Provision creation also factors what steps are you taking. If deep has confidence that they can recover ,that’s why they are not creating provision.

Regardless of the fact that debtors are due since March 22

Provision creation also factors what steps are you taking. If deep has confidence that they can recover ,that’s why they are not creating provision.

Regardless of the fact that debtors are due since March 22

This is like asking a thief whether he committed robbery.

Of course they are gonna say that they can recover. It is the duty of the auditor to determine whether these balances are recoverable or not. The auditors which did not carry out the aforementioned duty.

What he is saying is

According to Management, Loan given to Prabha earns them 12% p.a.

That means Loan amount * 12% should be Deep’s income and the same amount should be Prabha’s expense

But Prabha’s expense is only ₹15 lakhs. 15 lakhs interest (without amortization) on a 12% interest rate amounts to roughly ₹1.25 crores amount of loan.

Which does not match with the loan given to Prabha as per Deep’s financials

That means that they might be lying on the interest rate

So ultimately you are saying that, they have recognised debtors on March 25 and now you want results in just 6 months,what’s the update on debtors.

These are old debtors it will take time and this also involve court cases etc

Everything seems easy while arguing from a home

I could say the same for you boss. You are no different than me. We are both sitting at our homes

There is no point writing such cheap sentences when my replies have been respectful. I have never gone personal, at least when it comes to you.

I don’t want results in 6 months. What I want, is for the auditors to do their job, confirm the balances, acknowledge it’s recoverability, if any, and make provision if it’s not recoverable. Simple.

This discussion is looping and marching towards never ending story. I request not to take this too personally. Everyone has their own understanding. Even I am not good at these accounting items but I feel it’s too much. Can we stop this @kautuk @Pankaj_Motwani.

I talked with Prabha IR

They said they have capitalized the interest portion in CWIP, till the project gets commissioned

All right, makes sense now why Finance costs of Prabha is only 15 lakh

Also here is the summary of the loan given to Prabha, according to the latest AR

Also out of 751.88 interest income booked, 676.69 is interest receivable in the books of Deep. That means that the actual cash inflow from interest is less, though the management, rightfully booked, interest income on accrual basis. This can also be verified from the fact that the interest outflow in the Cash Flow Statement is less, which means no actual cash has been transferred from Prabha to Deep.

Its pretty standard since interest is always booked on accrual basis. Though this might potentially indicate cash crunch faced by Prabha if it persists for a longer time

There’s one point that prima facie is in favour of the management. By amalgamating Deep Energy, Savla Oil & Gas and Prabha, they have increased disclosures as Prabha and Savla Oil & Gas were earlier private limited companies

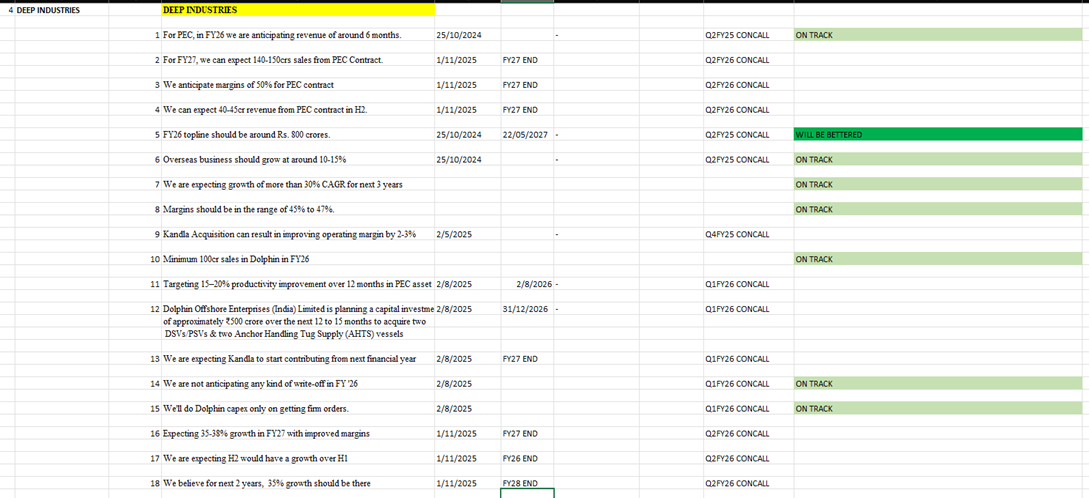

Q2FY26:

• Company’s order book stood at ₹ 3,050 Cr as on date. (Same as PQ)

CONCALL NOTES:

• ONGC PEC CONTRACT: We are expecting on full year basis revenue from this particular contract to the tune of Rs. 140 to Rs. 150 crores from next financial year onwards. And the margins we are expecting out of this contract in range of around 50% kind of EBITDA.

We can expect 40-45cr revenue from this contract in H2. In this financial year FY26, we are expecting total revenue of around 60 crores from this production enhancement contract.

We have crossed the baseline. And this production is increasing above baseline, which is progressing as per our expectation. And we believe from next financial year on full year basis; we would be earning as per our expectation.

So, price realization, currently it is in line with what ONGC used to sell. And with higher quantity coming up, we may take a call to sell at spot as well with higher price. But these decisions are dynamic and depending on the volume and availability of clients. So, but we are quite bullish on that part as well.

• Even if crude oil price is higher or lower, the activity of production is continuously going on with India being energy deficient country. And so, we have seen in last 20-25 years, this crude oil price movement generally not affecting us much.

• We believe this kind of other income (20cr) would continue in next half as well. So, interest and mutual fund income would definitely be continued in coming quarters as well. Of course, I cannot comment on revaluation gain on foreign currency

• So, we have a bidding pipeline close to 700 odd crores but it has a high potential to grow in the next quarters.

• We are expecting growth of 35% to 38% year-on-year basis in next financial year. Margins we believe should improve a bit going forward and we are expecting our EBITDA margins to grow upwards beyond 45% in coming quarters

• Expect to close QIP by end of this FY.

• W****e are expecting H2 would have a growth over H1.

• More PEC contracts: So, there will be various bidding rounds coming up. And if that happens, definitely, we will be bidding for it. And hopefully, we should win some of those projects.

So, their (ONGC) internal back-office work is going on. So, we cannot comment on the exact timeline when they will come up with such more tenders. But it is very much expected in coming quarters.

• Asset acquisition in Dolphin: We have identified and shortlisted few assets and we are working on it. Once we will be able to tie up those assets for contracts, we will go for acquisition. So, we are on quite advanced stage of that part.

• We believe for next 2 years, this kind of 35% growth is clearly visible. Depending on further addition to this order book, we can continue the momentum beyond 2 years as well.

• ONGC Sick Well program: ONGC Sick Well program is a little different than production enhancement. So, sick well is basically that they are not producing anything out of it. So, the challenges within sick well are different to the ones of the enhancement. So, there are few tenders that for sick well, they have already been published. We are evaluating that probabilities, and how potential are those. So, I think it will take some amount of time to evaluate and then perhaps we will take some decision on that.

• On potential of increasing competition: So, as the sector definitely gets more and more of business, potential business competition definitely is bound to come. So, that fact cannot be ignored. But having said that, we have been into this industry for more than three decades. And I believe that the edge that we have over the technical things and providing solutions to the client is something that matters the most. So, even after having a competition, I think we have already sustained for last three decades with a decent amount of growth. And I’m very sure that as we go forward, we’ll continue with that trajectory.

• This year, we are expecting to close Dolphin Offshore at around 100 crores of top line in FY26.

• My question was that I think we have around 100 crores of loans now as of now given. And we are raising QIP of 300 crores. Maybe some rationale for that. We are already giving loans and then we are raising equity. So, just maybe some rationale is there which I am missing to understand.

So, there one loan is given to company called Prabha Energy and it is a 12% interest bearing loan. And that particular loan was originally given before de-merger. So, I think that is still continue there.

• Given the company is already generating strong cash flows and has a very low debt level, what is the rationale behind raising 300 crores through a QIP? Is it primarily to accelerate the 400 crores CAPEX or to strengthen the balance sheet for future opportunities?

So, I would say both because we believe that our balance sheet should have the lowest possible leverage. As in our industry, we have always seen that people have gone wrong because of high leverage. And so, we believe that we should have leverage which should be very much in control. And of course, the momentum and the growth we are foreseeing in coming years, it would definitely help us capturing that growth with such strong balance.

Also, there are some possibilities we are looking around for acquisitions. So, when the acquisitions have to happen, we should be ready with our resources. So, there are multiple things related to the growth and acquisitions put together and therefore, we are trying to raise this fund.

• So, total CAPEX we are expecting is of 600 crores of which 100 crores has already been done. And balance would be going further, including the CAPEX for production enhancement contract.

THINGS TO TRACK:

• PEC Contract –Will they face technical difficulties as this is a new segment? Will the revenue generation be as guided? Can the segment surprise on the upside?

• New Offshore/Marine segments: Apart from the barge, what other segments/assets will the company get and how will its revenue and margins pan out?

• QIP and Potential Acquisition and Capex

• Gas Compression and Gas dehydration segments: How much will these be affected by increased competition going forward? Would new segments be able replace their revenue contribution in the long run?

• Core orderbook slowdown?: As focus of the management turns to PEC’s and Offshore segment, will the core segment slowdown a bit? Increased competition in those segments may have led the management to pivot to these new growth segments.

• Kandla energy operations progress: When will operations start? Impact on Ebitda margins and cost savings.

• Loan to Prabha energy: Since Prabha has started operations on gas field, will the loans by Deep get reduced?

Brilliant performance in H1 and stage looks set for even greater performance in H2 and even beyond. Share price reaction has been very poor recently. Sometimes market is like that or there maybe something going on behind. But we can only focus on the facts.

Yes, the issue of Prabha loan needs to be monitored and checked at annual report of next year.

Still, all being said, Deep looks ready to go into next orbit of scale over next two years.

DISCLOSURE: INVESTED

I was checking my monitorables tracker for Deep and I noticed the following fact -

In Q2FY25 concall, Guidance for PEC contract revenue and EBITDA margins was given as 100cr from second year at 40%+ EBITDA margins.

Now in Q2FY26, Guidance is raised to 140-150cr sales with 50% EBITDA margins.

So I think they are having better than expected progress on this contract.

P.S:

Whatever Deep’s management says they not only complete it but better it!

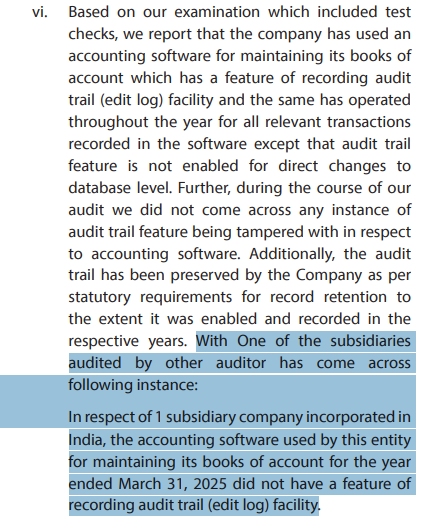

Please ask which subsidiary does not have an audit trail facility. If it’s Kandla, the receivables figures are even less reliable.

The more we get to know Deep, the more complex it becomes

Edit: It looks like Kandla, since AR 24 does not have this qualification

Long post ahead

A charge is a lien created against the company’s assets for a loan. So if you take a secured loan, the company has to register a charge on behalf of the loan provider so that in event of default, the loan provider can claim the proceeds from the sale of the said asset. So a charge of Re. 1 means the loan amount is either equal to or less than Re.1

All Working capital loans taken by Deep Industries are hypothecated against its Current Assets (65% of which are trade receivables). In fact, even some term loans (with maturity of more than one year) are secured against trade receivables.

Concept of Margin Requirement and why is it relevant

Suppose my Current Assets are Rs. 100 crores. If the bank gives a 25% margin, I will get a loan of Rs. 75 crores. If ay any point my Current Asset value falls below Rs. 75 crores, say 70 crores, I will have to deposit Rs. 5 crores (75-5) with the bank. This is also known as Margin Call.

Conversely, I can avail more loan if my Current Assets increase.

Deep Industries Ltd.

DIL Index of Charges.XLSX (19.5 KB) Source: Ministry of Corporate Affairs

Please refer to the excel above containing all charges yet to be satisfied. (Satisfaction of charge occurs when either the loan is repaid or asset is removed from the charge).

Row 22; Charge Holder PNB Investment Services Ltd. ; Date of Creation 23/01/2023

As depicted in the first pic of the post, PNB Investment Services is the Security Trustee for charges against the company’s Current Assets. The amount of charge is a whopping Rs. 237. 50 crores.

Interestingly, this charge was created (loan taken against current assets) only weeks after the acquisition of Dolphin, where around 150 crores of receivables (Current Assets) were added in the balance sheet of Deep Industries. The receivables, which by the way are outstanding from a very long time and for whom no provision has been made yet. (A provision would reduce the trade receivable balance and hence reduce the amount of total current assets, which could trigger a margin call)

Similarly, just months after the acquisition of Kandla Energy, another charge was created on 8/09/2025 (refer row 2 of the excel) in favour of Axis Bank Ltd. Axis bank has too provided Working capital Loans to the company.

Notice a pattern? Acquire companies cheaply, with high receivables. Keep the receivables in the consol books. Do not make a provision (which would reduce current assets). Ask the auditors to not verify those receivables. Take working capital loans against those receivables. Acquire companies cheaply.

There is a clear benefit to the management by not writing off receivables. If it did, its working capital sanctions would get affected, drastically. Imagine the impact of a 300 crore write off in the current assets on the outstanding working capital loan limit.

Furthermore, the current borrowings, excluding current maturities of long term debt has almost increased by 8 times as at 31.03.2025 when compared to 31.03.2024! I would not be surprised if this figure increases further.

I once asked a question on the Kandla acquisition, Why now? I have gotten my answer. Free onboarding of 200 crores of receivables which will enable them to take loans against them faster. In fact this could also be the reason why management is not letting the auditors verify those balances. Kandla also did not have a audit trail per se. So there are no internal controls, external verification or other confirmation regarding these balances against whom such gigantic loans are taken. They needed to take a WC loan faster and hence hurried on the Kandla acquisition to increase their book value of current assets.

This in my humble opinion establishes a clear motive for the management to not take provisions for receivables.

Regarding Inventories

Inventories are also current assets. The management in fact did take an inventory write down as an exceptional item in FY 2025. Here is my theory (the below two paragraphs should not be construed as a statement of fact):

As per regulatory requirements, stock audits should be carried out for all WC limits in excess of Rs. 5 crores. Stock audits are also required to be certified by a practicing Chartered Accountant and the margin requirement for stocks is much less than that of Debtors. (For example, for stock worth 100 crores you will get a loan of 85 crores as against a loan of 60 crores for a 100 crores worth of debtors)

Now when the stock auditors conducted the stock audit, they realised that the stock acquired from these acquisitions are not realisable and hence made them (the management) write down its inventory. There is no such requirement for debtors, lol. The management in fact admitted in an earnings call that these inventories were not realisable.

Some tough questions for the management in the next earnings call in addition to the usual 60% growth guidance ones:

The Game, Mrs. Hudson, is ON.

Short term borrowings are 109cr. Inventory + recievables excluding Dolphin & Kandla receivables stand at around 350cr Rs.

Short term borrowings excluding current maturities of long term debt is at 24cr. Which has increased from 3cr last year. For a company with around 2000cr of operating assets and increasing scale, 20cr jump is literally nothing (So much for your WHOPPING 8X JUMP)

Also 24cr of short term borrowings against 350cr of working capital assets (It’s just too ridiculous to make any argument when facts are such as these)

Same assets maybe hypothecated with different financial institutions for working capital limits.

Also I am pretty sure there would be enough due diligence from the bank side on these old receivables to not lend against them. Even Deep has stated in public forums that these were gotten for miniscule amounts and recoverability of them is to be ascertained over the next two years.

2cr was the amount paid for Kandla energy. Any point you make against Kandla basically irrelevant for me as practically no money was spent to acquire it. (If out of the 300 odd cr receivables, they manage to recover even 3cr, that’s a 50% return on investment, apart from the actual chemical business which should start by next FY)

They rely on the auditor’s report.

This is like asking a thief whether he committed robbery. Of course they are gonna say these are recoverable. It is the job of the auditor to determine whether in fact they are realizable.

Any point you make about no money being spent to acquire Kandla is irrelevant to me. I have explained reasons in earlier posts

This is as per 31 March 2025. As per MCA, the company registered charges worth 37.50 crores from June 2025 to date alone. Let’s say still the working capital is 350 crores. But the working capital is hypothecated against term loans as well. And the term loans figures are pretty big

So anyway I have come to a sudden realisation that writing on Deep Industries is not worth both the reader’s and mine time/efforts.

I will spend time that I could use otherwise to find something on Deep, think of a movie reference to write it on VP and post it here. Existing investors would spend equal time to find wrongdoings in my thesis and post them here.

It’s really not worth it. I am just tired of it all. I am sure others are too.

I hope I am wrong about Deep though. Don’t want my fellow members to lose their hard earned money.

Anyway I would like to apologize if I unintentionally came off as rude or blunt. Trust me it was not my intention. I just wanted my posts to be fun to read. All of this would be worth every second spent if someone learnt something from the convos above. Be assured I learned a lot for which I am really grateful :).

My conclusions on Deep:

It’s a good company, showing real growth, growth drivers. But obviously not plain as white. There sure are grey areas.

This is the last you will hear from me on this thread. Until next time

Indeed your efforts are valuable. Not sure what triggered sudden exit from this discussion but love to see you in other threads as well. Atleast I don’t understand this level of accounting but sometimes and for someone this really helps a lot. Thank you for all your insights.

@kautuk I learnt a lot from this discussion. Thank you.

I was advised by well-meaning friends not to invest in Deep because of CG, but by that time I had earned great returns after 2 years of holding.

I’m an accounting newbie and can’t even think of such research like you did. Thanks a lot for the education. It has certainly made me re-evaluate my holding.

They have sufficient Assets in their book . even if we exclude those acquired debtors, their borrowing amount is just 15-20% of their Fixed assets + other assets like normal inventory debtors levels

So I don’t believe they really need those acquired debtors for working capital