Quite a good set of results. Hope they can continue it going forward.

3 Likes

in Banks and NBFCs anybody can double the loan book if they want to. But very few can do so while maintaining the asset quality.

3 Likes

Interstingly, when all the banks are making new highs DCB is still lying low. I find it bit surprising as fundamentally and operationally this bank is on a strong footing. Is there some concern which is keeping the investors away ?

DCB bank break a new 52-week high today… Trading at Rs. 144.60/90 levels… up 8.70% in a day.

What has been the key development that is causing this trigger? Any insights?

Marcellus exited the stock in Aug 2022

I can’t think of a better development for a stock too go up ![]()

3 Likes

Can somebody explain why this bank has low p/b compare to its peer? any management issue?

No management issue, in fact the recently retired MD, Mr. Murali Natarajan ensured that the bank had the highest levels of transparency of operations and financials of the company. It’s just the growth has been quite slow and is still a small bank for quite some time now

I have had bad customer experience with most banks and DCB is no exception. They launched new product - niyo app, may be it’s not that new, but the point is that if you don’t back it up with great customer service, ppl will never do business with you. With all this digitalisation, you cannot replace great customer experience just with an app. The idea of using technology is to make the process of using product simpler and convenient for the customer and not save money by having fewer call centre agents. This is the issue with almost all the banks. Kotak is slightly better than other banks.

1 Like

Anyone else started to receive text message for loan from DCB bank, this number I rarely use for other purposes (just used it for account creation), so high chance they got this number just caused I purchased this stock, needless to say I am disappointed and irritated both as stock holder and receiver of the texts.

I dont pick up calls genrally on that phone (if it is unknown), probably they are calling too but cant tell for sure.

Hey guys,

Recently I called on a DCB bank customer care number asking for unsecured loan just to check their response. Madame who received the call politely declined it saying they only do secured lending. I want others also in the community to try and give feedback.

Thanks

Hi…Today I have taken a position in DCB bank. I think it is most undervalued bank currently in private sector. Reasons for its undervaluation is its lower ROA. But in my opinion , nothing much is to loose in DCB bank from its current market price.If thinks improve from here in next 3-4 quarter then chance of gain will be quite substantial which can beat easily nifty 50 returns.

Dis: buyed @ 119.61 and its 2% of my portfolio. All views are invited.

1 Like

Discussion Topic: Evaluating DCB Bank’s Long-Term Lending Strategy

Hello DCB Community,

I recently had an insightful conversation with a DCB Bank manager about the bank’s approach to lending, particularly to MSME clients. He mentioned that DCB Bank is not very aggressive in its lending practices. Instead, they focus on building strong personal relationships with their MSME clients, offering loans that are mostly collateralized, with less stringent income verification compared to larger banks. The paperwork is kept relatively easy, and the bank isn’t overly concerned about CASA (Current Account Savings Account) ratios or deposits, as they offer higher interest rates than many competitors.

My Questions to the Community:

-

Reliance on Personal Relationships and Collateral: The bank’s strategy seems to rely heavily on personal relationships with clients and the value of collateral rather than strict income criteria. Do you think this approach is sustainable and prudent for long-term success? Is it really as safe as it seems to base lending decisions primarily on collateral value?

-

Ease of Selling Collateral: The manager mentioned that since the lending is mostly collateralized, they are less worried about risks. However, how easy and practical is it to sell collateral in case of defaults, especially in challenging economic conditions or with specialized assets like machinery? Does relying on collateral provide enough protection in the long run?

-

Long-Term Moats for DCB Bank: Beyond this lending approach, what do you see as DCB Bank’s long-term competitive advantages (moats)? How can the bank sustain its growth and differentiate itself from larger players and fintech companies in the evolving financial landscape?

Looking forward to your insights and opinions on whether this strategy can help DCB Bank thrive in the long term or if there are potential risks that need to be addressed.

Thank you!

2 Likes

It is more of tactical buy with lower downside in this market. Dcb operates between 120-160 range. I will wait for my prices to come in 3-4 quarter and look for management actions whether they can deliver what they are saying.

There I decide whether to hold or sell. Suppose if it goes lower from this point, I will deploy my additional cash reserves.

Moreover chance of loosing money is less and probability of gaining appears to be more.This is my way of seeing the things.

1 Like

You are correct, sir. I also see potential here, but I want to understand more about how this bank operates. My concern is that, based on my assessment, they seem less aggressive. How will growth come in the future if they maintain this approach?

1 Like

Have been invested for some time and track on spare times. I don’t think we’ll get great ROE from this bank like we see in other private banks. Having said that, a very good possibility of consistent 12-13% ROE is highly possible in near future. The management’s comments of 14% ROE from 1% ROA doesn’t look feasible I feel. Future is obviously open. At this point of time, small ticket sizes of the loans, mostly doing collaterals and ability to recover slippages has been evident. Assuming company won’t grow like HDFC Bank during its younger days, at the same time, they can still grow at a reasonable rate, and I feel current valuations are very cheap for a company with steady growth and possibility of higher growth in the future.

Disc: Invested.

5 Likes

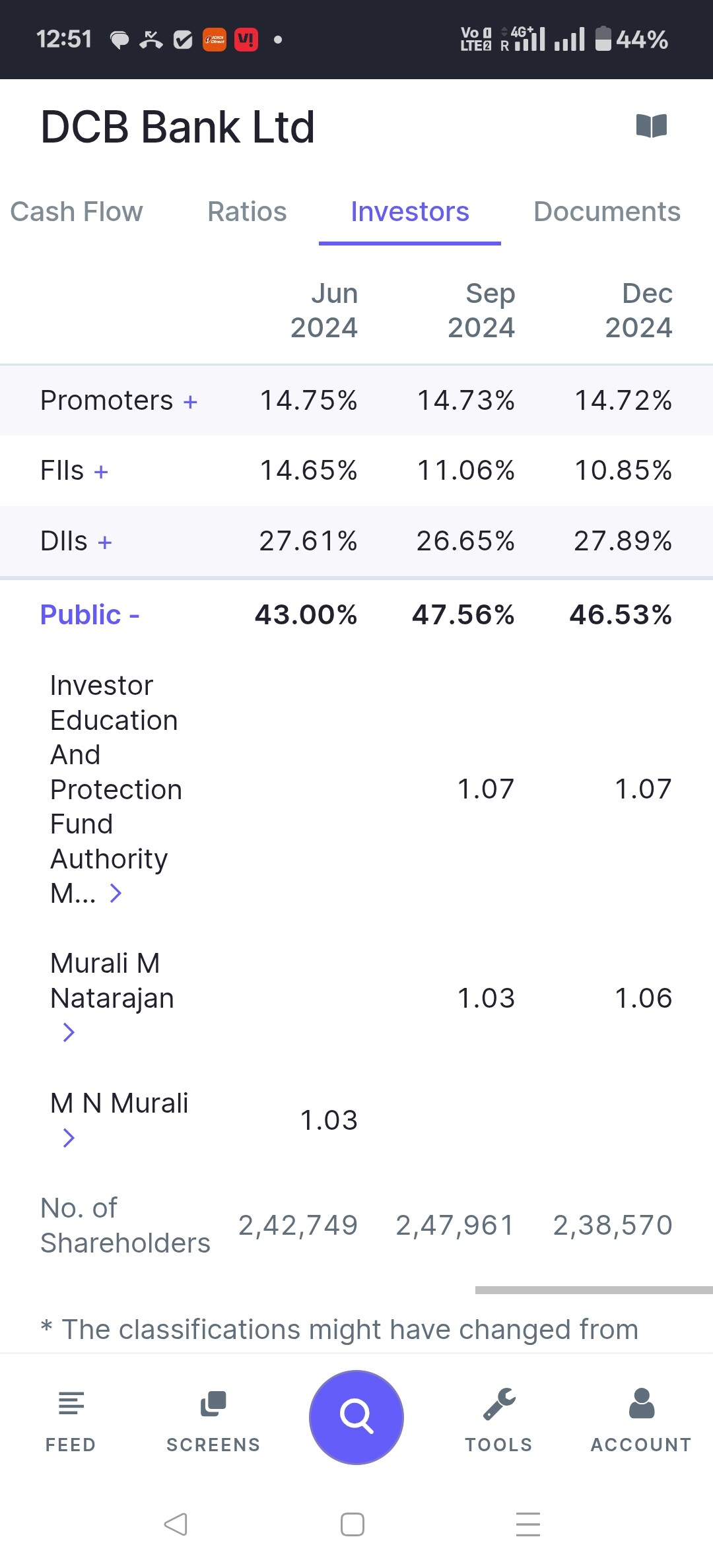

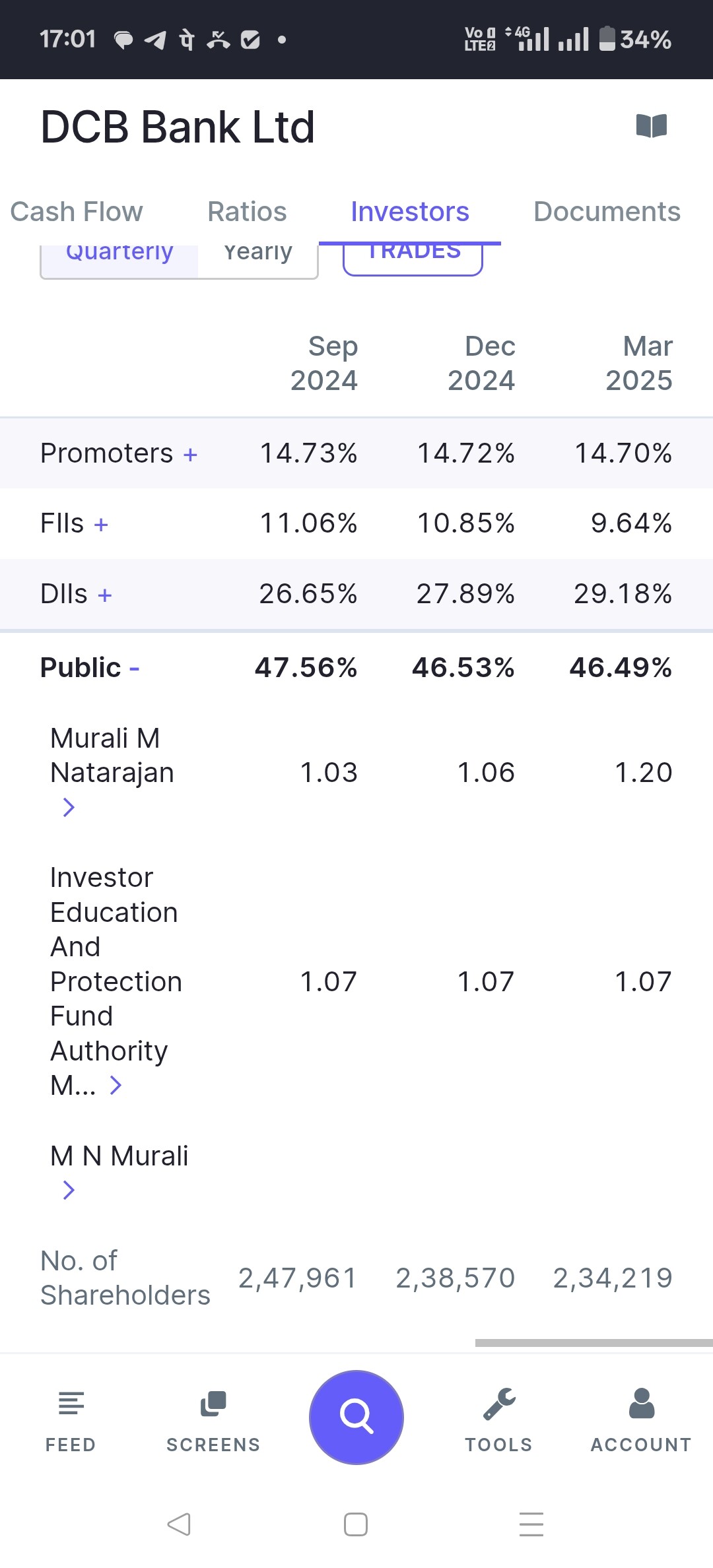

Insider Confidence: A Strong Endorsement for DCB Bank

Former DCB Bank CEO, Mr. Murali Natrajan, has increased his stake in the bank from 1.03% to 1.06% in the December quarter. This move signals his continued confidence in the bank’s future and trust in its current management, even after retirement. In contrast, at IndusInd Bank, both the CEO and CFO offloaded their major stakes at the 52-week high, and soon after, financial irregularities began to emerge. This highlights the significance of insider actions as a key indicator of management’s belief in a company’s long-term prospects.

1 Like

Can you guys share your views on whats the strong moat of DCB bank as compared to others?

Only one thing which I doesn’t like for this quarter results is the rise in NPA. Management is telling that rise in NPA is due to MFI segment, unsecured Direct assignment eg . Student loan and secured direct assignment like mortgage.

NIM falls to 3.2% can be overlooked due to repo rate cut of 100 bps point. However increase in credit cost will ultimately affect NIM.

Overall mixed results. Can be great if NPA doesn’t get increased in this quarter.

Disclaimer: Holding and biased. Will love to hear other fellow investors opinion.

2 Likes