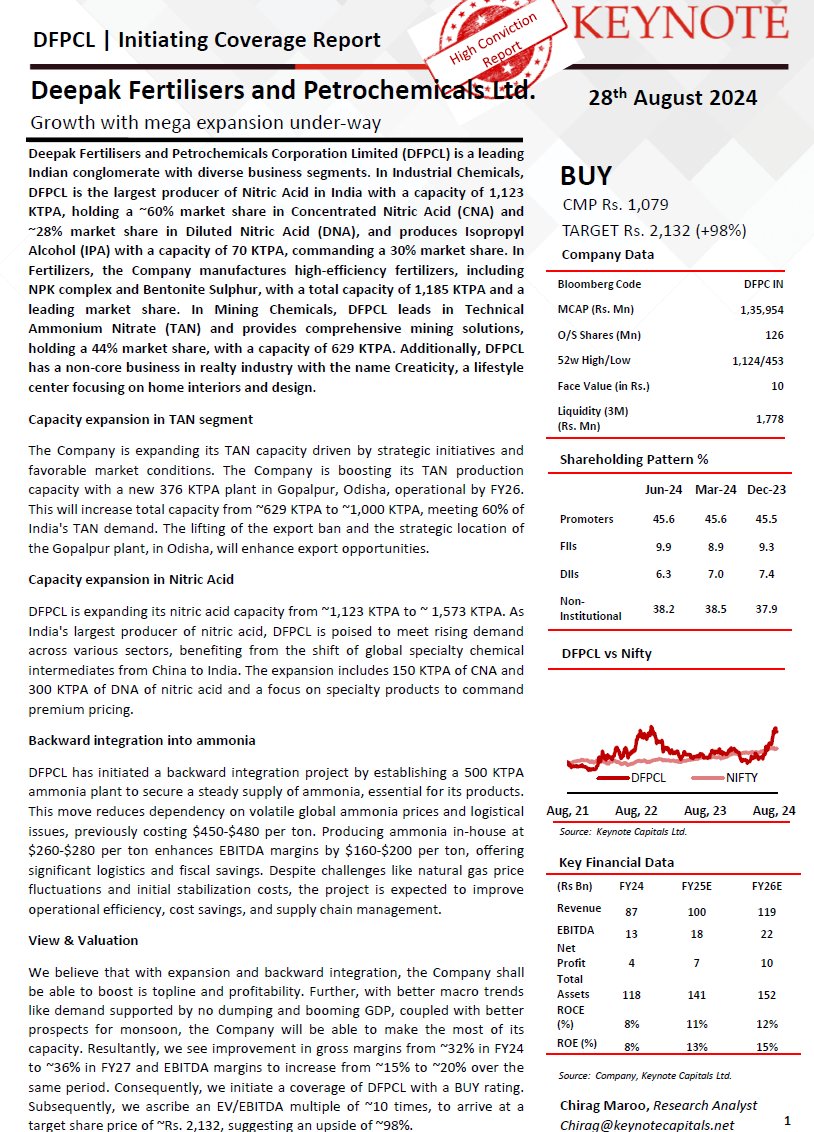

Keynote has given Target of 2132 for Deepak Fertilizers, +98% Upside

Keynote_initiating_coverage_on_Deepak_Fertilisers_and_Petrochemicals.pdf (1.7 MB)

"The company is well-positioned to drive growth in both revenue and profitability. Additionally, it will capitalize on increased capacity utilization, supported by favorable macroeconomic conditions. Strong demand, bolstered by the absence of import dumping and a growing GDP, coupled with positive monsoon forecasts, will further enhance the company’s prospects.

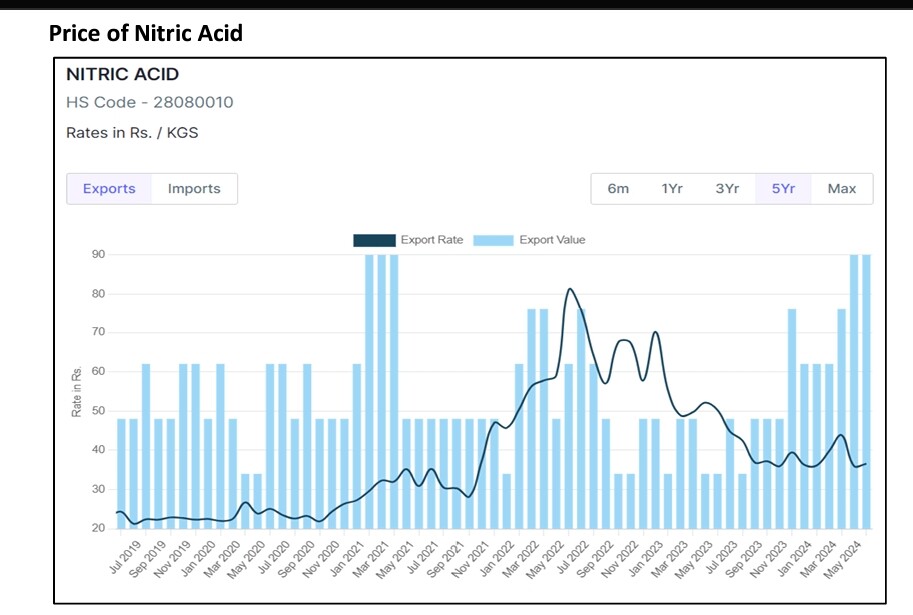

The global ammonia and nitric acid market is currently facing significant changes due to several key factors. Strict environmental regulations and high compliance costs are leading to the closure of ammonia production facilities across Europe, reducing regional supply. At the same time, natural gas prices are rising because of higher domestic demand and LNG exports, which is driving up production costs for ammonia producers, especially in Europe.

As a result of these developments, global prices for both ammonia and nitric acid are expected to rise, benefiting producers in regions with lower raw material costs, such as India. However, industries that rely on these chemicals, such as fertilizer and explosives manufacturers, may need help with these increased costs.

disc- invested, not buy/sell reco

15 Likes

Recent CRISIL rating A1 stable Rating Rationale

Highlights:

- Over the medium term, the operating margin should sustain at 18-20%, higher than the historical long-term average, aided by benefits from backward integration in ammonia

- DFPCL will also benefit from the lower-priced natural gas, as per its long-term contract with Equinor, priced favourably than its existing contracts

- Going forward, the group will raise additional debt to fund its capacity expansion in TAN and nitric acid, with an estimated capital expenditure (capex) of ~Rs 4,500 crore over next 2-3 fiscals

Disclaimer: Holding it in my portfolio

9 Likes

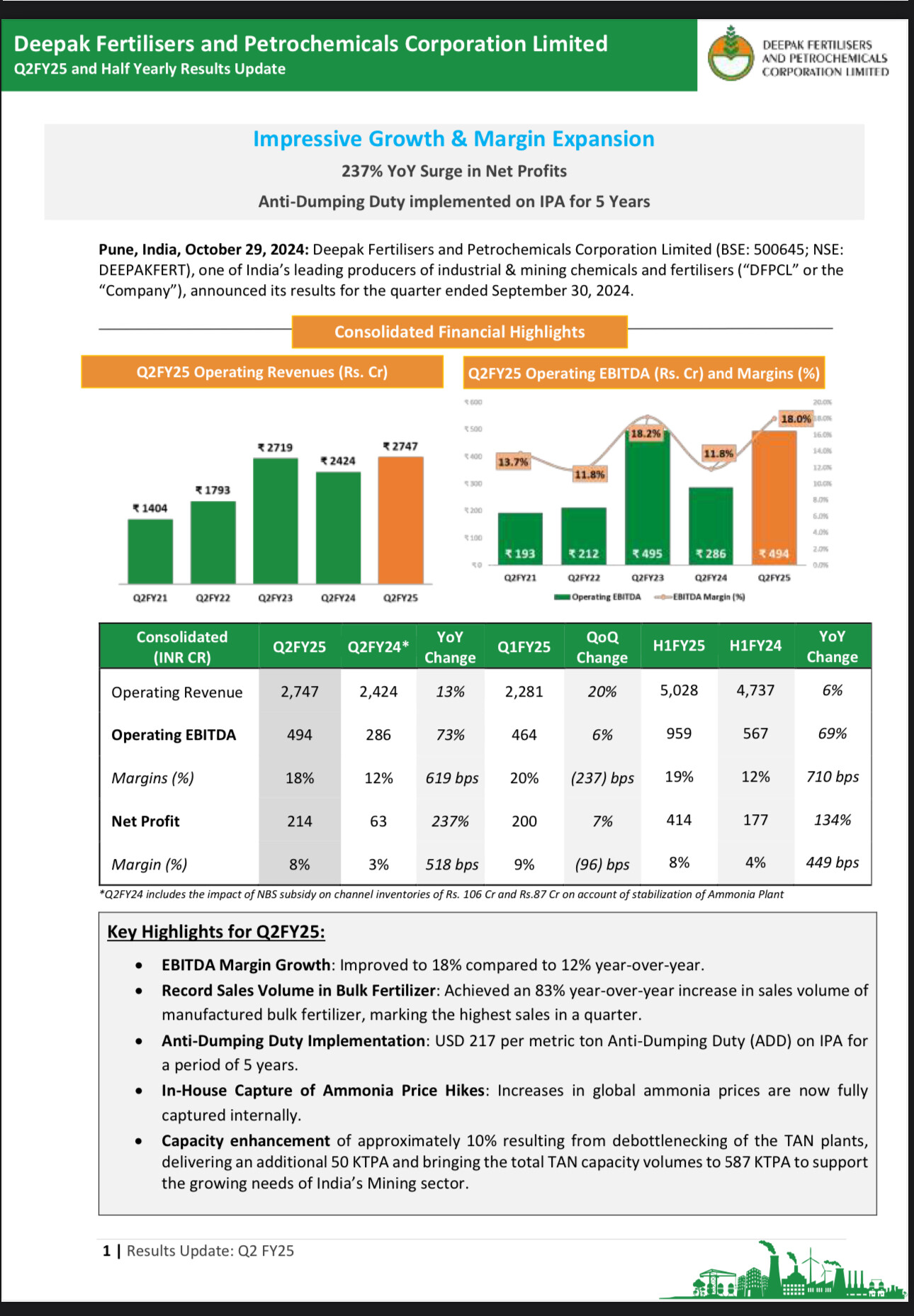

Q2 Fy25 Results

great set of no.s (driven by fertilizers, crop nutrition segment)

YoY revenue - 2,747cr Vs 2,424 cr ![]() 13%

13%

YoY PBT - 298 cr Vs 116 cr ![]() 156%

156%

YoY PAT - 214 cr Vs 63 cr ![]() 237%

237%

YoY EPS - 16.64 vs 4.76 ![]() 249.58%

249.58%

QoQ revenue - 2,747 cr Vs 2,281 cr ![]() 20%

20%

QoQ PBT - 298 cr Vs 269 cr ![]() 10.7%

10.7%

QoQ PAT - 214 cr Vs 200 cr ![]() 7%

7%

QoQ EPS - 16.64 vs 15.49 ![]() 7.42%

7.42%

• Debt Reduction: Prepaid ₹200 crores in debt, improving the Net Debt to EBITDA ratio from 2.66x to 1.64x.

• Change in key RM Prices in Q2FY25: Ammonia ~11% YoY; MOP ▼ ~40% YoY; Gas ~9% YoY

• Mining Chemicals (Technical Ammonium Nitrate):

• In Q2 FY25, premium product LDAN’s sales volume soared by 16% YoY and rose by an impressive 20% in H1 FY25 compared to H1 FY24

• Business Outlook: The mining and infrastructure is expected to pick up post monsoon as demand for Power (Coal), Cement & Steel is expected to increase thereby providing robust support for TAN demand.

Disc invested

12 Likes

4 Likes

Deepak Fertilizers | Q3 Highlights

a. CNB business continue to out-perform, revenue up by 55% YOY, driven by good monsoon and execution of crop focus value added strategy.

b. TAN business delivers revenue growth of 29% YOY, contributed by increase in LDAN and overall sales volume growth.

c. Management said India faced a slightly slower start to the year, but with the government’s ongoing focus on investment-led growth and strong structural drivers, we remain confident about the future of the chemical and fertilizer industries.

d. Our Q3 FY25 results reflect the strength of this confidence, highlighting the success of our strategic transition from commodity products to high-value specialty offerings, moving from customer to end consumers supported by effective backward integration and innovation

9 Likes

Why is the market punishing it? I thought the results were good.

may be due to decrease in ammonia price ?

any views from community ?

2 Likes

2 Likes

Just a few questions on the VP users tracking the company

- Russian exports of TAN were banned as they needed it for their own use during the war , and now if we see this war coming to an end in the near future how do you see the demand supply situation for TAN evolving due to this development ?

- Agrochem globally had seen overstocking after Covid-19 and have shown some initial signs of recovery , how do you see this development affecting demand-supply for TAN ?

5 Likes

Order imposing penalty passed against the wholly owned subsidiary of the Company i.e., Mahadhan AgriTech Limited.

Company has large debt in its book and also substantial Capital commitment for ongoing Capex which will further increase the leverage.

Exisitng Ammonia plant is below break even due to low ammonia prices and high Raw material Cost.(Latest Concal : Okay. I will not give you a very specific number, but as we spoke earlier, the moment we have an ammonia price crossing $400 FOB middle East plus, we start reaching more and more to near breakeven point.Ammonia - Singapore Exchange (SGX) present ammonia around USD 350). CAPEX of Rs 4500 Cr incurred and still not able to generate sufficient EBIDTA.

2 CFO have resigned in a span of 24 months.

Business nature is commodity. Other member can throw some light on the overall group leverage, recent pledging etc, .

Disclosure: Invested

7 Likes

Interesting snippet from Q4FY25 conference call

Having said that, there is a perplexment that does remain in my mind. Recently, when we did the CCD negotiations on the basis of just the mining business — DMSL — we were in a position to garner the funding at a 12x EV/EBITDA multiple, which puts the valuation of just the mining business at around ₹13,000 crores. Whereas, in totality, the entire Deepak Fertilizers group is being valued at only ₹17,000–18,000 crores. And the perplexment is this: how is it that the sum of the parts — meaning the totality of three businesses that are each doing well — is not being valued even as much as just one part?

9 Likes

CWIP as per balance sheet is 1403 Cr. TAN project CWIP should be around (75%) Rs 1650 Cr and Nitric acid CWIP should be around Rs 900 Cr i.e Total CWIP =2550 Cr.

why there is difference.

There was delay in project execution of around 2 years in its Ammonia project.

“. ICRA notes that there has been a time overrun (from Q4FY2022 to Q1FY2024) in the ammonia project on

account of the Covid-19 pandemic-related challenges, land acquisition & land conversion issues. It also faced cost overrun

(from Rs 2,920 crore to Rs 4,350 crore), owing to increase in land acquisition costs, EPC cost, addition of certain project

components, increase in foreign exchange component, Increase in cost towards storage and preservation of equipment and

interest during construction (IDC).”

Market would be wary about timely completion of CAPEX without increase in project cost. Further CAPEX of Rs 4500 Cr of Ammonia is below breakeven as Ammonia prices are less than USD 400 (presently 305 as per investor presentation).

Disclosure: Invested.

3 Likes

Deepak fertilisers.pdf (474.8 KB)

This was company announcement

Deepak fertilizer announced TAN plant back in Dec2021 and plant is getting commissioned next half of 2026. However, Chambal announced the TAN plant in 2023 and the project is commissioned in Jan2026.

I am tracking Deepak TAN plant from so many years and they always give quarterly update. How is Chambal so fast or is Deepak too slow?

Disc: Deepak Fert is my top 3 holding.

2 Likes