Disc - I have trimmed my position in DCM Shriram from 10%+ to < 4% and have completely sold out Andhra Sugars

DCM Shriram Q4FY18 results are out →

Investor Presentation:

https://www.bseindia.com/xml-data/corpfiling/AttachLive/52d2d6e4-2f99-4e6b-9141-bf8745894909.pdf

Results:

https://www.bseindia.com/xml-data/corpfiling/AttachLive/2e66251e-dc01-47c4-9a40-d89698f57eb0.pdf

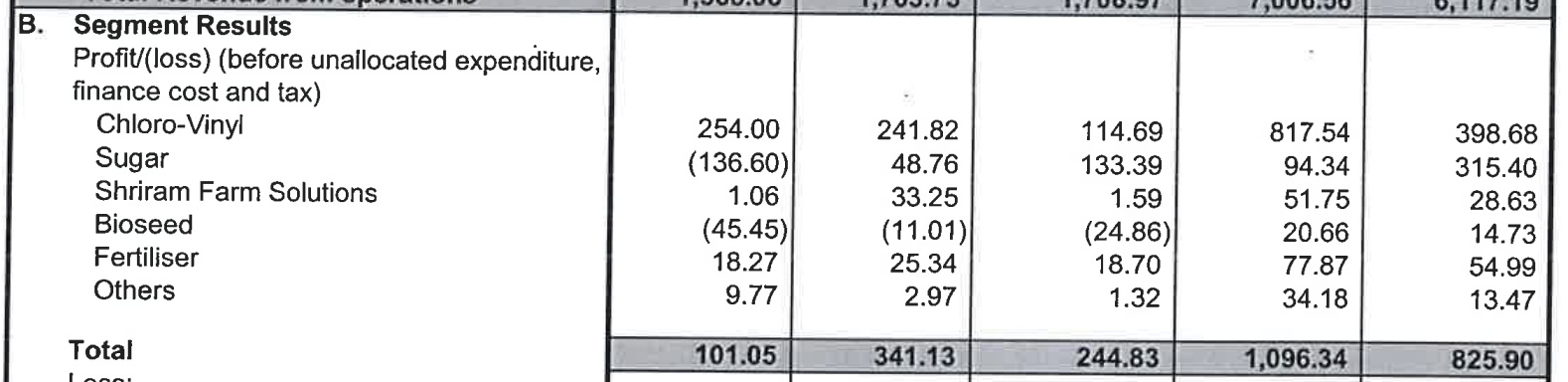

As expected Sugar is in really bad shape. DCM is one of the better players in realizations & efficiency and yet PBIT has gone from 48Cr to -136Cr. QoQ.

Despite such massive hit, I am thinking of holding on to small allocation in DCM Shriram (and ride through the tough times) because of following reasons -

-

Good Management: The management of DCM Shriram is absolutely fabulous. The level of disclosures, shareholder communication and corporate governance is top class. Due to strong background/history, I feel like they are averse to number dressing or taking short term decisions. Even in commodity businesses, they have superior OPM, ROCE, WC management in both Chlor-Alkali and Sugar businesses vis-a-vis competition. Even at the worst of Chlor-Alkali cycle, ROCE does not go below 13%.

-

Capex: Chlor-Alkali ECU is expected to soften due to additional capacities that might come in but I dont think the prices will fall in a hurry. As management described, Chlorine realizations have turned positive. Also additional capacities of DCM might support some moderate level of growth in Chlor-Alkali business. Further the PBIT margins in power business are 60%+. I am hoping power business along with distillery might help to rein in losses at the downturn of Sugar cycle.

-

Two Quality Businesses: Fenesta remains a very good business with a rising brand. The PBIT of 30Cr. for FY18 is encouraging. Although the government pricing action to reduce prices of cotton seeds are negative for GM industry, Bio-seed spends a lot more amount on R&D compared to some other seed companies in this industry. I am hoping that management can scale this business up.

-

Capital allocation: Capital allocation is probably one area where DCM management has a little bit average record due to decision to expand Sugar capacities. Though across an entire sugar cycle (4-5 years), ROCE is 20%. Apart from this one decision, they have taken capital out of Hariyali business, reducing bulk fertilizer business, not growing cement business. They have poured that capital into Chlor-Alkali business which has very attractive ROCE for last 13 years & Fenesta (a standalone player might not have spent enough to build this business due to upfront capital requirements).

I may be completely wrong in holding onto DCM Shriram but it feels like this is the management that can help to create a lot of shareholder wealth.