Deccan Gold:- After spending two decades as an explorer, Deccan Gold Mines is stepping into its golden moment. The company is moving from studies to real production in two of its gold mines. One is India’s first new primary gold mine since Independence (Jonnagiri - GMSI) now coming alive after producing ~60 kg in trials and targeting ~500 kg gold production per year. And another one is Its Altyn Tor project in Kyrgyzstan which has also begun trials and expects 300–350 kg gold production in FY27. For the first time in its history, Deccan is on the verge of generating real cash flows, just as global gold prices touch record highs.

Beyond Jonnagiri & Altyn Tor, the company is positioning itself as a broader critical-minerals play, aligned with India’s ambitions to build domestic and international presence in strategically important resources.

-

Its entry into Finland through Kalevala Gold Oy marks Deccan’s first venture into a Tier-1 mining jurisdiction.

-

In Mozambique, the company has secured exposure to Lithium, Cesium and Tantalum (Li-Cs-Ta), along with Gold-Copper prospects.

-

More recently, Deccan has expanded into Europe with the Logrosán tungsten project in Spain, adding another critical mineral to its portfolio.

-

Gold exploration in Tanzania

India’s Gold Mining History till date

Historically, India had more active production but most large mines closed (Kolar Gold Fields (KGF) was a major historic producer, producing >800 t during its lifetime, and was closed in 2001). Since then domestic production has been negligible outside Hutti. IBM and GSI show that while geological potential exists, actual annual primary production has been single-digit tonnes for many years.

KGF in Karnataka is one of the world’s oldest and most famous gold mining regions. Mining here dates back centuries, but large‐scale industrial extraction began under the British in the late 19th century. Over its ~120‐year history (1880–2001) KGF produced on the order of 800–900 tonnes of gold. The mines reached remarkable depths (nearly 3.2 km, historically one of the deepest mines), and even powered Asia’s first electrified mining operation (in 1902).

The KGF/BGML mines shut down in 2001 for multiple interrelated reasons. By the 1990s KGF was unprofitable. Operating costs (power, labor, maintenance) far exceeded gold revenues. A key issue was price control: BGML had to sell its gold to the Government at London Metal Exchange (LME) prices, which were often below world market prices. In Parliament (2024), the Mining Minister stated that operations were closed because they became economically unviable. With global gold prices also low in the late 1990s, there was no economic justification for heavy investment.

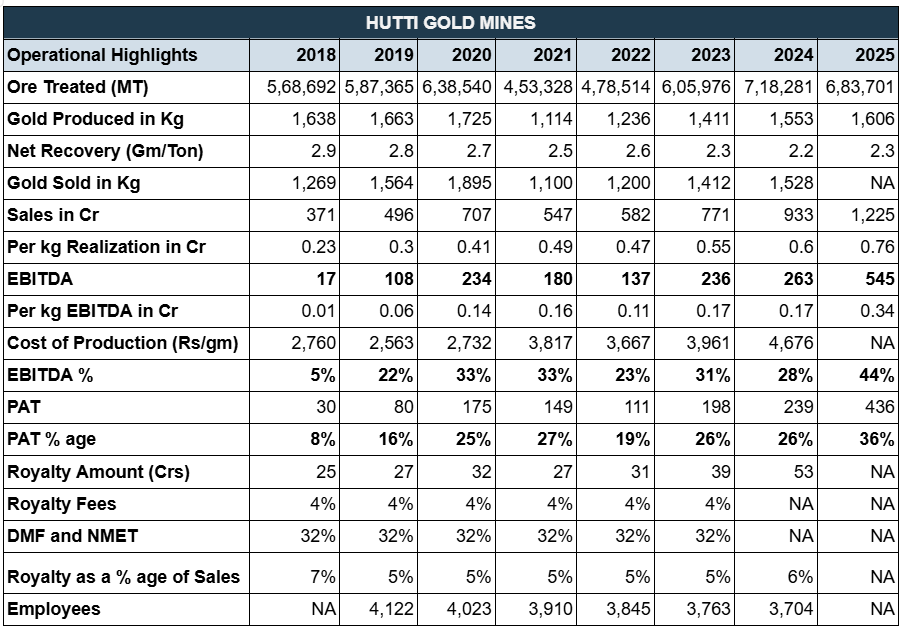

The other significant gold producer in India has been Hutti Gold Mines which is also the only primary gold producer in India presently. Hutti was established in 1947 as Hyderabad Gold Mines, HGML is a Government of Karnataka undertaking. Today it operates Hutti Gold Unit (HGU) in Raichur – a fully integrated mine with 5,50,000 TPA capacity.

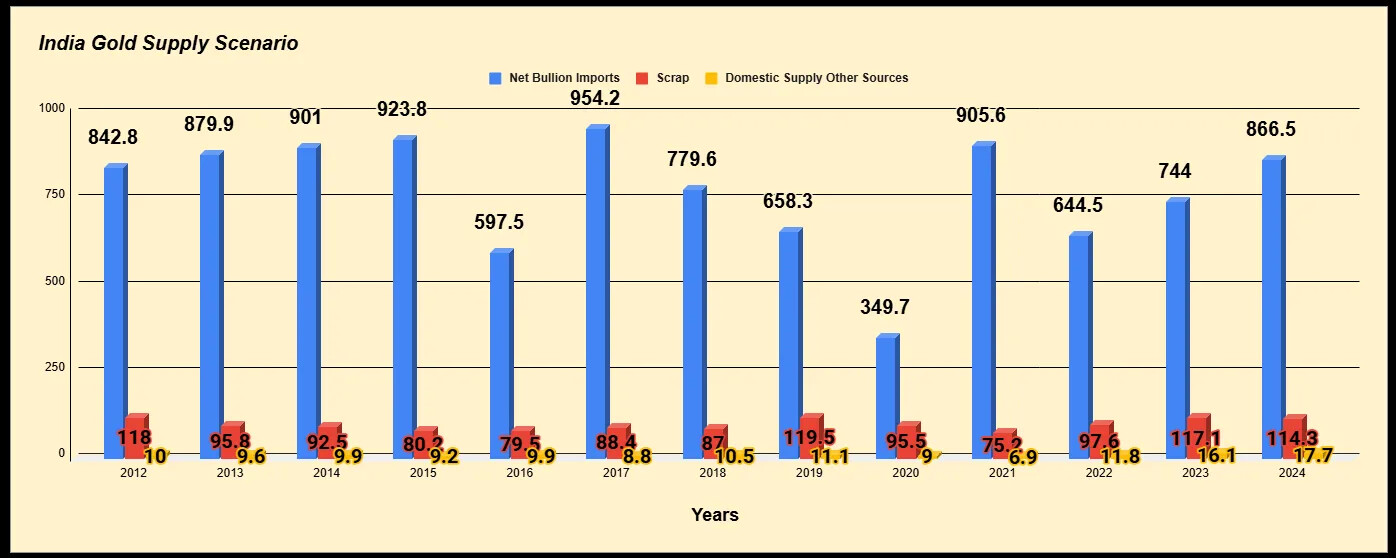

India’s Demand and Supply Scenario

India is a very large gold consumer (~800 tonnes of demand in 2024) but produces almost no gold domestically (state-run Hutti ~1.5 tonnes/year). Most Indian demand is met by imports (Switzerland, UAE, South Africa, Peru among top sources).

India accounted for above 16-17% of global gold demand both in volume and value terms (WGC Report, 2024). In particular, Indian shares of global gold demand in 2024 stood at 16.1% in terms of volume (802.8 MT out of global demand of 4974 MT) and 16.3% in terms of value (USD 62 Billion out of global demand of USD 382 Billion).

On the Supply Side, we have:

-

Domestic mines

-

Recycling / processing other metals

-

Imports

-

Hutti in Karnataka, accounts for 98% of the total production, while Jharkhand accounted for the rest.

-

Small quantities of gold are produced as a by-product from other minerals, mainly copper. These sources contribute only limited volumes. The largest such source is Birla Copper’s smelter at Dahej in Gujarat, which processes both domestic and imported copper concentrates. During copper refining, trace amounts of gold present in the concentrate are recovered as a by-product. The Dahej plant has an installed gold recovery capacity of about 15 tonnes per year, although actual production has been lower; for example, gold output was around 6 tonnes in 2020, well below its rated capacity.

Then, How’s the demand getting fulfilled in India?: Via imports- In 2024, India ranked as the 5th largest gold importing country globally with USD 51.8 billion worth of import and accounting for more than 9% in the global gold imports. India was placed behind Switzerland (18.3%), China (17.9%), UK (13.4%) and Hong Kong (11.4%) as a percentage of total gold imports globally.

According to the World Bank Report (2024), Gold stood 2nd in the major import commodity list of India with an import value of 47 USD billion in FY 2023-24 following Crude Oil’s import value over USD 180 billion. Gold import directly hits our forex reserves.

What matters now? Let’s look at the current and future of DGML:

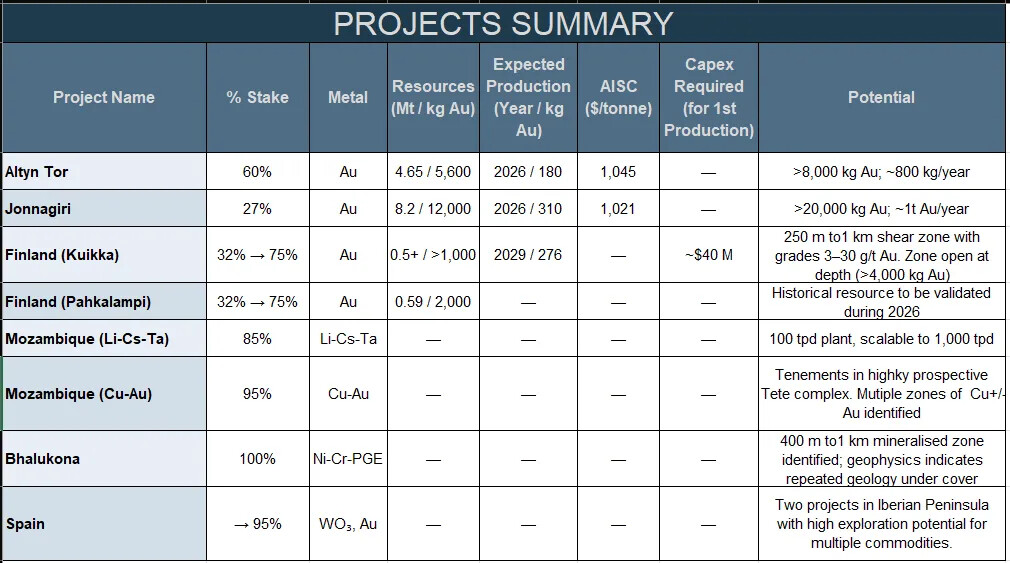

DGML has 2 projects which are about to start mining and few more in pipeline, let’s look at them one by one.

The flagship project, Altyn Tor Project: Altyn Tor is Deccan Gold Mines’ flagship overseas project and its first real step toward becoming a geographically diversified gold producer. The company’s investment into Avelum Partners, which owns and operates the Altyn Tor mine, marked Deccan’s entry into Kyrgyzstan and signalled a clear intent to build cash-flow-generating assets outside India.

What makes Altyn Tor especially attractive is its simple geology and metallurgy. Gold at the site is hosted in quartz and quartz-carbonate veins and stockwork zones, and the ore is free-milling in nature. Historically, recoveries of around 60% were achieved using gravity circuits alone, which places the project in a very low-risk metallurgical category. In practical terms, this means Altyn Tor does not require complex or expensive processing like roasting or pressure oxidation, keeping both capex and operating risk firmly under control.

On the resource side, the project currently hosts about 4.65 million tonnes of mineral resources at an average grade of 1.21 g/t gold, equivalent to roughly 5,600 kg of contained gold, with a 0.5 g/t cut-off grade. Interestingly, the resource base already includes around 1.4 million tonnes of historic tailings and low-grade stockpiles, containing approximately 1,590 kg of gold. These tailings were left behind by earlier operators because gold prices were lower and processing technology was less efficient at the time. Today, with better recovery methods and much higher gold prices, this material has become economically attractive again.

There’s also some clear upside beyond the current resource. Limited step-out drilling around the existing mine footprint has already indicated the potential to add at least another ~620 kg of gold, suggesting that Altyn Tor could quietly grow into a larger asset over time.

Put simply, Altyn Tor supports the mining of roughly 5,600 kg of contained gold, and nearly 1,590 kg of that comes from tailings alone. Since the tailings material has already been mined and crushed in the past, there is effectively no mining cost involved — only re-treatment and processing costs. That translates into:

-

faster cash-flow generation,

-

much lower capital requirements, and

-

significantly lower execution risk.

Broadly, Altyn Tor gives Deccan a great mix of near-term production, simple processing, low technical risk, and quick cash-flow ramp-up. In many ways, it acts as Deccan’s financial beachhead outside India — a project that can start generating real money relatively quickly and help fund the company’s much bigger long-term ambitions in gold and critical minerals. The company expects a 180 Kg and 350 Kg per annum gold production in 2026 and 2027 respectively with a peak potential of 800 Kgs per annum in 3-4 years.

Let’s move to Deccan Gold’s most advanced domestic gold asset—and the cornerstone of its long-term India gold strategy—the Jonnagiri Gold Project.

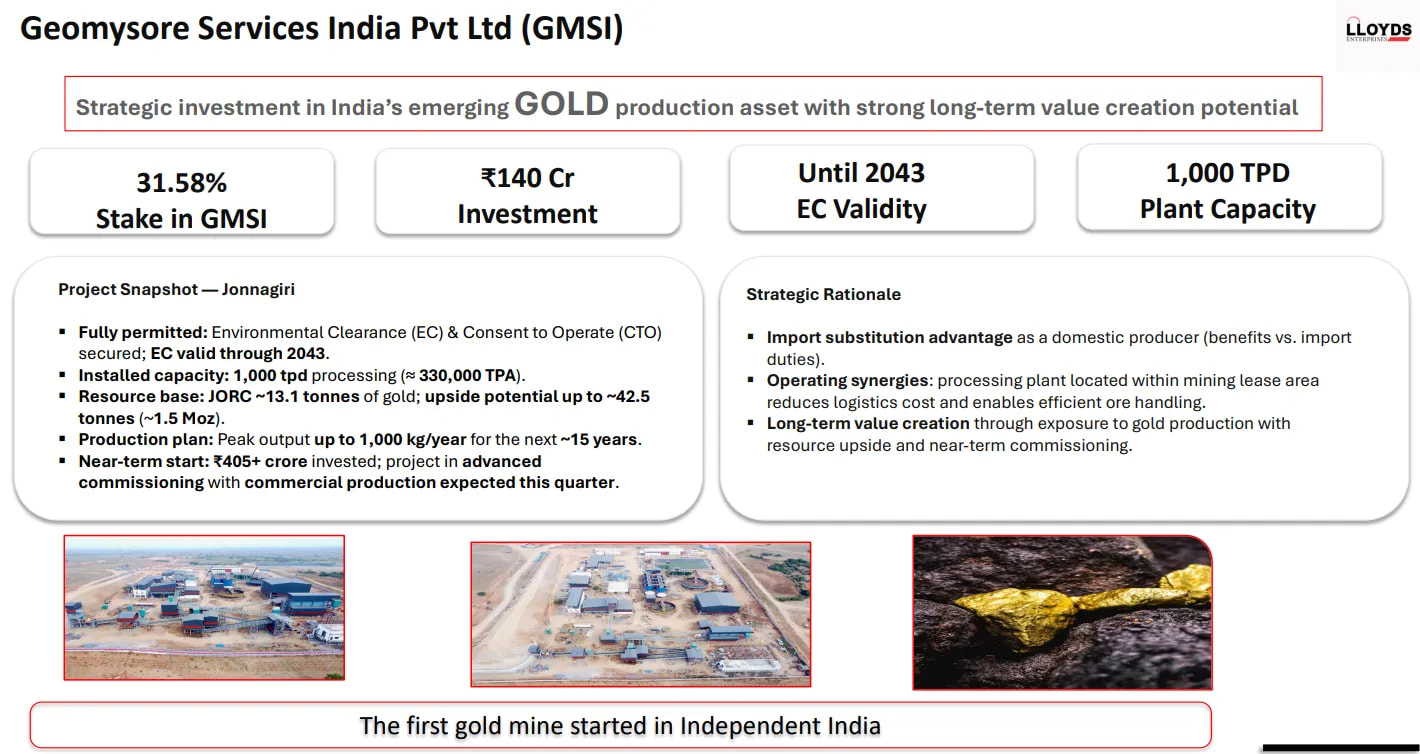

Located in the Kurnool district of Andhra Pradesh, Jonnagiri is India’s first private-sector gold mine. The project is owned and operated by Geomysore Services (India) Pvt Ltd (GMSI), a joint venture between Thriveni Earth Moving, Lloyd Enterprises, and Deccan Gold Mines. Jonnagiri currently hosts 6.5 million tonnes of mineral resources at an average grade of 2.03 g/t Au, translating into approximately 11351 Kg of gold mineralization, with meaningful upside discovery potential as mining progresses. The combination of open-pit mining and simple metallurgy makes this project structurally low-risk, economically attractive and highly profitable.

Who is GMSI?

GMSI is one of India’s most experienced gold exploration and development companies, operating since 1994 with

-

Mining capacity: 0.4 MTPA

-

Processing capacity: 0.3 MTPA

-

Exploration footprint: Over 35,000 sq km across India with focus on Precious and base metals

In short, GMSI brings execution capability—not just geological ambition.

What’s GMSI?: GMSI is a gold exploration and development company operating across India since 1994. The company has a mining capacity of 0.4 MTPA and a processing capacity of 0.3 MTPA. With a focus on precious and base metals, Geomysore has explored over 35,000 sq.km and made significant discoveries in major geological belts across multiple states.

Shareholding Structure & Why Lloyd Matters

As per disclosures dated July 2025:

-

Deccan Gold Mines: 26.7%

-

Prakar Estates & Promoters LLP: 63.17%

-

Lloyd Enterprises: 50% stake in Prakar LLP

This implies an effective 31.58% indirect stake for Lloyd Enterprises in GMSI.

Why is Lloyd important?

Lloyd Enterprises holds a 31.58% stake in GMSI. Lloyd Enterprises is part of the broader Lloyd Group that also controls Lloyds Metals & Energy — one of India’s fastest-growing iron-ore miners. This matters because Lloyd’s involvement is not that of a passive financial investor. It brings into the Jonnagiri ecosystem a promoter group that already understands how to build, permit, finance, and operate large mining projects in India.

Its EPC and infrastructure background materially de-risks mine development, plant expansion, and on-ground execution at GMSI. In many ways, Lloyd’s presence converts GMSI from a geological asset into a scalable, bankable gold production platform.

How Jonnagari started?- Geomysore applied for a Mining Lease over an area of 5.97 sq km in the year 2006. The Government of Andhra Pradesh had advised Geomysore to submit an approved mining plan for considering the grant of Mining Lease. Accordingly, Geomysore submitted a Mining plan to the Indian Bureau of Mines in 2008, which was approved on 04th August 2008. Geomysore also received the Environmental Clearance from the Ministry of Environment and Forest in 2010 which is valid till 2043.

As per Deccan’s latest presentation:

-

JORC Mineral Resources: ~8.2 Mt @ 1.49 g/t Au

-

Contained gold: ~12 tonnes

-

Potential upside: Could scale to 32+ tonnes as mining exposes depth and extensions

Management has consistently highlighted that gold mines are built in stages and often outlive initial mine plans.

Dr. Hanuma (Q2 FY26 concall), while discussing Altyn Tor, summarized this well:

“*I will give you the example that is currently being operated, that is Hatti Gold Mines. It was started in 1945 as a surface small operation. Today it is operating at a kilometer depth and it is an underground mine. So most of the gold mines will go to a much larger depth”

*

The same logic applies to Jonnagiri.

Mine Life and Expansion Potential as per Deccan

Under current approvals:

-

Processing capacity: ~330,000 TPA

-

East Lode mine life: ~10 years

-

Extended life potential: 12–15 years with additional resources

GMSI is also in the process of updating its 2017 Feasibility Study, which management believes will:

-

Increase Mineral Resources materially

-

Expand final pit limits

-

Improve long-term economics

Lloyd enterprises in its latest presentation shared an update regarding their Jonnagiri project:

-

Environmental Clearance (EC) & Consent to Operate (CTO) secured; EC valid through 2043.

-

Currently it has a 1000 TPD capacity and a Resource base: JORC ~13.1 tonnes of gold; upside potential up to ~42.5 tonnes (~1.5 Moz).

-

Near-term start: ₹405+ crore invested; project in advanced commissioning with commercial production expected this quarter i.e., Q3 FY26.

-

Production plan: Peak output up to 1,000 kg/year for the next ~15 years.

GMSI also also expected to list separately over the next 2 years. This can be a big trigger for value unlocking for Deccan.

-

The Finland Gold Project (Kalevala Gold Oy): Deccan’s Finland entry marks its first serious step into a Tier-1 mining jurisdiction. The company currently holds a 32% stake in Kalevala Gold Oy, with the option to increase this to up to 75% as the project advances.

- The development vision here is fairly ambitious. A 1,000 TPD processing facility is planned, and management believes that annual gold production of around 700–1,000 kg per year could be achieved for at least the first five years of operations. Total capital expenditure for this phase is estimated at roughly US$40 million (₹300–320 crore).

On the resource side, the project already has two meaningful blocks although Kalevala holds tenure across 3 gold exploration projects in Eastern Finland:: Kuikka block: ~0.5 million tonnes with over 1,000 kg of gold, with upside potential that could take this beyond 4,000 kg as exploration progresses. Pahkalampi block: ~0.59 million tonnes with around 2,000 kg of historical gold resources, which are expected to be validated and upgraded during 2026. While still some distance from production, Kalevala gives Deccan a foothold in Europe, long-duration gold optionality, and a credible second gold growth leg beyond India and Kyrgyzstan.

Mozambique (Li-Cs-Ta)- 85% stake: Deccan’s Mozambique presence is arguably its most strategically important non-gold bet, especially given global interest in critical minerals.

This project gives Deccan direct exposure to

-

Total planned investment: US$30–40 million, including the processing plant.

-

Amount already invested: ~US$25 million (~₹220 crore).

-

Additional near-term capex: ~₹20 crore to bring the plant into operation. The development plan includes setting up a 1,000 TPD processing facility, with envisaged output of around 200 tonnes per day of lithium concentrate. This will not be battery-grade lithium. Instead, the concentrate is expected to be shipped to India, where it can be further processed depending on grade and market demand.

Mozambique Cu- Au (95% stake): Deccan also holds a 95% stake in a copper–gold exploration project located in Mozambique’s highly prospective Tete Province, a region that remains largely unexplored for copper and other base metals despite favourable geology.

- Multiple zones of Cu- Au mineralisation have already been identified across the company’s tenement package, and copper mineralisation has been clearly established in parts of the licence area. In several locations, small-scale and artisanal miners are actively scavenging for copper oxide minerals such as malachite and azurite, which are classic surface indicators of underlying copper sulphide systems at depth.

Chhattisgarh Bhalukona (Ni-Cr-PGE)- 100% stake: Back in India, Deccan is building optionality in base and precious metals through the Bhalukona project in Chhattisgarh, which is prospective for nickel, chromium, copper, platinum, and palladium.

-

This is still an early-stage exploration project. Meaningful drilling is expected around

-

10,000 tonnes of copper, and

-

10,000 tonnes of nickel, along with by-product platinum and palladium.

Management has acknowledged that the company paid a ~21% premium to secure this asset, which is a bit on the higher side.

-

Spain Logrosan exploration project: Deccan’s entry into Spain marks its foray into Tungsten, a globally recognised critical mineral with major applications in defence, aerospace, high-temperature alloys, industrial cutting tools, and electronics. The company has the option to acquire up to 75% of the Logrosán project prior to production. One of the most attractive aspects here is that the project already hosts known mineralisation, and management believes it can be converted into a formal Mineral Resource within 1–2 years.

Gold exploration licenses Tanzania: Beyond Europe, Deccan has been steadily building optionality across highly prospective African greenstone belts. A key pillar of this diversification is Tanzania—one of Africa’s most prolific gold-producing regions.

Deccan Gold currently also holds six prospecting licenses in Tanzania, including four semi-contiguous gold licenses in the Nzega District, one license near the Geita Gold Mine, and a newly acquired lithium license. Initial greenfield exploration at Nzega involved mapping, rock chip, and soil sampling, which returned encouraging gold anomalies. During 2025, Deccan completed detailed follow-up work across anomalous zones, including structural analysis and additional sampling, with results currently awaited. **

Below table summarizes all the projects of the company:**

Valuations and My view:

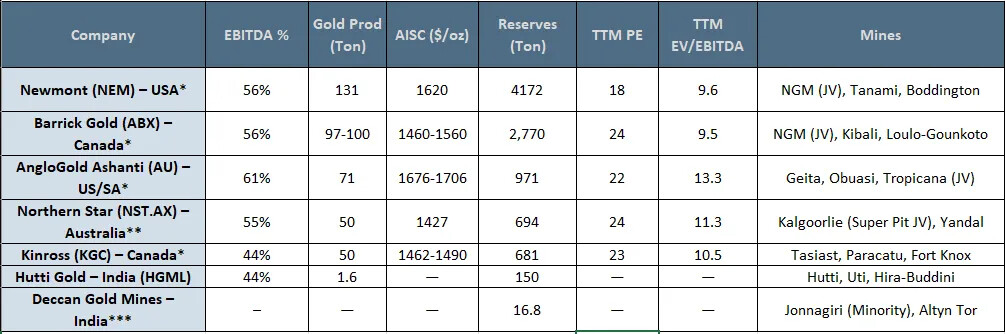

We looked at Newmont USA, Barrick Gold Mining Canada, Anglogold- US, Northern Star- Aus, Kinross- Canada and Hutti Gold Mines (India) to get a grip on how Gold miners are valued globally. Broadly companies traded at 18-25x P/E multiples and 10-14x EV/EBITDA.

Players listed below in the table are very large, established global gold miners with operations across geographies. Deccan Gold on the other hand is a smaller player trying to diversify itself across a range of critical minerals. Below table showcases how global players are valued:

-

*Figures are for CY2025 Revenue,

-

EBITDA, and Gold produced are on 9M basis unless **

-

**figures are for FY25 P/E and EV/EBITDA on TTM Basis from Yahoo Finance

-

*** Deccan mines are early stage- Scope for reserves upgradation

Note: For DGML only proved reserves are considered at this stage. Whereas for rest proved as well as probable reserves are considered.

Deccan trades at a Mcap of 2464 Crores and we expect an attributable EBITDA of 200-250 / 400 Crores in FY27 / FY28, the stock trades at ~10x / 6x FY27E / FY28E EV/EBITDA (net debt free post recent Rights issue).

Deccan’s steady state EBITDA can be 800 to 1000 Cr from these 2 projects in 3 years. It is at the start of its production and cash-flow growth curve with real production coming in CY2026. Over FY27-30, it will witness structural growth in mineral volumes, revenues and operating cash flows hence we expect valuations to be at a premium to global critical mineral players.

What’re the Risks in the story:

Things can always go wrong — and in mining they often do — so it’s important to examine the key factors that could derail Deccan’s investment thesis.

-

Regulatory / Legal Risk – India: Regulatory/legal risk in India is binary and structural: a single SC judgment line could mean:

-

Ganajur/Hutti assets are permanently locked into auction/compensation, or

-

A narrow window opens for a few advanced pre‑2015 cases.

-

-

Exploration & Technical Risk: DGML has moved some assets (Jonnagiri, Altyn Tor) past the pure exploration risk, but others (Bhalukona, Mozambique Cu, Tanzania) are classic early‑stage, high optionality, high failure‑rate bets.

-

Execution Risk: Any delay in mining in GMSI or Altyn Tor can delay cashflows.

-

Funding/Dilution Risk: DGML has deliberately leveraged equity heavily to buy into near‑term assets (GMSI, Avelum, Kalevala). If Jonnagiri and Altyn Tor cash‑flows ramp as guided, that equity will be amortised by earnings. If not, the company is at risk of becoming a perpetual issuer, diluting future upside into each new round.

Governance & Management: Who Really Runs Deccan Now?

From “old DGML” to “new DGML”: leadership change. For most of DGML’s public life, the face of the company was:

- Sandeep Lakhwara – former Managing Director, with a long history in DGML, primarily focused on Indian exploration (Ganajur, Hutti, Dharwar).

The pivot begins around 2021–2022:

- The board brings in Dr. M. Hanuma Prasad as a central figure:

- Initially via Geomysore (GMSI) – he was MD of GMSI and architect of the Jonnagiri build.

- Gradually transitions from GMSI to DGML.

- By late 2021 / 2022:

- Sandeep Lakhwara’s term as MD ends.

- Dr. Hanuma Prasad is appointed Managing Director of DGML.

The new MD is:

- A geologist with ~25–27 years of exploration and mining experience, across India, Africa, and Central Asia.

- One of the key brains behind:

- Jonnagiri’s resource definition and FS,

- The Avelum/Altyn Tor acquisition,

- Entry into Mozambique and Bhalukona, and

- The global exploration/consulting effort via Dubai (DGFZCO).

DGML moved from a “legacy Ganajur‑first explorer” mindset to a more aggressive “multi‑jurisdiction project developer” posture, and the MD change is both a symbol and a driver of that.

Governance story

- Positives:

- Clear technical leadership at the top (MD is a geologist with real project execution under his belt).

- Board/management bench has global experience (BHP alum, ex‑civil servants in Kyrgyzstan, African exploration leadership).

- Strong disclosure of key capital transactions, loan terms and project updates; willingness to face tough Q&A publicly.

- Concerns:

- Heavy dilution since 2015; existing shareholders have had to absorb multiple rights, swaps, and warrant rounds.

- Dependence on specific anchors (Hira, AIR, Lionsgold, Med Edu) for funding and equity, with GMSI pledge at the centre until Jan 2026.

- Timing of capital raises (e.g., Dec 2025 rights issue before production numbers are visible) has alienated some long‑term retail holders.

Disc: Hold Tracking position and this is most relevant excerpt of a substack blog we wrote.

Sources:

-

https://www.bseindia.com/xml-data/corpfiling/AttachHis/66a44a24-9f87-4f73-b5b6-0a3bbb213a59.pdf

-

Hutti Mines using biotechnology to extract gold | Bengaluru News - Times of India

-

Gold Mines In India: The Untold Story - Jar: India's No. 1 Gold Savings App

-

Centre Proposes Increased NMET Funding for Overseas Critical Mineral Acquisitions

-

Notifications : National Mineral Exploration Trust, Government of India

-

Govt launches India's 1st exploration licence auction for critical minerals - The Economic Times

-

https://mines.gov.in/admin/download/64dc579c4f9e31692161948.pdf

-

https://www.lloydsenterprises.in/wp-content/uploads/2025/07/Intimation-Under-Reg-30-1.pdf