Valuations seems attractive no doubt but i feel below 3 reasons is what is worrying investors in CIL 1. captive coal mines by coal india’s erstwhile customers seems a big concern, also. 2. Last year since Supreme court allowed that States can also have seperate Royalty charges, market maybe wary of royalty/cess increases. Plus 3. the good growth shown by renewal energy shows future growth on coal may be less than in the paat.

5 Likes

Future do belong to renewables but that future is at least 10 yrs in India for coal degrowth to happen (Because energy demand is growing at 5% but renewable energy is growing only at 10%. So coal still have a long way). By that time, CIL would have paid us back since P/E=7.

4 Likes

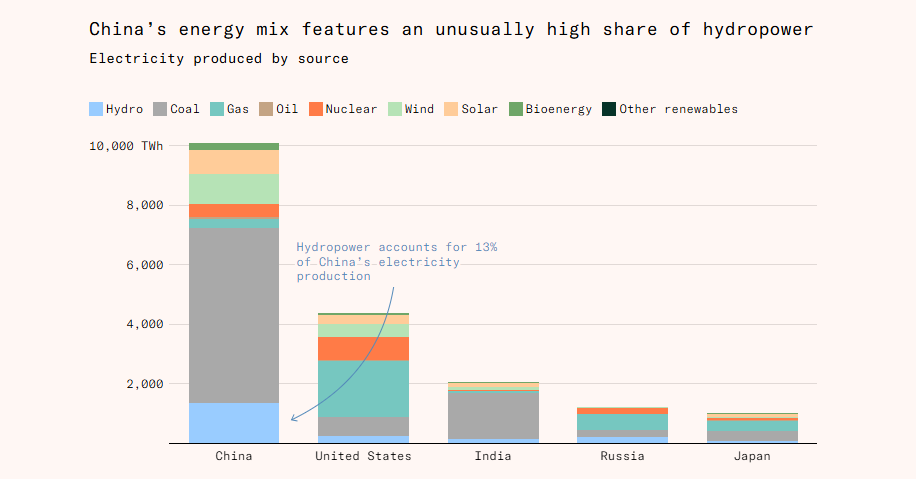

These source of energy is just like food habits. one eats whats easily available. US & Russia are rich in natural gas whereas india has negilible. Solar suits India due to climatic conditions but solar was not growing at a rapid pace untill last 3 yrs.

5 Likes

Even though Coal may remain a major energy source for India for the next decade or so, but it seems Coal India will continue to loose its market share. From the latest quarterly results - both FSA Volumes and E-Auction Volumes dropped; E-Auctions prices also dropped.

- Volume drop shows competitive intensity increasing; NTPC and other customers using their captive mines for their coal requirements.

CIL may continue to give good dividend yield and unless it is able to grow in other areas (other critical minerals - rare earths, etc) using its mining expertise, i fear it will just act like a bond, and stock value maybe stuck in a range till then..

2 Likes

CIL’s Coal Offtake is reducing at an accelerated rate.

-5.9% for Oct 2025 as compared to Oct 2024

-2.4% for Apr-Oct period as compared to Apr-Oct 2024

Disclosure: Invested

2 Likes

Though the production has increased by 1.1% this month over Nov 24; however offtake which matters more currently since there is no coal shortage, is still down compared to Nov 24, also year to date comparison with last year is also down approx 2% however from Oct25 to Nov 25. it has increased some 16.5%;

1 Like

CIL operates through eight subsidiaries, namely Eastern Coalfields Ltd, Bharat Coking Coal Ltd, Central Coalfields Ltd, Western Coalfields Ltd, South Eastern Coalfields Ltd, Northern Coalfields Ltd, Mahanadi Coalfields Ltd and Central Mine Planning & Design Institute Ltd.

BCCL and Central Mine Planning & Design Institute Ltd are set to be listed on stock exchanges by March 2026, with all preparations completed, sources said.

1 Like

I am curious to know whether listing subsidiaries will unlock value and increase in transparency.

Listing of HDFC AMC or HDB Financial Services might have created more value for share holders, since HDFC / HDFC Bank was holding 100% in it and After listing generally stock market adds to the value by raising the market cap of HDFC AMC and/or HDB.

Is this principle applicable for COAL INDIA as well ? How it will increase transparency just by listing them as separate stocks is not fully clear to me. May be, I am missing some thing. Eventually the Management Control may still remain with COAL INDIA so how it adds to transparency? Looks like optical gimmick to me.

Also, if all subsidiaries are listed as separate companies, What will remain in Coal India? How much revenue and EPS will remain with parent company? Some of these things are not clear.

Note: I may be wrong as my understanding of PSU companies is limited even after holding COAL INDIA for some time.

4 Likes

-

I think listing means each entity gets its own management … and takes decisions of its own vertical.. so may add value.. but need to be seen..

-

as per quick google CIL subsidiaries are like: north, eastern, western, central coal fields..and others

-

All CIL does is COAL production .. even each subsidiary will also do the same once listed as well… coal production.. unlike VEDANTA which is listing with each metal.. like aluminium,oil&gas.. which definitely adds value.. which is not case with CIL… so need to see on value addition.. and if it benefits shareholders..

-

Other subsidiaries which i can see , looks might add value as they are not just coal producers :

Bharat Cooking coal, gasification and chemicals, CIL Solar, Lignite and coal videsh as well..

so these might help shareholders.. -

Already confirmed with SouthEasternCoalLimited(SECL) and Mahanadi Coal Limited(MCL) are getting listed in 2026-27.. so need to see how they add value.. and yes if all listed what is left with CIL .. if all coal fields are made their own entities..

Discl: Invested.. my long term dividend play.

6 Likes

Coal India will be using funds from subsidiary IPOs to fund it’s 16000 Cr Capex.

I’m guessing dividend payout will likely shrink as Coal India is divesting parts of its subsidiary companies however it can be value accretive in the long run as market value of subsidiaries expand.

Neutral in the short term, positive for long term.

Disc: no holdings, tracking

1 Like

CIL latest cash reserves is 99,200 Cr (as per screener and annual rep). So, nt sure if it really needs subsidiary ipo’s money for it..just to capex 16,000 cr.. listing subsidiary may be for easy governance and better visibility etc..

Actually dividend pay may increase.. if it lists subsidiary.. and sell its partial holdings.. Govt can demand more dividend from CIL.

4 Likes

Reserves are not strictly cash. Check cash & cash equivalents.

Fair point. Cash equivalents are 32000 Cr

Ownership will decrease, how will dividend increase? (In short term)

1 Like

Well.. Government often pushes PSUs to pass cash via dividends or buybacks …so the proceeds of listing wont sit with CIL alone.. govt will surely take away in form of dividend..lets see.

1 Like

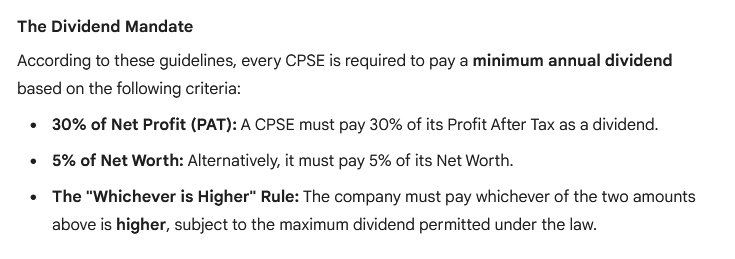

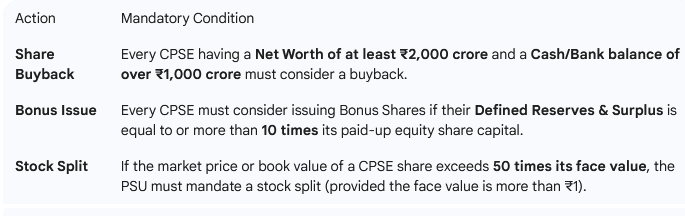

yes,

and this too

from gemini, which quotes Department of Investment and Public Asset Management (DIPAM) Guidelines on Capital Restructuring of Central Public Sector Enterprises (CPSEs).

3 Likes

yes, that is what i m thinking too.. if above conditions followed.. when CIL lists its subsidiaries the proceeds that CIL receive full or partial .. will end up in dividends.. as it lists more subsidiaries each year.. dividend flow will be there..

2 Likes

Something to watch out for starting 2026 - EU’s CBAM (Carbon Border Adjustment Mechanism) could have second order impacts on Coal India.

The European Union’s Carbon Border Adjustment Mechanism (CBAM) is a climate policy that functions as a carbon price on certain goods imported into the EU. Its primary goal is to prevent carbon leakage, which occurs when EU-based companies move production to countries with weaker environmental laws to avoid the costs of the EU’s domestic carbon market (the EU ETS).

Importers will be required to purchase CBAM certificates to cover emissions.

CBAM focuses on highly carbon-intensive sectors where the risk of leakage is highest:

- Iron and Steel (and certain downstream products like screws and bolts)

- Cement

- Aluminium

- Fertilizers

- Electricity

- Hydrogen

Disc: Tracking

4 Likes

The EU India FTA is stalling on this point. CBAM levies. carbon credits is not something we agree to.

2 Likes