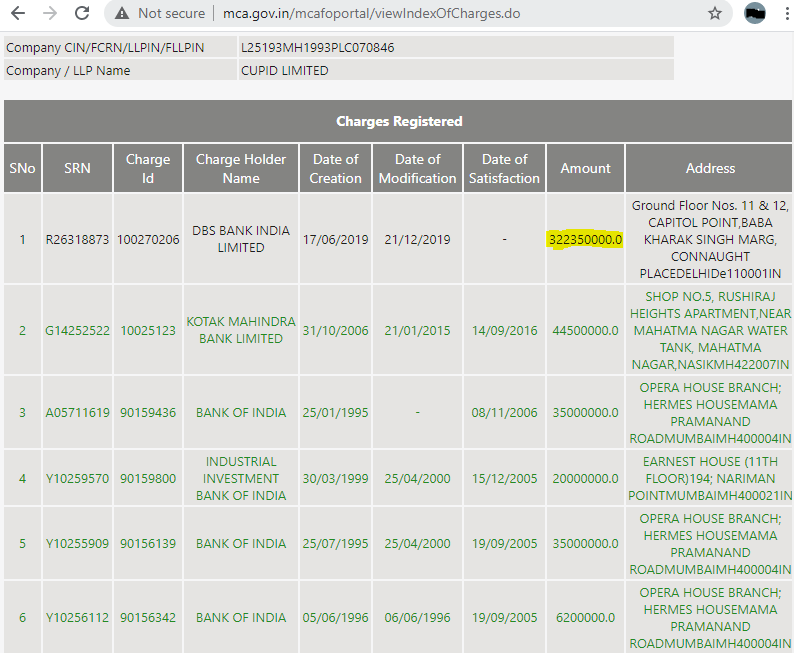

If we compile these together, what we see on today is

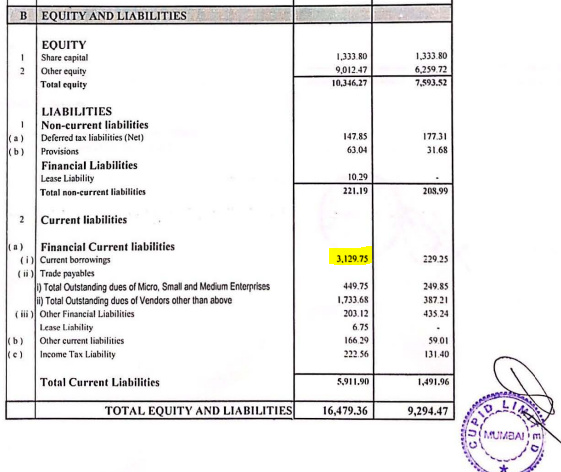

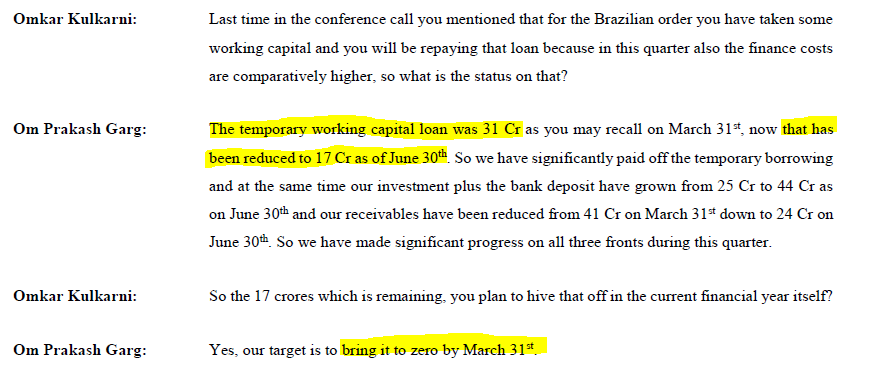

Loan as per management : 17 Cr (on 30th June) Loan as per MCA website : 32.23 Cr (even on 2nd Sept) Loan as per Q4 filling : 31.29 CR

I request your help in understanding it better as I don’t have any background of finance. Say if company had taken a debt of 31.29 Cr on 31-03-2020 (as per Q4 filling) & paid back 14 Cr during Q1 (between 01-04-2020 to 30-06-2020) why does MCA webpage still show 32.23 Cr even on 2nd Sep…

Shall we blame procedural delays at MCA / Bank end for this or there is a gap between facts & management commentary.

The temporary WC loan was 31 Cr. There is a slight mismatch with the MCA figure of 32.23 Cr, and this 1.23 Cr you can consider as gap in management commentary. But the reason probably is that the bank sanctioned 32.23 Cr and filed a charge for that amount, and the company never utilised the limit beyond 31 Cr.

When they mention that it has been reduced to 17 Cr, it means that their utilisation of the sanctioned limit is 17 Cr as on 30th June. They will probably still have the option to increase utilisation back to 32.23 Cr but they are looking to reduce it down to zero.

Probably when they reduce it to Nil and feel that they might not need this sanctioned limit again, they will ask the bank to remove the charge from the MCA website. The charge on MCA website can’t be changed basis fluctuating utilisation of limits because that is the nature of working capital limits. MCA shows sanctioned limits while the management commentary mentions the amount they are using out of that sanctioned limit as on 30th June.

Also note, the Balance Sheet also mentions the utilised amount and not the sanctioned amount. If a bank has sanctioned 100 Cr to a company and their limit utilisation is only 50 Cr, then the March balance sheet will show only 50 Cr as Debt.

We trust the management and know that its NOT a redflag but as per process we need to validate the numbers as well.

Now I conclude that MCA webpage will show the SANCTIONED amount & NOT the availed loan amount. Even if you have paid part of loan, SANCTIONED limit doesn’t change.

The expected reduction in casual sex should reduce the transmission of HIV and STIs, and first evidence of a corresponding reduction in new infections is already available in the literature.

We can also guess that people living with their sexual partners are having sex more often. Less certain, however, is whether there will be a “coronavirus baby boom”. On account of uncertainty tied to the ongoing pandemic and unprecedented economic disruption, couples may have less of a desire to conceive. This logic was born out in a Turkish study in which married women reported having more sex, but few said that they intended to become pregnant. Come early 2021 we may see hints of a baby boom or bust, or perhaps little change at all in birth rates.

Early 2021 is also when we may optimistically have coronavirus vaccines widely available. Then we’ll find out if our sex lives revert to how they were before or are irrevocably altered."

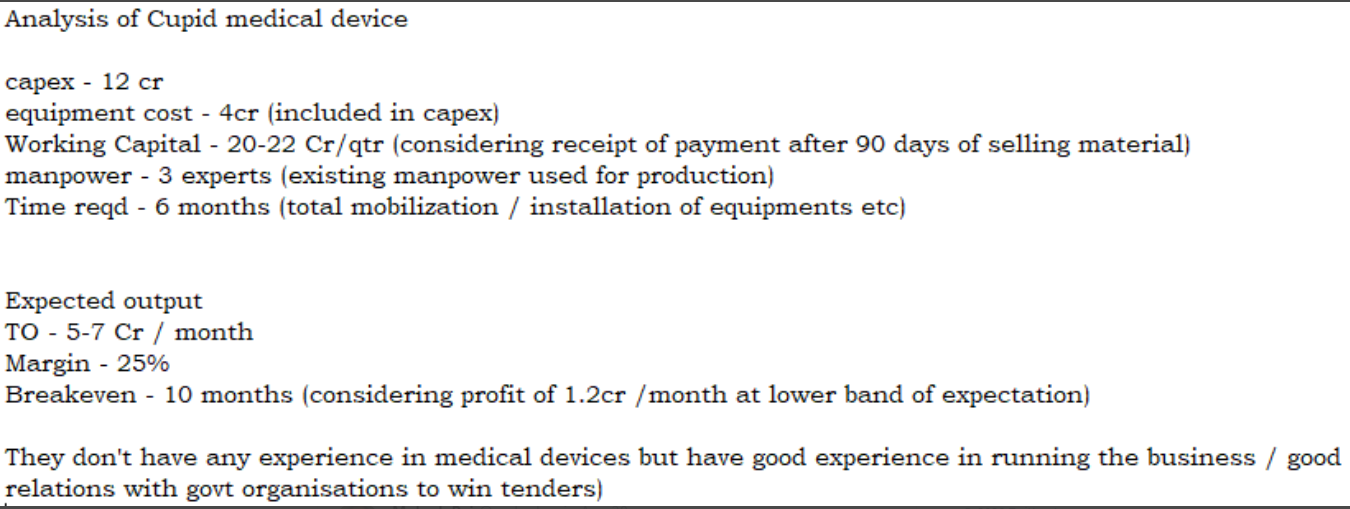

As management is expecting 25% margin on these test kits.

We must compare this with existing player in similar business, who has sold 4.22 lac kits for RT-PCR Tests in August with an average price realization of Rs. 325/- per test. They get roughly 38%-40% profit margin on that. But interesting part is upcoming competition, where they claim that other competitors have started offering rates below Rs. 250/- due to which there market share is reducing. They state that prices can not be drastically reduced due to several business reasons. Coming to Government tenders where Cupid is planning to compete, the prices range is much lower around 150/- to 200/-

Even they have gone on record to quote that GOI has allowed a quota for exports of RT-PCR kits vide trade notice no. 20/2020-21 dated 31/07/2020. However, it allows only one application per manufacturer per month to be filed. So restriction are already in place, considering huge no of patients in our country.

Due to huge competition from Chinese/ Korean companies’, prices have gone down globally also.

Now the question to ponder is “Will this new venture be fruitful & can it contribute as per management expectations”. We are still 3 months away from jumping in the tough market where healthy margins are enjoyed by early birds and little or very little juice is left with each passing day.

Let me also take a moment to appreciate the fact that Cupid is a great example of how to treat the minority Shareholders and transparency / disclosures.

Thanks Dinesh! I was just reading the con-call and opened ValuePickr to ask about the update and here we go! I think this reply has shown their integrity.

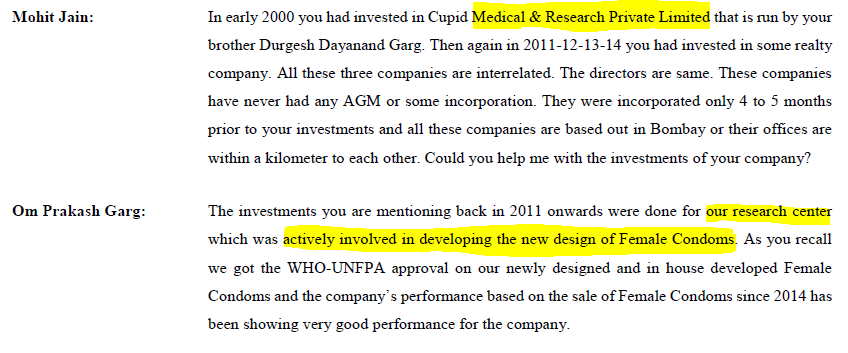

But in the con-call Mohit Jain was stating the amount as around 50 lakhs and the mail states it as around 40 lakhs.

So, has anyone figured out why there is a difference?

Fantastic work Dinesh. Thanks so much for this. That one email has removed all doubt that I had regards cupid(Corporate governance, US female condoms fda, Medical devices) Your blog post started me on my way to building conviction and your email reply has finally got me over the edge. Your hard work, grit and determination regards following a company in so much detail is inspiring. One question though… any idea when the actual us fda approval for female condoms is slated to happen? Sales are to start around FY 22 so I’m assuming they need to start planning for capacity etc now itself (especially since the market is so huge) but I cant find anything regards updates on the actual approval(I must have missed it). Also, would it be B2G only with the US or also B2C?

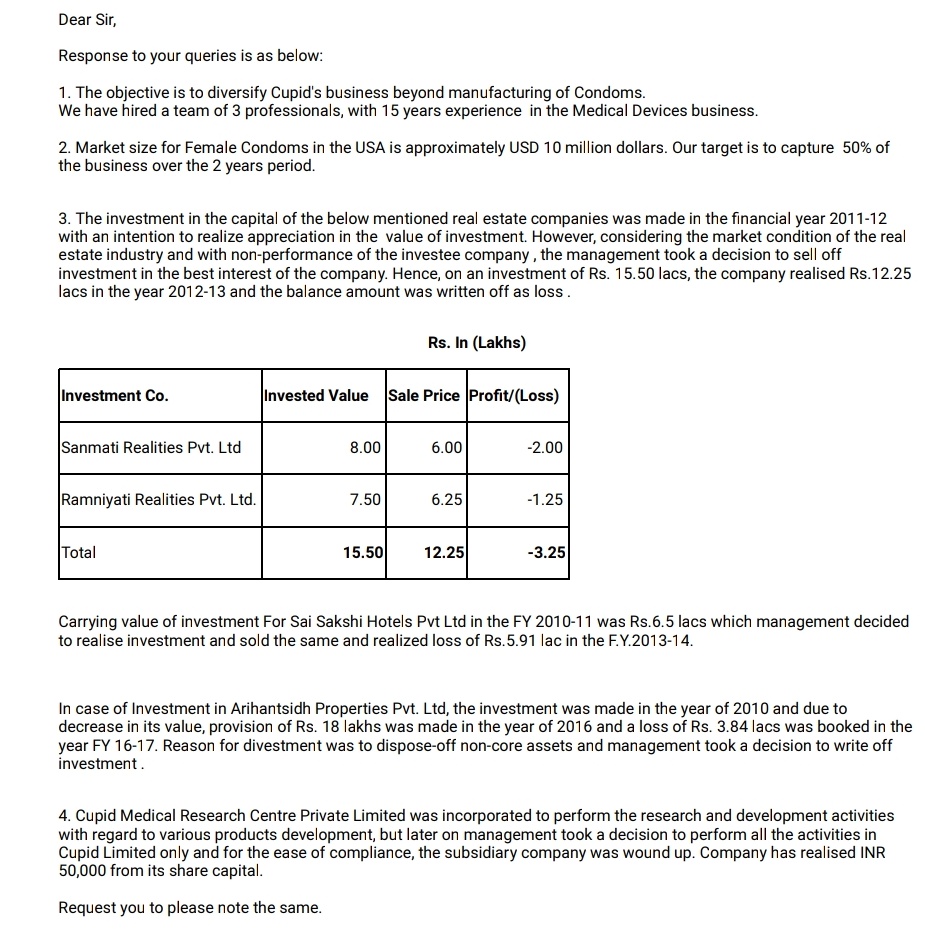

But still, those real estate investments seem very shady. Management could have easily pocketed some gains. Its very easy to manipulate it on property side. Might give an insight to the character of management. Because 50 lakhs was a significant percentage to net profits back then. As veterans have said all shenanigans start small and with trial and error. Good business dynamics and a doubtful management. They may not be doing such things now but how do I trust them in future when there is something fishy in the past? Now I am in a dilemma. But as tempting and mouth watering as this is, I think I am going to stay away. Nonetheless, it would be a great learning experience.

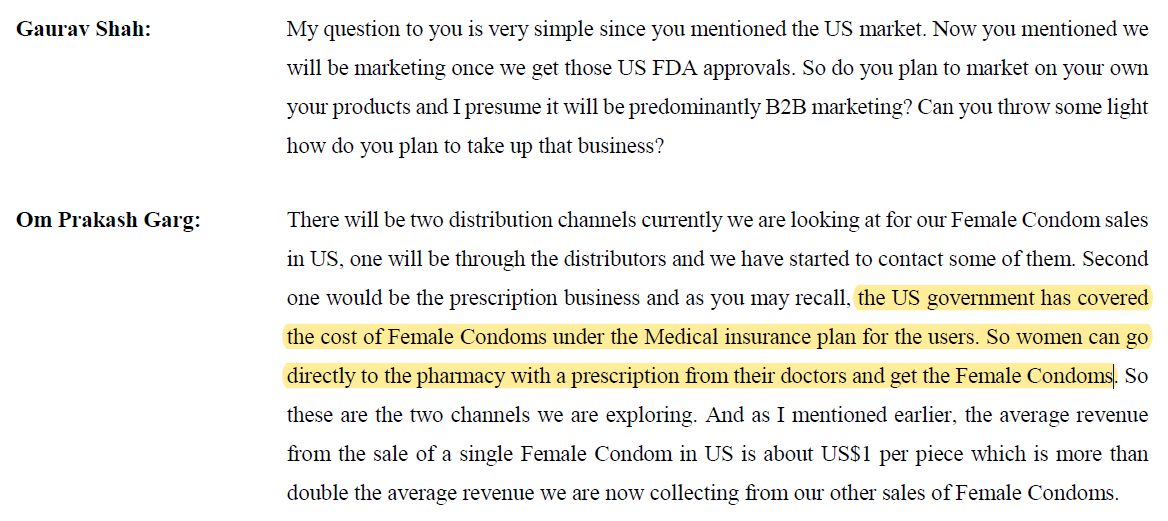

An efficacy study needs to be submitted to the USFDA for Female Condoms approval. It’s been going on in Africa for some time. However, COVID19 has delayed the study. The same was discussed in the concall.

But as you say, if they’re expecting Sales to start from FY22, the study would be submitted before that I guess.

The Female Condoms market in the US is mostly Prescription-based. So Doctors would recommend Female Condoms for select patients and they’d buy it from OTC. You can read FC2’s Annual Report to understand more.

But I guess they can also market directly in OTC. We’ll head about the strategy later I suppose.

A bit ambitious, but completely reasonable. Cupid will have a massive Cost advantage over FC2. Read FC2’s 10K filings. They’ve mentioned Cupid as a threat in at least 4-5 places.

When I valued Cupid, I assumed they’ll be able to capture 50% of the market in 10 years (Conservative assumption). But I don’t think it’s unreasonable to say that they can capture it in just 3-5 years.

But in their recent con-call they said the medical insurance plan covers Female condoms which means they could just buy it from a pharmacy like Male condoms.

Am I right?

Of course, they could. But the market / Sales is mostly prescription-based. The awareness about Female Condoms is limited.

Even in Europe, Cupid is already selling Cupid Angel in OTC. But the Sales figures are extremely low.

It will take quite some time for the Female Condom to be as widely used as the Male Condom (The Price premium over Male Condoms is a major reason why it isn’t so popular).

Guys… more scuttlebutt stuff I have stumbled upon… from verus concall for the previous qtr… they seem to be doing very well with fc2 in the prescription mkt… with increasing sales and amazing margins… their management talks about how the prescription mkt doesn’t involve much mkting cost…on similar lines to Mr gargs commentary…

I’m sure if you’re the only company legally allowed to produce Female Condoms (In the U.S.), Doctors can only prescribe your product. No Marketing required there.

Hope that clarified.

Hope that clarified.

No Marketing required there.

No Marketing required there.