agreed, but Danish Power IPO price band was ₹380 per share and it is near, I am now more intrested to see execution, for fresh entry those who entered early thier opinion may vary. Disc. not holding

Any public info on what is the capacity enhancement for which capex is being done ?

2 Likes

Good thread on Danish power

4 Likes

In their drhp , They have mentioned Shilchar , Indotech and TRIL as peers

1 Like

check here

- Inverter Duty Transformer:used in power electroncis. (solar, wind, and VFD applications) convert low voltage AC to medium voltage AC.

- Power Distribution Transformer: used in power to end-users by stepping down medium voltage (e.g., 33kV) to low voltage (e.g., 415V).

- Power Transformer: Used in transmission systems to step up or step down high voltages (e.g., 110kV to 400kV) for long-distance power transfer. Handles large power capacities.

So i think their peer could be shilchar. TARIL, Indotech operates in higher power tranformer segments.

4 Likes

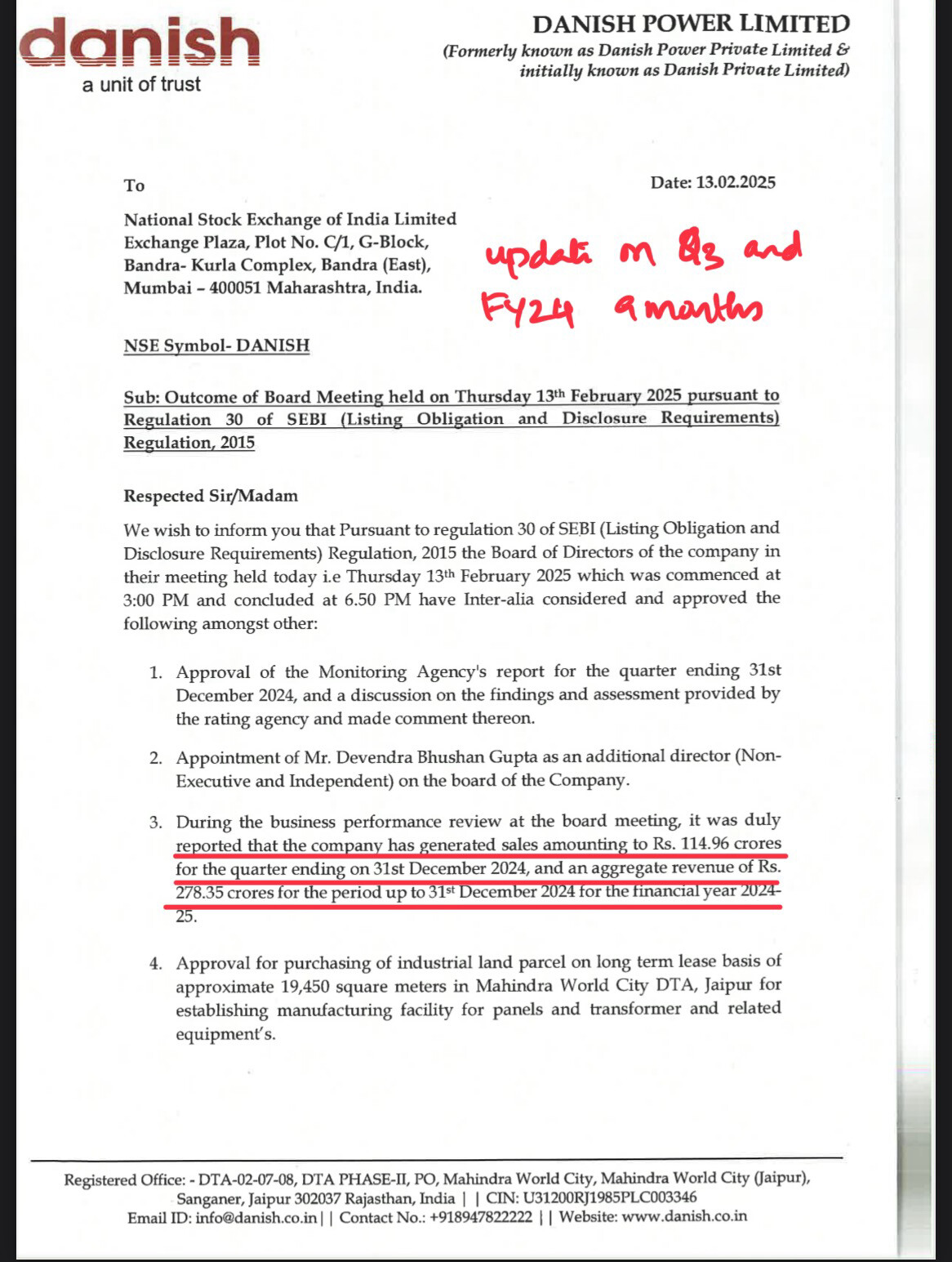

Update from Danish power.

**Q3 revenues c. 114 cr and 9 months FY 25 revenues c. 278 cr. **

**FY 24 revenues were ₹ 331 cr. **

If they do c. 125 cr in Q4 ( Q4 usually better ) then FY 25 they will end up with Rs 400 cr. ( Not a very exiting growth ) .

**They also notified exchanges on receiving an order for C. 100 cr from Waaree renewables to supply IDT transformers within 8 months . **

Key monitor-able is capacity expansion slated for Q1 FY 26 and current capacity utilisation.

Disc : Invested

5 Likes

Indotech’s Parent company Shirdi Sai electricals has also forayed into Inverter duty transformer (pretty much same capacity as Danish Power), which means sooner than later Indotech should get that technology transfer.

IMO Indotech is also valuation wise better placed than it’s peers.

1 Like

Management in the past had said that they are running near full capacity utilisation and hence growth will be missing till capacity expansions goes live

1 Like

But with new capacity the company capacity will be 8000 MVA or greater

With the Rs 100 cr order from WRTL how much is the order book as on Dec I think it will be near to 480-490 Cr. If anybody know it then it will be very helpful.

1 Like

What will be the total capacity after expansion , will it be 8000mva or 11000 Mva? There’s alot of confusion regarding the same , IPO document mentions 8000MVA whereas some reports are claiming 11000 MVA.

Hi,

This is the capacity expansion plan with timelines. I believe this was given as an exchange filing .

As per this Q1 should have 8000 MVA and Q3 11000 MVA.

Sharing the peer capex plans also for quick comparison.

This is from some research report on transformer sector 2-3 months back

13 Likes

1 Like

Not seen the 11,000 MVA capacity figure in any of the exchange filings.

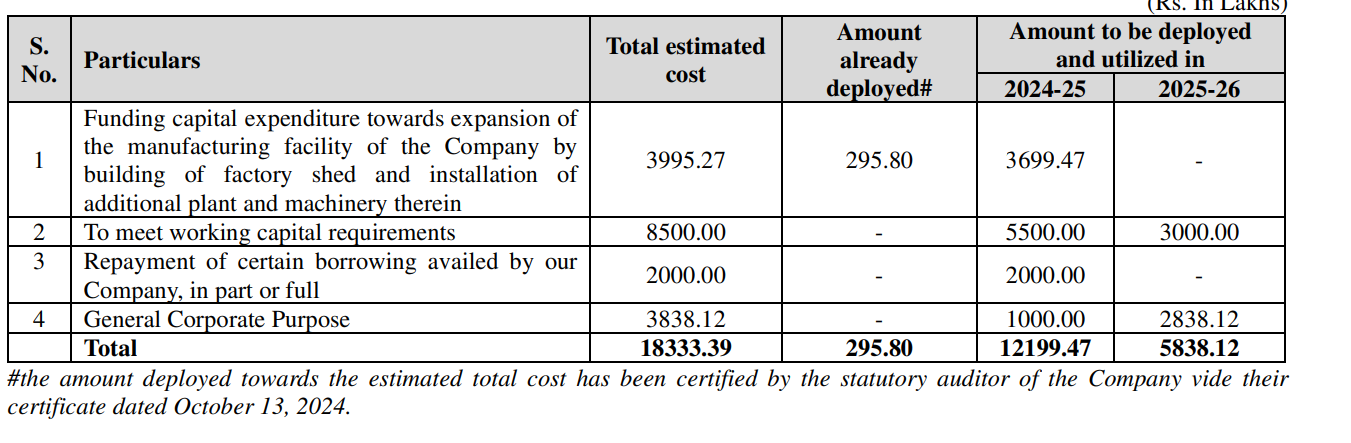

Company was supposed to deploy 37 crores for CAPEX of new facility in FY 25 itself as per the prospectus.

However as per the latest balance sheet (Mar 25) only 13 crores can be seen CWIP.

If anyone is aware about the status of CAPEX, please update. Thank you.

3 Likes

Danish received fresh order for Inverter Duty Transformers - order value 52 Cr inclusive of 18% GST

4 Likes

Danish Manufacture transformers of mainly two types: a) inverter duty transformer b) power transformer .

Demand for inverter duty transformers is increasing rapidly and the company is rapidly increasing its capacity and at the same time its utilization % is also increasing with every result . Its peer company is Shilchar tech because it also manufactures the same type of transformer . Shilchar is a big company and performing well, especially its export segment . So there is an option value with the danish that it can also start exporting after 2-3 years , however domestic demand is itself sufficient for these manufacturer .Inverter duty transformers are used in renewable energy projects like power and wind projects. OPM - 17-18% and PAT margin is 15-16 % . Also shilchar tech FY 25 revenue is 623 cr and OPM is 30% while danish power revenue for FY25 is 425 and OPM is 17-18% while MCAP of both companies is drastically different like for danish it is 2000 cr and for shilchar it is 6000 cr. Right now the capacities are being developed rapidly by companies but the situation of oversupply is less likely for the next 3-4 years as continuous demand is growing in the export market and the real demand in India is yet to come.

Currently the waiting time for transformers is 12-18 months as on 17 aug 2025 . Kay cee energy and infra ltd management also looking to establish a manufacturing unit to take advantage of this .

8 Likes

The results seems to be ok.Does anyone know why market is punishing the stock.if anyone has access to the con call please share