DCM Shriram Limited is a conglomerate which operates in multiple businesses from Caustic Soda/Sugar/Plastics/Fertilizers/Seeds etc. Most of the business here are commodity and regulated and hence there isn’t much that separate them from others in the same. Instead of going in detail of each business I am going to present a snapshot of financials and how each business has performed over the years.

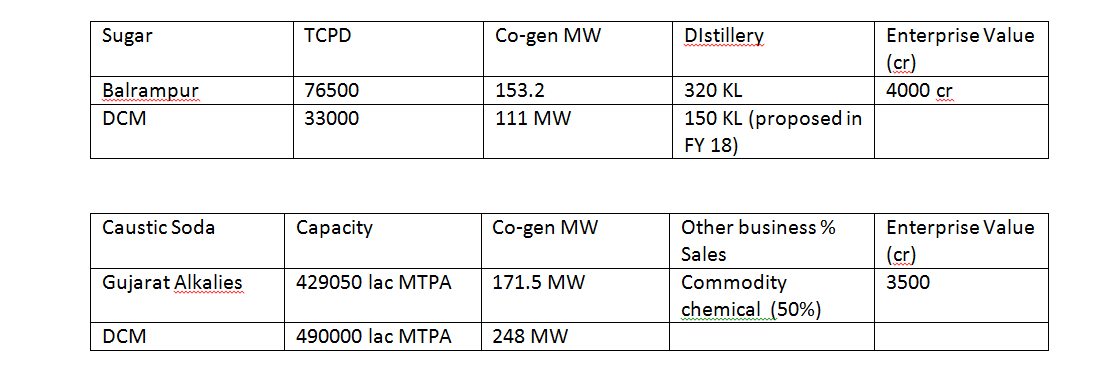

Chlor Alkali/Vinyl: DCM Shriram is India’s 2nd largest Caustic Soda manufacture considering the newly commissioned capacity. India is a net importer of Caustic Soda and its production is constrained mainly because of the by-product chlorine, which cannot be transported over longer distance and the growth of Caustic Soda consumption to Chlorine is in 2:1 ratio. One of the Caustic soda units (Kota) is forward integrated so that the by-product Chlorine can be used for manufacturing PVC or Carbide depending upon realization. Their PVC manufacturing is through Carbide/Acetylene instead of ethylene route which is the general way of manufacturing PVC in India. This results is nigher margins when PVC/Crude goes up and lower margins otherwise. The Chloro-Vinyl business of the Company has highly integrated operations with multiple revenue streams and captive power generation facilities. Chlor-Alkali operations are at two locations (Kota – Rajasthan and Bharuch – Gujarat). The multiple revenue streams enable the Company to optimize operations in a manner to maximize the contribution per unit of power (sell power to grid or used it for production). The following financial data gives a rough idea about the Chlor Vinyl business:

The entire Chlor/Vinyl business has been very good in terms of RoCE, being consistently high ranging 30% to 60% depending upon the capex cycle and depreciation. It is very difficult to imagine a commodity business driving such high return ratio but looking at other players like Gujarat Alkali /Andhra Sugar/ Chemfab it does appear that the industry as a whole seems to have decent return ratios.

Key triggers: The Company has recently expanded capacity by 70% and the sales growth this year is mainly due to volume increase. The company has commissioned the expansion and newer capacity should result it increased sales volume coming year. This should also result in some incremental operating leverage. The company is likely to have a 100% capacity utilization level as the year goes ahead. The Caustic Soda Q4 sales volume have increased by 60% YoY from 58604 MT to 93731 MT. The entire Chlor Vinyl division sales have gone up from 330 cr to 455 cr YoY in Q4. The company is expanding its chemical division in Kota by incurring a capex of 100 cr.

Key Risks: Caustic Soda is a global commodity. Any appreciation in Rupee can result in imports getting cheaper and realizations going down. Also Caustic Soda production is heavily dependent on power and in turn Coal prices. Any changes there can impact input prices significantly. Gujarat Alkali has plans of increasing capacities significantly. As other commodity industries a supply glut can result in realization coming under strain.

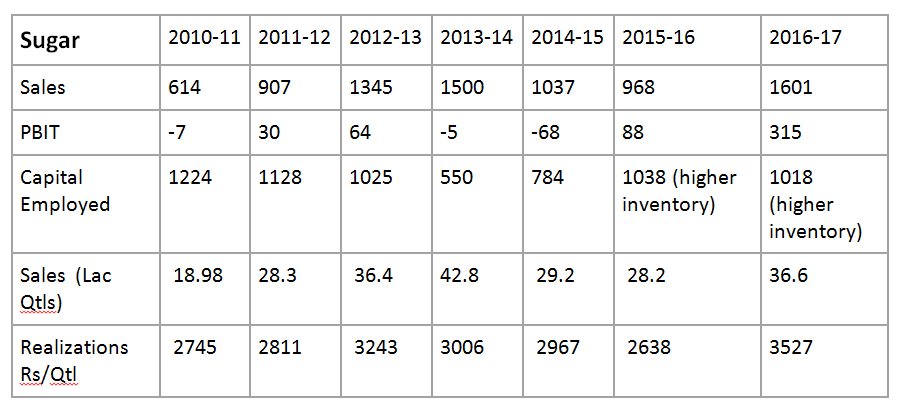

Sugar: There isn’t much that I can write about Sugar which is not covered in this forum on the Sugar thread. The current economies make the business look very attractive hiding the extreme cyclical nature. DCM Shriram is one of the most efficient as far as recovery % is concerned and has managed the debt and balance sheet well.

Other than the sugar prices the key drivers for profitability is the recovery rate. DCM’s recovery rate has been among the best in industry.

Key Points: The company has not increased sugar production capacity, but has constantly upgraded itself. It has also add co-gen and has currently adding a distillery. The crushing capacity has remained at 33000 TCD in last 7 years.

Key risks: Sugar is regulated commodity and has a direct bearing on the farm community. Both the cntral govt and state govt defines MSP/Subsidies. Wholesale sugar prices have fluctuated between Rs 21 to Rs 40 in last few years. As can be seen the current return ratios hide the pain that sugar companies has gone in previous years.

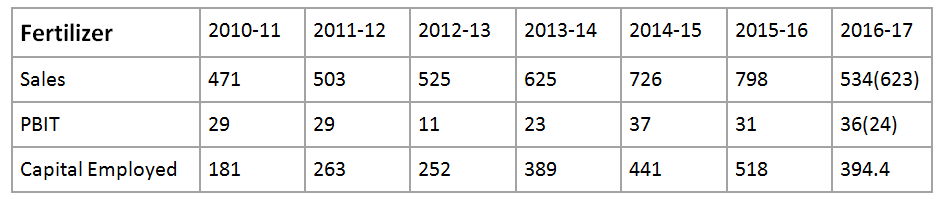

Fertilizer (UREA): The company has a capacity of 3,79,500 TPA of under the Shriram Brand. It is a highly regulated industry where the government determines everything from raw material sourcing to conversion price to subsidy to import. The returns generated by the industry has been sub-optimal and has led to closure of lot of fertilizer factories. The following are the financials of this division:

Key Points: One of the major issues here is that the government subsidy remains pending for over 6 months resulting in high working capital. The govt is current testing a DBT (direct benefit transfer) where the subsidy can get credited within 15 days of farmer buying urea. The pilot program is running in 20 districts and if it succeeds it will be slowly ramped up in rest of the country. The company has not increased its urea capacity in last 7 years.

Key risks: Highly regulated, capital intensive agri sector.

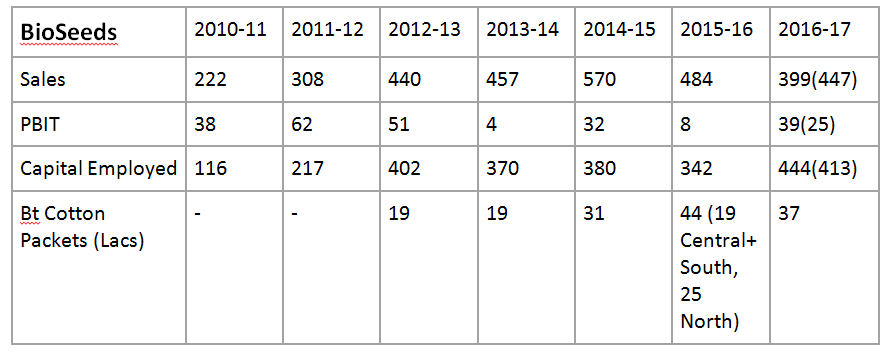

BioSeed: Bioseed business is intensely research based and is diversified across key crops (Cotton, Corn, Paddy and Vegetables). India is the key market with presence across all above crops. International presence is in Vietnam , Philippines and Indonesia wherein the key crop is Corn. The performance of the business has seasonality, with Kharif being the major season in India. Out of total sales roughly 60% are from Bt. Cotton licensed from Monsanto. The company also sells GM corn in international market with technology licensed from Monsanto. The company in the last few year has invested 8-10% of revenues into research. The Company is focused on strengthening the research activities by strengthening its internal capabilities and forging alliances with State Universities, International companies and Universities etc. The company has taken several steps to strengthen its Biotech program so as to leverage that opportunity as and when it arises in India. The company has around 30% of cotton seed market in north India with Brand Names Yuva, BioSeed 100, BioSeed 105, BioSeed 6588 and Bindass. The company has been able to enter Maharashtra and parts of Telangana and is looking to increase its footprint there. The following are financials of this division

Key Points: Bt Cotton industry is regulated and heavily dependent on the monsoon with a markt size of around 5 Lac packets. The company does seems to have some edge in technology and s also working on field trials of GM Corn in India. The current season cotton acreage is expected to go up by 8% to 10%.

Key risks: Highly regulated, dependent on Monsanto and limited opportunity size.

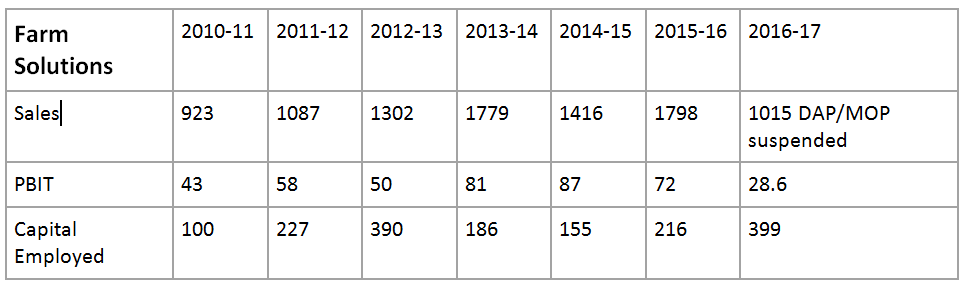

Shriram Farm Solutions: The portfolio comprises Value-added products such as Seeds, Pesticides, Soluble Fertiliser, Micro-nutrients etc. along with Bulk Fertiliser (SSP). This business is seasonal in nature.

Key Points: Company does not have a manufacturing presence but is majorly marketing and distributing products in different segment.

Key risks: Dependent on monsoon.

Other Business:

Along with the above business the company is also into other business like Fenesta, Cement (small cement plant mainly to handle waste generated by Carbide ) and Hariyali Kisan Bazar assets which sells fuel and the PVC Compounding business which makes advance polymers in tie up with WestLake (earlier Axiall 50:50 venture).

Most of the business that I have mentioned above is commodity, regulated and cyclical in nature and generally companies like this have high working capital and mediocre return ratios. The promoters consistently incorrect capital allocation decisions throwing good money after bad money. What got me interested in Shriram is Fenesta:

Fenesta:

Fenesta Building Systems manufactures and sells UPVC windows (Un-Plasticized PVC) and door systems under the brand “Fenesta”. It offers complete solutions starting from design, fabrication to installation at the customer’s site. The product has gained acceptability across the nation with higher consumer recall and the brand has become synonymous with UPVC windows.

The business caters to 2 segments.

- Institutional segment/Developers segment which comprises of residential including Group Housing and Villas and Commercial building.

- Retail Segment which includes the new construction and replacement market

UPVC doors and windows are one of the fastest emerging segments and have gone up from a market size of 0 to 1500 cr in 10 years. Fenesta is the most recognized brand in this segment with around 20% market share. The company manufactures UPVC at its Chlor-Vinyl plant at Kota (Fenesta division can independently source it) which is used in manufacturing the doors and windows. The business has set up self-owned Fenesta branded showrooms along with dealers and distributors in nine cities across India. Fenesta is now “The Superbrand” in Windows & Doors Industry in India. In my discussions and Scuttlebutt with builders an interior designers it was quite evident that Fenesta is considered as highly aspirational with very high quality parameters like sound-proofing, resistance to humidity etc. The key competitors for Fenesta in this segment are LG, Rehau and cheaper Chinese imports. But they all fall behind in pricing, quality and service. Fenesta windows have 10 years warranty and can be installed in a day. The company has been reluctant in disclosing the numbers of Fenesta and has only provided sales numbers and has clubbed it with other business. The business turned PBIT level +ve last year. The key reason behind Fenesta’s quality is the process by which UPVC is manufactured. A Carbide/Acetylene process used by DCM (only company in India to make PVC with this route) results in a high quality compound resulting in high quality windows.

Business Quality: Although the management does not provide numbers in terms of profitability or capital deployed it has consistently said that it is not a capital intensive business. The current capacity is 18000 windows per month and the management is expanding it to 32000 (75%) windows per month with a capex of 18.5 cr. which implies an asset turn of over 11 times on expanded capacity. Further there is 10% advance on booking and the rest of it is paid at the time of delivery implying a very health working capital cycle. Management has indicated a margin of around 7% but there is a large amount of advertising and marketing expenditure used for building future business which significantly reduces the margins.

Risks: The management has little experience in brand building and the dynamics. Unlike CPVC which is patented there are multiple UPVC manufacturers and there are a number of small brands and there is very high competition.

Management :

Capital Allocation: The record here is not great but is improving. The management ventured into a rural retail business and expanded it very quickly taking undue risks. This resulted in heavy losses and the business had to be called off. The management still carries around 200 cr of fixed assets from this business. Further the capital employed in Fertilizer and Bioseeds has gone up significantly with very ordinary return ratios. To their credit they haven’t expanded sugar and fertilizer capacities.

Fairness towards minority Shareholder: DCM Shriram sold land to DLF in 2007 and the entire amount of 837.5 crores was brought into the books of the company.

Accounting: There have been multiple instances of conservative accounting practices followed by management. In their seed business the company paid taxes taxes citing that the case is in court. Also the company paid full royalty to Monsanto last year again citing that it will wait for final court order. The company. In another example the company refused to bring the subsidy declared by the government on cane into books until there was an official notification.

Valuation:

It is extremely difficult to value a conglomerate that involves multiple business which are cyclical in nature. Some of the general parameter used are sales to mcap (.5 to 1 entry 1.5 to 2 exit), replacement cost, capital employed or peer comparison. I will be doing a peer comparison in detail but a rough comparison for various business gives the following:

Without going further it is quite evident that at a MCap of 5600 cr DCM trades quite cheap when compared roughly to its other peers and discounting the Fenesta business. In the next few years Fenesta could possibly be the most defining business of DCM Shriram limited.

Discl.: Invested. Forms more than 5% of my portfolio. This is not a recommendation and I am not a SEBI registered analyst.

Financial highlights:

Annual reports:

http://www.dcmshriram.com/annual_reports

Presentation/Conf Calls

http://www.dcmshriram.com/results_presentations

Fenesta:

https://www.youtube.com/watch?v=yONEd1gI6w8

http://www.prismma.in/upvc-doors-and-windows-leading-companies/