Heavy pledging of over 76% seen this quarter and the company has indicated high financing costs given the large stock carry over. Should this be seen as a big red flag?

1 Like

Decent Numbers by Shriram.

-

Margins in Chemical segments has reached to the lows observed in 2015-2016.

-

Sugar segment has done well this quarter. With the commissioning of 200KLPD distillery, I am expecting steady performance in next quarter too.

-

Finnesta has done well with 15% odd growth at PBIT levels.

Company still trades at a single digit P/E despite observing significant margin compression in chemical segment.

Disc. Invested

We need to see post the new nos (annualised and seasonally adjusted) as chlor alkali spreads are coming from a very high base. Assuming similar spreads there will be a decline in PAT for few more qtrs (maybe 3).

True that but we also need to add the benefit of 200 KLPD distillery that will accrue to the company.

I did some back of the hand calculations for FY 2021 and I am adding the numbers below

Distillery PBIT = 330 Cr.

Chlor Vinyl/Chemical = 525 Cr. (Based on 25000 Rs realizations)

Plastics - 95 cr.

Finnesta - 65 cr.

SFS + Bioseed = 100 Cr.

Add Sugar revenues to above. Since I don’t know how much PBIT can be expected from that business, I am not making any guesses.

This should enable company to earn PAT of more than 600 crore easily for the next year. We have to acknowledge that if India starts picking up then the realizations for Chlor Vinyl business would also increase.

Hitesh Bhai,

Valuation looks attractive, decent quarterly result for Q4. MF are also buying. Bioseed and Fenesta segment looks promising.

Is it good for long term(1 to 2 years) bet?

disclaimer: Invested in last 2 months. View can be biased.

This looks an interesting update :

Need to see how this plays out.

Disc : Invested in Core portfolio

2 Likes

Could you please breakdown how you got those numbers? They seem quite high.

This is intrsting & important at this time, seems Mgmt is allocating cash where its required :

Am sure this should increase margin for the Fenesta.

Disc : Invested in Core Portfolio.

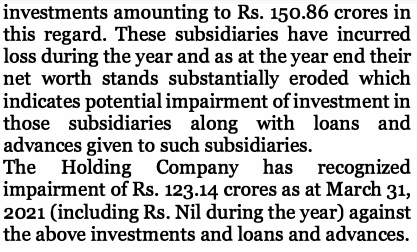

These are the Key Audit matter as highlighted in the

INDEPENDENT AUDITOR’S REPORT.

Can some one help me in understanding this. Specially on the impairment of Rs 123.14 Crores.

Disc : Invested.

1 Like

Good Q1 Result. Also they are increasing distillery capacity by another 120 KLD. But I feel this is just a start of the addition of distillery capacity and in few quarters/next year we may see huge distillery capacity addition (probably highest in whole sugar sector based on crushing capacity). Expansions in other businesses are also going on which means profit growth is for sure. They have good profit each year which can support this expansion.

Disclosure: I have invested in this with good chunk of my portfolio.

Intrsting read !!!

1 Like