Hi,

I had just one concern related to internal and statutory auditor change in the last 5 years. Would be really grateful if the VP community could contribute to this. Here it goes:

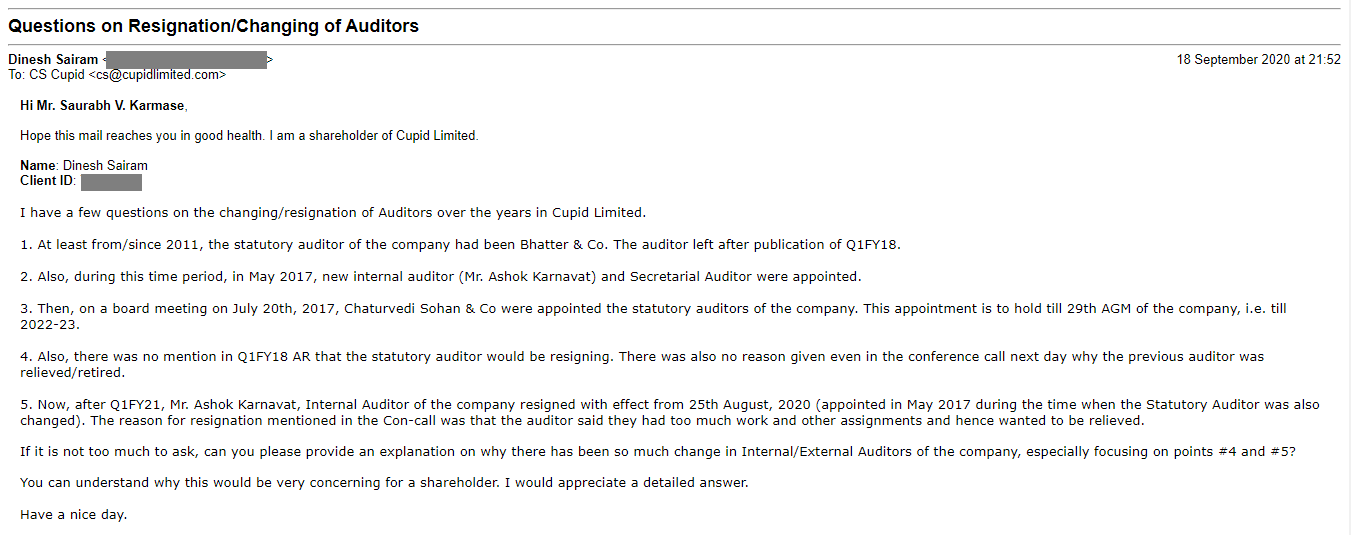

- At least from/since 2011, the statutory auditor of the company had been Bhatter & Co. The auditor left after publication of Q1FY18.

Also, during this time period, in May 2017, new internal auditor (Mr. Ashok Karnavat) and Secretarial Auditor were appointed.

- Then, on a board meeting on July 20th, 2017, Chaturvedi Sohan & Co were appointed the statutory auditors of the company. This appointment is to hold till 29th AGM of the company, i.e. till 2022-23.

(Chaturvedi & Co has been been in existence since 1999… Even during the PR at that time, the list of their clients was included and they performed the audit of around 46 companies. A cursory look would tell you that Cupid would be among 3 of their largest companies they audited. The company had 7 partners and the youngest one, Mr. Rajiv Chauhan, is the signee on most of the Cupid reports till now.)

-

Also, there was no mention in Q1FY18 IR that the statutory auditor would be resigning. There was also no reason given in the PR and in the conference call next day why the previous auditor was relieved/retired.

-

Now, after Q1FY21, Mr. Ashok Karnavat, Internal Auditor of the company resigned with effect from 25th August, 2020 (appointed in May 2017 during the time when stat auditor was also changed).

The reason for resignation mentioned in this Con-call was that the auditor said they had too much work and other assignments and hence wanted to be relieved.

Exact line - "Basically they were overloaded with work and mutually we agreed that it would be better if we find a replacement for him"

As against this, the Board of Directors considered and approved the appointment of B C S AND ASSOCIATES LLP, Chartered Accountants as an Internal Auditor of the company with effect from 26th August, 2020 to 31st March, 2021

Now, the community here has been effusive in praise of the management and corporate governance of the company. Maybe I don’t have enough to connect the dots here, but if there’s one thing we have learnt from previous fiascos, it is that such cliched reasons do not present the underlying reasons all the time.

Is it normally this straightforward in other companies as well for internal auditors to resign with aforementioned reason? This is a risk that one normally runs in small cap companies and personally wanted to be very sure if I’m missing something here.

(Not making any comparions here, but DHFL joint auditors which were appointed in FY13 did not offer themselves for reappointment “in view of their pre-occupation with other work” as per the FY16 annual report. The rest, as we know, is history; hence the reason for my apprehensions.)

Would really appreciate responses from your end.

Regards,

Shashank

Disclosure: Holding a small part of my Portflio.