2 Likes

What would be the material impact of this order on CIL is it contestable or final any senior member please share your views

2 Likes

The material impact of the Supreme Court’s verdict on CIL could be substantial, affecting its financial health, operational efficiency, strategic decisions, and stakeholder interests. CIL would need to implement a robust strategy to manage these implications.

So, in an interview in ET, it was stated that total dues for coal India may come to 30k Crores.

Out of this, they indicate up to 24k is recoverable from their clients, and 6k will be from their end. This is the maximum, subject to how state governments levy them, royalty, etc.

Now, this will be over 12 years. Even if we take 30k entirely, payable over 12 years with no interest, etc., it comes out to 2500/yr. The impact is real but manageable. ~ 7% current profits.

The Market thinks it’s a nothing burger, and prices have increased since the decision. You have to analyze the rest.

Disclosure: Invested.

8 Likes

Hello All,

Is Coal India Ltd limited a good option to buy and hold at the moment. Mixed reactions when it comes to energy management for the future.

Pros- Coal dominates India’s energy mix, contributing about 50-55% of the country’s electricity generation. India is both a producer and importer of coal, using it primarily for thermal power plants. (source chatgpt).

Cons- burning of fossil to develop and drive fuel and energy will see a decline in the coming years considering the harm is causes to nature.

2 Likes

Does anyone here tracks this? Its not clear from the news on how much of it is a growth compared to previous year. It would be great to have a trend view of this to take this news as a base for additional entries as right now price is quite low to add more of Coal India.

If anyone here has insights and understanding on it, do share!

1 Like

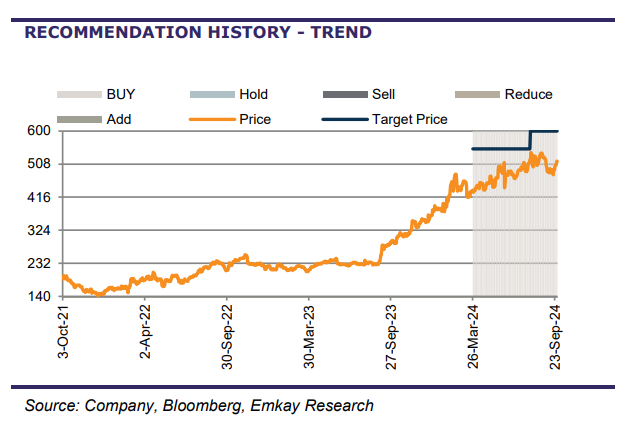

Emkay Research: Buy | TP 600 Rs. (Oct 1 Report)

“Coal India’s production volumes tend to be seasonal with the second quarter of any fiscal year softer than the rest of the quarters. The seasonality factor has averaged 41.4%/58.6% for 1H/2H, historically . Essentially, the production of 341mt in 1H implies full-year production of 825mt adjusted for seasonality , which is marginally lower than our estimate of 830mt and the company’s guidance of 838mt for FY25.” - Emkay Research

Emkay says dont worry about productionn coming down in monsoon months. Coal India is on track to achieve its ambitious target of increased coal prodution this year. The best is yet to come. Q3 and Q4 will be better.

5 Likes

4 Likes

I would be little cautious about Coal India ROCE going forward, as it has reduced Dividend Payout from 60% in FY22 to 42% in FY24. As a result, Reserves have increased from 36,980 to 76,567 Crores during the same period.

While this reserved profits will be certainly used for capacity expansion and expanding its Business lines, I believe that, moderation of Coal prices might have mild negative impact on Margins, Net Profits and ROCE will be under pressure.

Market may not elevate its P/B as it did during 2021 to 2024, and further re-rating in the stock could be limited. Margins are still good at about 33% and ROCE is also good at 64% but further improvement could be limited or Negative.

With reduced Dividend Yield at this Price point, I am more cautious now going forward compared to 2021 and 2022.

Disclosure: I have reduced my holding after the surge in Stock Price during 2023 and 2024, but may continue to hold it as a Dividend Stock with 4% to 5% Dividend Yield expectations. I might be wrong in my analysis as I am not a SEBI registered analyst.

4 Likes

The next leg up here will be once new generation of thermal power plants come up.

Thats expected to ramp up by 2025-2027. That will be new demand helping them increase sales by 1-3% above and beyond regular growth.

I agree pricing is a concern but they are eliminating higher costs from the cost structure so maybe margins can be controlled.

Disclosure: Invested from 2022.

5 Likes

As envisaged by me in my previous post, I was expecting muted earnings and net profits in Q2 FY25 and it seems that those concerns have played out.

With massive Capex plans in next 4-5 years, there could be negative impact on ROCE over next few years.

Following report highlights both positives and negatives about Coal India in near to medium term.

Disclosure: Trimmed the position during FY24-25 but still holding for Dividend Yield. Also optimistic about further increase in coal production volumes though net profit growth could be muted. I might be wrong in my analysis. I am not a SEBI registered analyst.

1 Like

Holding from 220 level for dividend only. Now the target price may vary due to n no of reasons. However, I hope dividend will continue to come.

1 Like

Sharkhan Report on Coal India. Buy. TP 560 Rs.

20241218084204_Coal-India-18122024-khan (1).pdf (326.8 KB)

Some interesting Investment rationales put forward in it are:

-

Company has strong growth levers – 1) Volume picking u p with the rise in power demand and 2) potential hike in FSA coal realizations.

-

Thermal capacity addition: With the expected increase in power demand in the next decade, the government plans to add 80GW of thermal capacity till FY32. Over half of the capacity has already been awarded and around 8GW capacity is to be added every year. This would lead to strong coal demand and 7-8% volume growth is expected over the next few years.

-

Government Initiatives: The government’s plans to increase coal production aim to substitute imports, which currently stand at over 250 million tonnes. This will help CIL to boost its production and meet the growing demand for coal.

- Rising Power Demand: An increase in power demand is expected to drive higher coal consumption, benefiting CIL’s volume growth.

- Cost-Control Measures: Initiatives such as reducing manpower are expected to help CIL manage costs effectively, thereby cushioning its margins.

- Valuations and Dividend Yield: CIL’s valuations are reasonable compared to historical averages, and the stock offers a high dividend yield, making it an attractive investment option.

Discl: Invested. Top 5 holdings of my portfolio. Currently at 20% loss. Entered at Peak.

4 Likes

Just entered today in the broader market meltdown.

I feel this will be a steady compounder 6-7% volume growth with maybe 4-5% pricing growth annual on a conservative basis leads to 12% growth +6% odd dividend yield.

Optionality of Coal gassification, critical minerals(like Lithium) mining, etc

Classic case of heads i win, tails i don’t lose much

The problem i see is lot of institutions will avoid taking fresh positions due to ESG norms and being a PSU very less chance of significant re-rating. Having said that lot of domestic mutual funds, including PPFAS, have good position in this.

Disclosure: As stated invested

3 Likes

Report by Share Khan looks reasonable.

We have to keep in mind that, stock price has corrected from 550+ levels to 385 as of today. This is very substantial correction of 30% in Price.

Now it is mostly in the Buy Zone even we apply simple logic. It was trading at P/B > 5.0 just few months back and Now trading at P/B of 2.5.

(Note: Book Value increased in their Annual Report for FY24, so we may have to understand the perspective here).

Why this de-rating might have happened ? Just few thoughts:

(1) During 2022-23 due to wars, Coal Prices moved up across the World.

(2) Coal Auction prices went up and OPM increased substantially for Coal India. Mr. Market re-rated the stock to P/B > 4.5.

(3) Now, Realizations are already declining as reflected in current Revenue of H1 FY25. OPM may not be as high as the levels during FY23 and FY24 going forward.

(4) Power demand generally declines in Rains and Winter which affects coal demands so Q2 FY25 was weak.

(5) Market corrections might have impacted Stock Price of Coal India.

An investor can stay invested in it or can Trade in and out as it gives opportunities to Enter and Exit.

Just adding my observations as holding since Feb-Apr 2022 but adjust my position size from time to time due to large fluctuations in valuations.

This is not an easy stock to hold!! I generally look at P/B for Coal India and P/B of 2.0 to 2.5 looks low to me and P/B > 3.5 to 4.5 looks higher. Brokerages look at P/E for Cyclic Stocks which looks misleading to me. EV/EBITDA can be another measure.

I may be wrong in my analysis. Not SEBI registered.

7 Likes

Thanks for your inputs! They are valuable. I never thought to look at P/B value for an energy stock. Intriguing to learn.

Do you mean 12+6=18% return per year ? I think dividend is part of the earnings and hence should not be added to returns. It leads to double accounting.