Disclaimer: Invested & Extremely Biased. Since management guards segment level EBITDA margins like nuclear launch codes, this is an exercise in reverse engineering, not clairvoyance. I might be directionally right or I might be hallucinating. Please consume with a generous bucket of salt.

Deepak fertilizers transition from commodity to specialty:

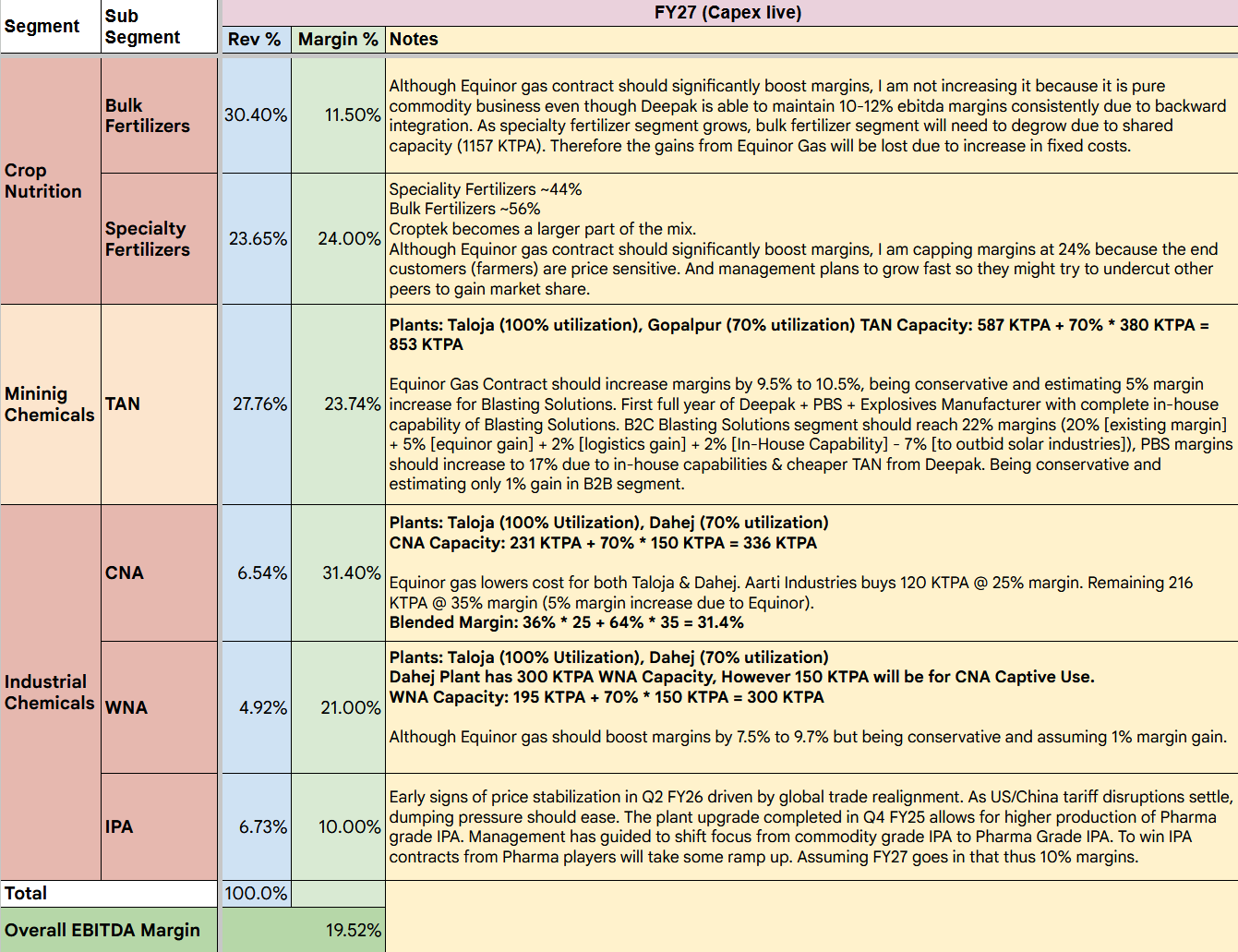

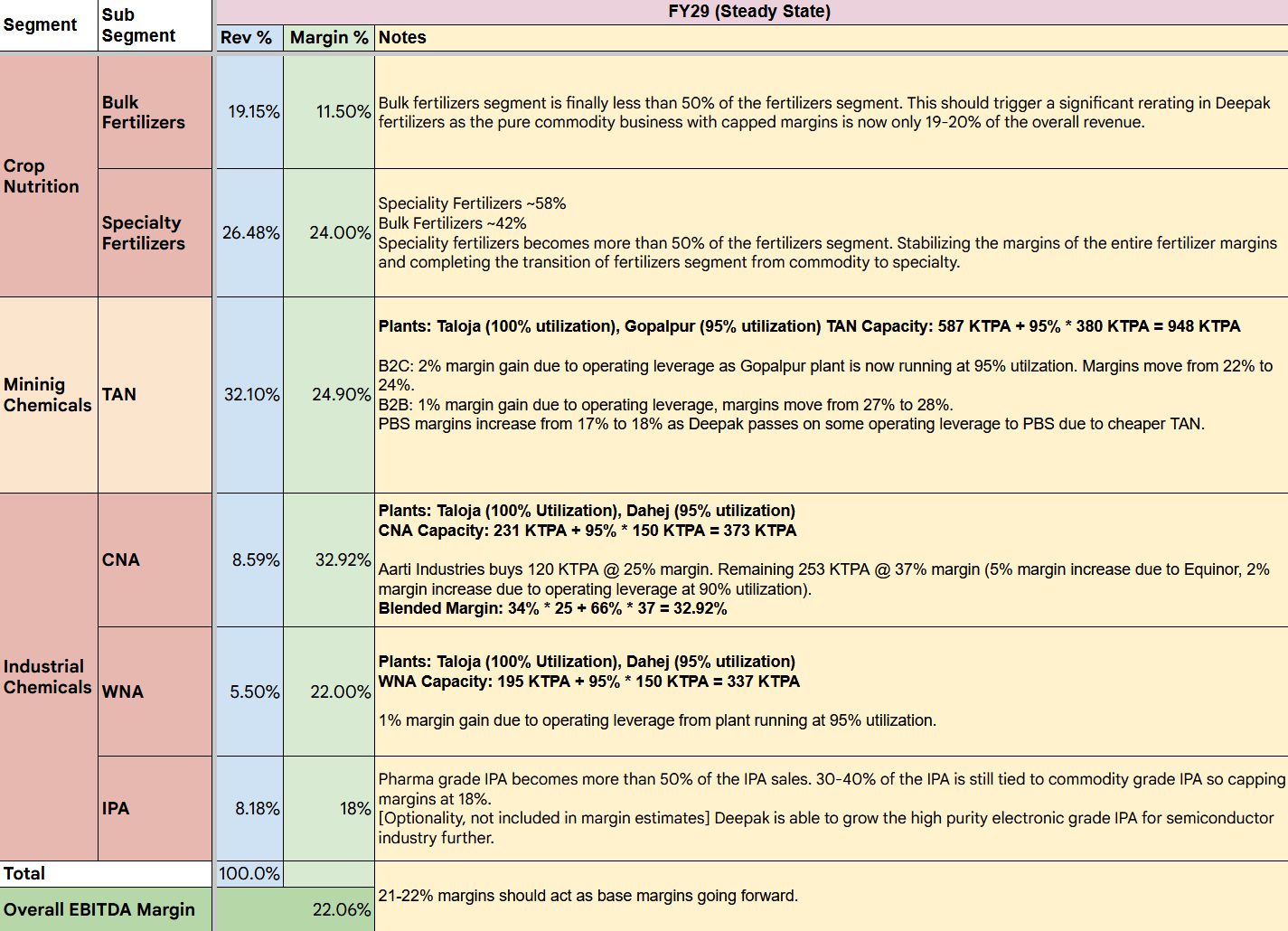

FY26

FY27

FY28

FY29

The above numbers do not include the unknown explosives manufacturer that they have bought. My estimate is by FY29, it should contribute 100-200 Cr of EBITDA. I have also excluded the ‘other’ segment which includes traded chemicals & fertilizers and real estate business.

Overall revenue from FY26 to FY29 will grow at a CAGR of ~13% and EBITDA will grow at a CAGR of 21%.

Excluding bulk fertilizers segment, revenue from FY26 to FY29 will grow at a CAGR of ~23% and EBITDA will grow at a CAGR of 28%.

Current Market Cap: 15,150 Cr

FY29 EBITDA based on my calculations comes to 3385 Cr. At 15x multiple, we get 50,775 market cap. At 20x multiple, we get 67,700 Market Cap.