Why data Center theme is not picking up pace as expected ? What are the Hurdles ?

It has picked up pace, it’s in the earnings and sales. Stock price wise, I think valuations are hurting those. Theme had a mega run b/w 2023-Sep 2024.

3 Likes

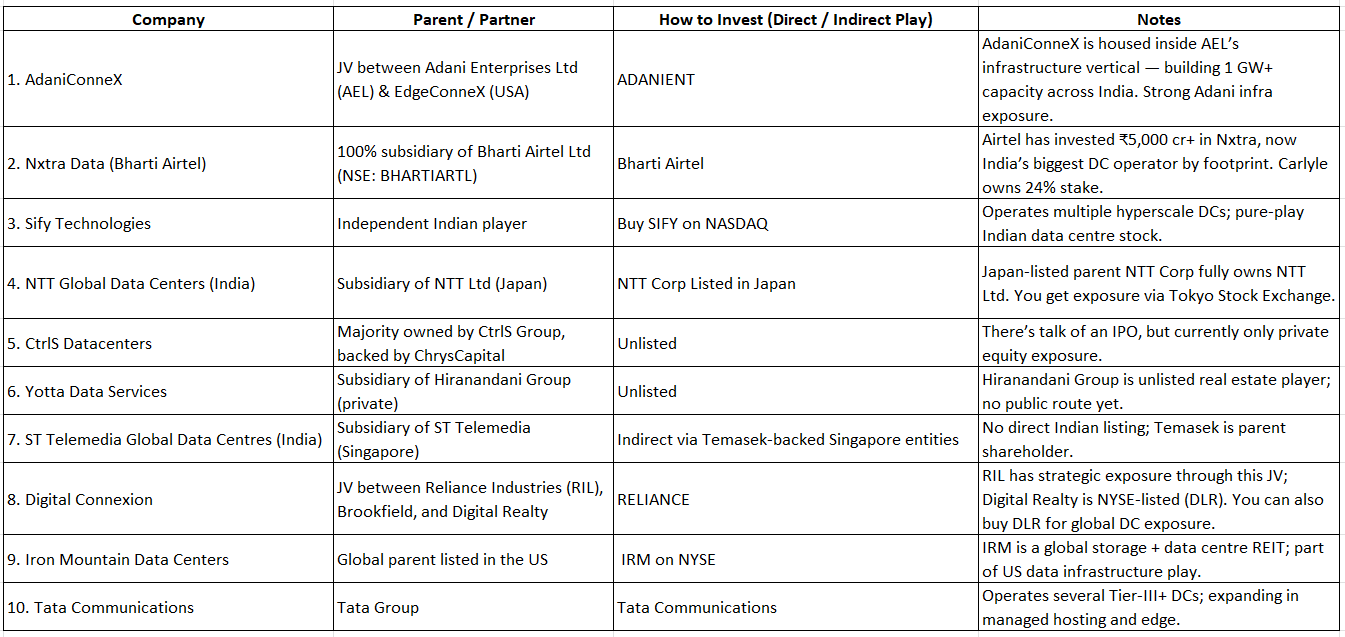

Can anyone explain what role in the data center ecosystem is being played by Tata communication and Orient technologies. Cloud & Infra by Tata comm and System integration by Orient tech is fine…but what about their expertise level, the involvement, the contribution of data center business to their overall revenue?

Also, among cooling solutions, I see all unlisted unknown players name in top lists…no mention of good old Voltas (Tata ecosystem), Hitachi AC (erstwhile Johnson control JV and probably now Bosch company) although their individual website does mention somewhere their intent on data center cooling business…Is data center cooling technology highly innovative and needs focused nimble players?

Also, read that Castrol has initiated some liquid for cooling solution specifically for data centers…

I see good opportunity in cooling & power solutions & maybe infra/cloud/connectivity rather that system integration part which maybe crowded, unless we have a very focused player.

I may be wrong

Disc: Invested in Tata communication, Hitachi AC hence maybe biased. Not a buy/sell recommendation. Post only for learning purposes. I can be wrong in all my assessments

2 Likes

I think one of the major reasons is commissioning time. A hyperscale or Colocation takes much time to be constructed & commercialized. The Breakeven period for data center per MW is also around 4-5 years since it is very capital intensive. And India is still at a very less capacity currently. So in order for things to reflect into earnings it might still take some time. Also, why we don’t see a major pickup maybe because major pure play data center companies are unlisted.

Do let me know if you found some things for cooling systems.

5 Likes

Good read on data centers.

9 Likes

I fully agree with the Article, AI and datacenter investments require clear profitability and sustainable cash flows beyond hype, unless revenue growth can cover depreciation and capex, investor value will erode despite short-term excitement. Thanks For Sharing this Article

3 Likes

They have released part 2 of the article that develops on the theme

4 Likes

In 2017, India consumed 8 Exabytes of data. Today? 229 Exabytes. That’s the engine for the $50,000,000,000 data center rush. It’s not just 5G. It’s millions of people streaming, paying, and demanding instant AI results. The infrastructure boom hasn’t even started. This is the new gold rush.

7 Likes

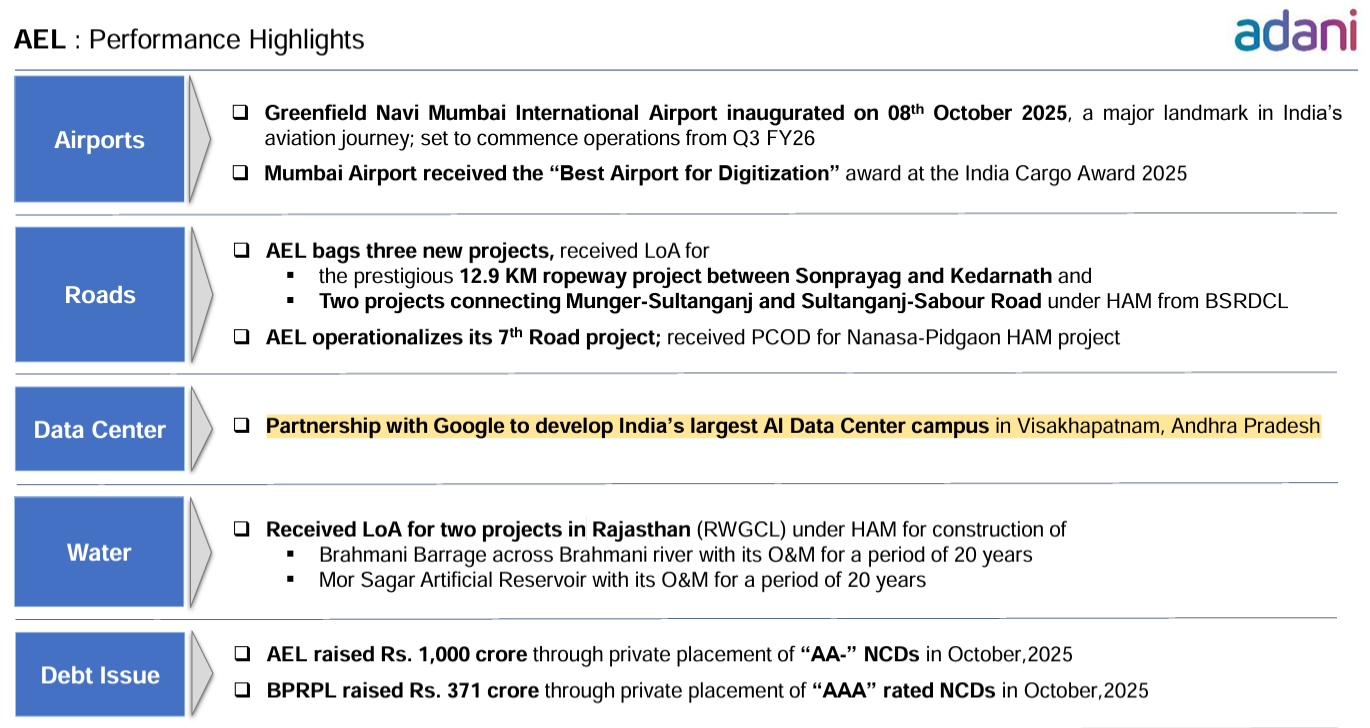

Wouldn’t recommend Adani ENT to get stake in AdaniConnex. Even Jio Platforms is going to be an IPO, existing shareholders won’t get anything. Same is likely to happen for any Adani listing.

Plus the Revenue from DC is quite low as compared to the commodity trading business of ENT.

1 Like

Update: Just Came to Know

Sify Infinit Spaces Ltd. filed DRHP with SEBI.

It’s part of Sify Group, one of India’s leading providers of data center colocation services. As of June 30, 2025, the company operates 14 data centers across 6 cities —Mumbai, Chennai, Noida, Hyderabad, Bengaluru, and Kolkata—with a total built IT power capacity of 188.04 MW.

10 Likes

The hype of data center is currently underway. Do not forget telecom and infrastructure boom and present status of companies. You have to be extra concious in Indian market while selecting stock.

5 Likes

Went through the thread. Interesting observations shared by you @karanshah137. I have this doubt that are there any players in the data center supply chain in India that have strong moat and ate definitely going to grow if the data center grows. Like in Capital Markets we know that if capital market participation is going to increase definitely BSE is going to increase, are there some similar companies like that in the supply chain (might be the 2 order effect beneficiaries too)?

2 Likes

@Milan_Vishnoi A strong moat, like BSE in the Cap Market, is Hard to find in the Data Centre Value Chain. It is a regulated Duopoly / Listed monopoly platform. And Backed by the COVID BOOM. In the Data Centre, We Just Have AI BOOM, no Monopoly as of now, and I don’t think there will be any

Currently, the closest BSE-equivalent is Colocation/ data centre operators, such as those mentioned in the Above Threads, because every MB of data, every AI inference, and every cloud deployment pays rent to them.

Their business is asset-heavy upfront, but once built, they collect steady “rental yield” for 10–15 years. High entry barrier is Another Advantage for Cloud Service Providers (Hyperscalers)

8 Likes

HFCL promoters claim multi year growth but keep selling their stake. In last 10 months they reduced 6% stake. Massive 700 crores worth. Don’t know how to trust them

5 Likes

That’s Correct, I posted for the OFC Indirect Play for Data Center, which is a big opportunity not particularly meant for HFCL alone

1 Like